The Weekly Top 10....History tells us the rate cuts do not impact markets anywhere near as quickly at QE programs.

THE WEEKLY TOP 10

Table of Contents:

1) Needless to say, the S&P stands at a very important technical juncture.

2) History shows that the stock market acts much more quickly to QE than it does to rate cuts.

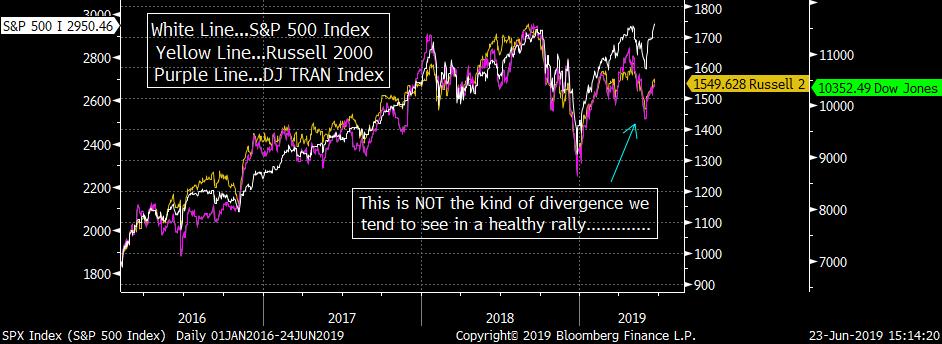

3) The divergence between the DJIA/S&P 500 and the Russell 2000, TRAN & SOX is still a concern.

3a) Are tech investors simply "swapping" within the sector?

4) The Treasury market is over-bought & due for a correction (bounce in rates).

4a) The corporate bond market is INCREDIBLY over-bought, and even MORE ripe for a correction.

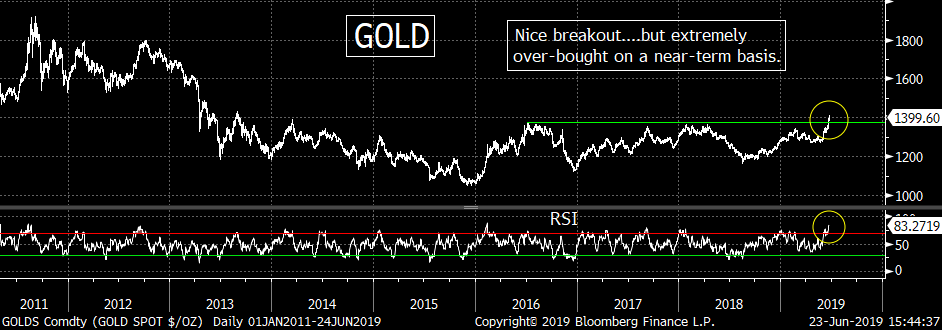

5) Gold: Looks great, but needs to work off its over-bought condition over the near-term.

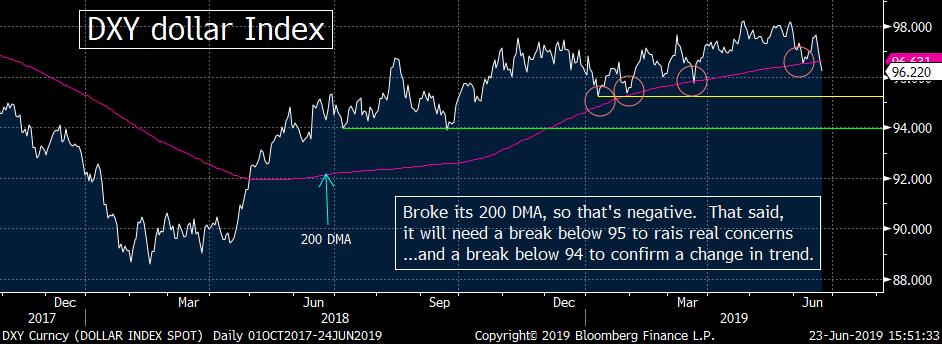

6) The dollar...broke its 1st key support level...so it has become some-what vulnerable.

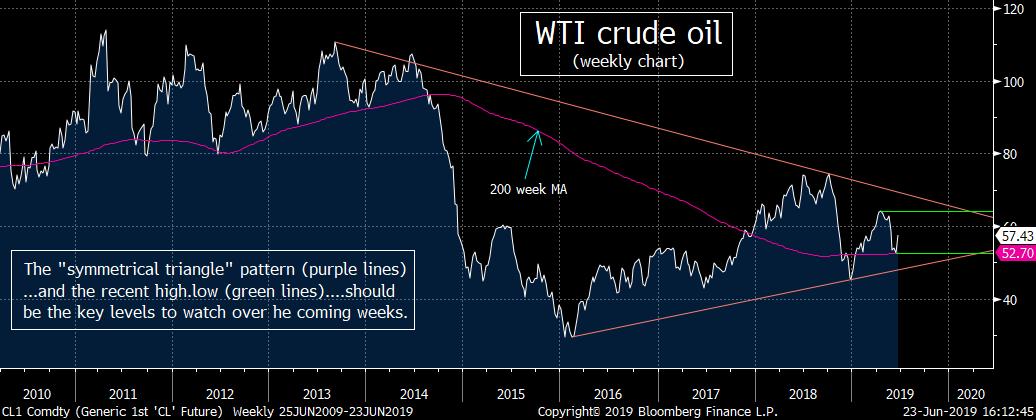

7) LOTS to look at with crude oil (including a "symmetrical triangle" pattern).

