Sell General Cannabis (OTC: CANN) to Avoid Potential 73% Decline

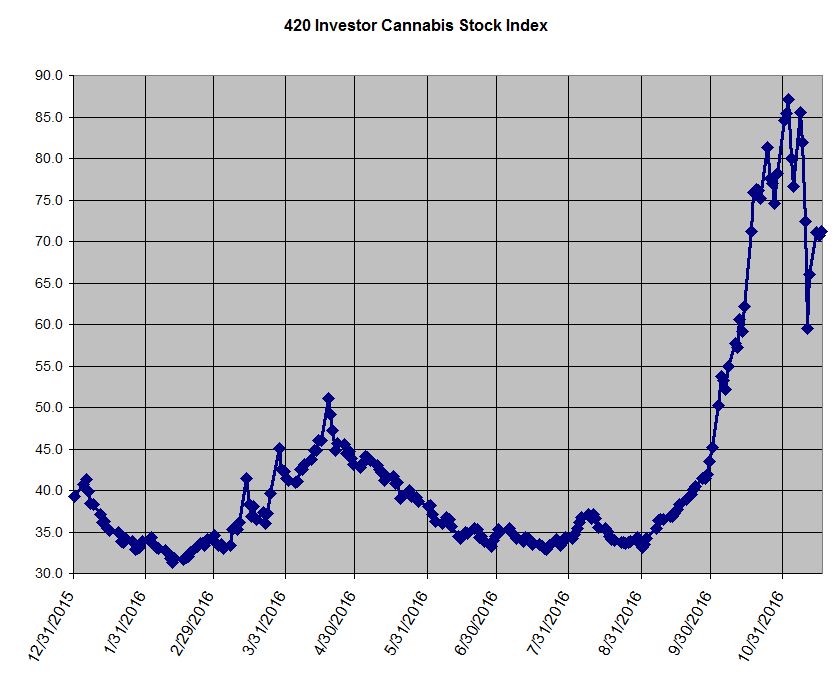

Cannabis stocks had a big run-up into the elections this year, peaking, on average, a week ahead on November 2nd, when the 420 Investor Cannabis Stock Index closed at 87.08, representing an increase of 162.6% from the end of August:

In the September 420 Investor Newsletter, which was published on 8/31, I discussed my expectations for a sector rally in advance of the elections, which featured ballot initiatives in 9 states, and shared several names with my subscribers that I expected would perform well, including General Cannabis (OTC: CANN). The company, formerly known as Advanced Cannabis Solutions and based in Colorado, provides several different services to the industry, including security (through Iron Protection Group, which it acquired in 2015), consulting (through Next Big Crop Consulting, which it acquired in 2015), apparel (through Chiefton Supply Co, which it acquired in 2015), supplies (through General Cannabis Supply), branding (through Chiefton Design) and real estate (it owns three acres with a cultivation facility in Pueblo that it leases).

Indeed the stock did have a very strong run, but it has retreated from the peak of $5.19 (a double-top from 10/18 and 11/08), where it had advanced 574% from its close of $0.77 on 8/31:

For anyone who was able to profit, I think CANN should be sold despite the 28% decline from the peak. I am expecting the stock to decline to below $1.00 within the next four months, which would represent a decline of more than 73% from the current price of $3.75.

In the November issue of the 420 Investor Newsletter, I described "The Atrocious Capital Raise at General Cannabis" as a reason to be very cautious on CANN. I discussed the recent capital raise, which was detailed in an 8-K filing, as the catalyst for the large decline I expect. CANN raised $3mm through the issuance of promissory notes and warrants, with $550K used to pay off existing debt and the balance representing new capital. The notes bear interest at 12% (so $360K per year in interest) and mature in 2019. The warrants are the issue, as the company issued 4.5mm warrants at $0.75 and 4.5mm at $0.30. These can't be exercised until March 21st.

The company currently has 15.6mm shares outstanding, so the 9mm warrants will boost the float rather dramatically. Even with extremely elevated trading volumes, the 9mm warrants represent over 10X the number of shares traded per day on average over the past month. The exercise of options is likely to be sloppy, as the Form D associated with the financing indicated that there were 16 separate accredited investors who participated.

For purposes of valuation, the fully diluted share count should include the warrants and 8.68mm options with a weighted average exercise price of $0.97, giving the company a current market cap at $3.75 and based on 33.3mm shares of $125mm, which is way out of line with the fundamentals.

The recent 10-Q highlights a weak balance sheet and inconsequential revenues along with negative operating cash flow. The balance sheet, which includes the September financing, shows total assets of $4.57mm, with cash of just $1.06mm despite having raised $3mm, most of which was deemed new capital. All current assets are only $1.4mm, but the company has current cash liabilities of $1.88mm (note that I am excluding the derivative warrant liability of $15.4mm). As it stands now, the company doesn't have the financial capability to cover its obligations unless it generates cash from its operations or finds alternative financing.

Through the first three quarters of 2016, CANN generated $2.2mm in sales, but the operating loss has exceeded $3.1mm. Cash flow from operations has been -$1.06mm. In Q3, the operating loss was $1.3mm, with the company using $629K to fund operations. Sales of $810K in Q3 grew 15% sequentially, but the operating loss expanded from $837K. At the present rate, the company will exhaust its remaining cash even before meeting its cash obligations by the end of Q1 next year.

I expect that the CANN warrant exercises will crush the stock within the next four months, as the warrant holders will be able to pocket $29mm based on the current price of $3.75, a very nice return for lending CANN $3mm at 12%! Adding some support to my negative thesis, CEO Robert Frichtel had a significant sale of stock in October, selling a total of 100K shares that were reported here and here, pocketing $361,700 (average selling price at $3.617). Based on the high valuation, weak financials and the pending warrant exercises, investors should consider selling CANN.

Recent free content from Cannabis Analyst

-

Marketfy Has Evolved - We're Moving to a New Platform!

— 3/06/24

Marketfy Has Evolved - We're Moving to a New Platform!

— 3/06/24

-

420 Investor Weekly Review 12/23/22

— 12/26/22

-

420 Investor Weekly Review 12/16/22

— 12/16/22

-

420 Investor Weekly Review 12/09/22

— 12/09/22

-

420 Investor Weekly Review 12/02/22

— 12/02/22