8) European stock STILL act very poorly...which should concern everybody.

9) Trump supporters should actually be hoping for a correction right now. (Think 2011.)

10) Summary of our current stance.

Short Version:

1) You don't have to be a junky towards technical analysis to know that when the broad market indexes (or anything else) tests the same level several times...a meaningful break above that level would be very bullish. Similarly, if it "fails" to break that level once again...and rolls over, the ensuing decline tends to be a material one. Therefore, whether stock market sees upside follow-through or not over the next week or two is going to be very important for the prospects of the U.S. stock market over the rest of the summer.

2) As much as the Fed has become much more dovish, they haven't "acted" yet...and there are reasons to believe that they will not "act" until the economy (and/or the markets) see more weakness. However, we'd also note that history shows that there is a big difference between “rate cuts” and “QE programs”. QE programs inject liquidity directly into the system/markets...and thus have a much more immediate impact. Rate cuts tend to have a delayed impact. In fact, history says that the stock market frequently (usually) declines after the 1st rate cut.

3) Another item that leads us to worry that we might not see more upside follow-through is the continued under-performance of three important leadership groups/indexes. As the DJIA & S&P 500 are making new highs, the Russell 2000 still stands 12% below its own record highs, the DJ Transports and SOX semiconductor index both stand 10% below their all-time highs. These substantial divergences…are it’s not the kind of action you tend to see before convincing rallies.

3a) We do need to point out that despite this wide divergence between the semis & the SPX…the XLK tech ETF is testing its all-time highs. Therefore, this could simply be a situation where investors are swapping out of one area of the tech group and into another. However, the FAANGs are also under-performing...as 4 out of 5 remain more than 10% below their all-time highs. History tells us that when these two sub-groups within the tech sector break-down, the rest of the group tends to follow eventually.

4) With U.S. 10yr Treasury yields briefly falling below 2% last week, everybody is focused on that market. However, it has become quite over-bought and over-loved, so it should be due for a pull-back (a bounce in long-term rates). We'd also note that the investment grade corp bond market (LQD) is even more over-bought (the most over-bought this century). Therefore, investors need to be careful about this VERY highly leveraged part of the fixed-income market over the coming weeks and months.

4a) Even though the HYG high yield ETF made a "higher-high" last week, it has actually been range-bound for a long time. We'd also point out that the relationship between the high yield & investment grade markets have actually been showing some stress all year...just like it did in the 4th quarter of last year and throughout late 2015 and very early 2016 (just before the stock market corrected back then). Therefore, we're not so sure that investors should be as complacent as they seem to be about the current state of the markets.

5) Gold broke above the all-important $1,380 level last week...which is very positive for the yellow metal. That said, it is getting very over-bought on a short-term basis...and very over-loved as well. Therefore, we think the commodity will pull-back over the very short-term...which means investors should avoid chasing gold right here. In other words, we'd be a buyer of gold on weakness...rather than chasing it over the next week or two.

6) The dollar broke below its first key support level last week...its 200 day moving average. The DXY dollar index still needs to break below the 95 level before we can raise a warning flag on the green-back (& it would have to break below 94 to actually confirm a change in trend). However, the break of this first key support level is something to take notice of...especially since any serious break-down in the dollar will have all sorts of implications for many commodities and emerging markets (among other markets).

7) Having said this, the correlation between the dollar & crude oil is actually not a compelling one...BUT that doesn't mean that WTI is not a key juncture as well. It is sitting right in the middle of a "symmetrical triangle" pattern...so whichever way it breaks that pattern should be important for how crude acts over the rest of the summer. Obviously, the OPEC meeting, the G20 meeting and the situation with Iran will be VERY IMPORTANT to this issue...but keeping an eye on this pattern could be helpful in the weeks ahead.

8) We don't mean to beat a dead horse, but the European banks continue to act VERY poorly. The European bank index stands 32% below its early 2018 highs...and just 2.6% from its December lows. That compares to the broad European stock index...which is just 4.4% below its early 2018 highs and 16.7% above its Dec lows.In other words, despite the bounce last week, the divergence between the European stock market and the European banks is a VERY wide one....which is certainly a bearish development.

9) We'd like to point out an interesting tidbit about the markets and the upcoming presidential election. Maybe President Trump wants the stock market to go up this summer...but he shouldn't. Just look what happened the last time an incumbent ran for President (Obama in 2012). During the summer of the year before the election, the stock market fell 18% from July into very early October. THEN, it bottomed...and rallied a whopping 33% over the next 12-13 months...and President Obama was re-elected. Voters don't care what the market/economy does the summer of the 3rd year of a term. They care about what's going on during the election year.

10) Summary of our current stance......If the S&P can break more meaningfully above its triple top highs, it will be very bullish for the stock market. However, we're not convinced this will happen. The Fed is definitely more dovish, but they have not indicated a July cut is assured. Besides, history tells us that the "first rate cut" has frequently (usually) been followed by DECLINES in the stock market, NOT gains. In other words, "rate cuts" are not "QE". They do not have the same direct & immediate impact on the markets that QE programs do!!! Therefore, we believe the market is setting up for another "head fake"...like we saw when it made a new high in April. However, a 2%+ move above its old highs will force us to change our stance.......Away from the broad stock market, we think that gold is poised to break-out and the dollar is poised to break-down...BUT both will probably take "breathers" over the short-term before they do. Finally, we're concerned about the technical condition of the investment grade corp bond market...and very worried about the action in the European banks. Therefore, there will be plenty to talk about this summer...no matter what happens in the stock market over the next week or two.

Long Version:

1) Needless to say, last week was a very good week for the stock market...with the S&P 500 rising 2.2%...and it now sits right on its highs from April (as well as from the highs from last September...and from and early 2018). Therefore, it clearly now stands at a very important juncture on a technical basis. You don't have to be a technical analysis junky to know that when the broad market (or anything else) tests the same level several times...a meaningful break above that level would be very bullish. Similarly, if it "fails" to break that level once again, the market tends to see a fairly decent decline. We mentioned last weekend that "the battle lines" were well drawn in the S&P...and it is now testing one of those well-defined battle lines...so the action in the stock market as we move into the last week of the 2nd quarter and the first week of the third is going to be quite important for how the market acts over the rest of the summer. (That was short & sweet and pretty clear...but there really isn't much we need to add to this comment, so we'll leave it there for our first point this weekend.)

2) The primary catalyst for last week's rally, of course, was the Fed's announcement on Wednesday... which seemed to lead investors to believe that the Fed would definitely cut rates at their next meeting at the end of July. There is no question that the Fed has become even more dovish in recent weeks...and there's also no question that whenever the Fed has actually acted in an accommodative way over the past decade, it has been bullish for the stock market. THIS is why we started this weekend's piece with a technical look at the S&P 500 Index. A more meaningful break above it's old highs (basically a triple top high), it will be very bullish...and if we do indeed see that kind of more significant breakout, we'll have to become more constructive on the stock market.....However, we DO want to point out a few key issues to contemplate after last week's Fed announcement. First of all, as our economist (Paul Shea) said midweek last week, a slight majority of FOMC members actually predicted no rate cuts in 2019...so Paul believes that the 90%-100% odds of a rate cut that the Fed Funds Futures are pricing-in right now is too aggressive. (Besides, the Chairman definitely said that that a rate cut would come IF the economy showed more signs of weakness.) Second, we'd also point out that there is big a difference between a "rate cut" and "Quantitative Easing" (QE). QE programs inject liquidity into the system in a much more direct way than a rate cut...and thus the historical impact has been quite different. For instance, when QE1, QE2 & QE3 were implemented, the stock market rallied IMMEDIATELY. (The same was true for "Operation Twist".) However, the last time interest rates were cut by the Fed was in mid-December of 2008. That's right, 2008...more than 10 year ago!!! Therefore, it was the direct injections of liquidity...and NOT the rate cuts...that have caused the "central bank fueled rallies" of the past decade. In fact, the last two times the Fed BEGAN cutting rates (in 2007 and 2001), the stock market DECLINED for an extended period of time. (After the first cut in 2007, the market began its 56% decline a few weeks later...and it 2001, it was followed by a further decline of 43% in the stock market.) Of course, those were unprecedented situations, but as we have pointed out that in other times in history (in the 20th century), the stock market has also frequently continued to decline AFTER the Fed begins cutting rates (going all the way back to WWII).....Very simply, history shows us that the stimulus that comes from rate cuts takes a lot longer to impact the economy & the markets than the direct liquidity injections that QE programs provide. Therefore, those who think we'll see and strong and immediate rally from this most recent development could be sorely disappointed. THIS is why we're going to have to see a more meaningful break above the old highs before we can turn more constructive on the stock market. Let's face it, the S&P broke slightly above its September highs in April...only to roll-over quite harshly just a few days later.

3) Of course, one glaring concern we have on the technical picture of the broad stock market is the action in the Russell 2000. So this is another reason why we'll want to see more upside follow-through in stocks before we can say the sideways range the market has been in for almost 18 months will come to an end. Yes, it has seen some good days here and there recently, but it still lags badly behind the S&P 500...sitting more than 12% below its 2018 all-time highs! This is especially concerning because the reason for the pull-back in May was due to the trade tensions with China...which should have given the domestically oriented small-cap names a chance to narrow its divergence. However, this has not take place......The same is true for the Transportation stocks. The DJ Transportation Index is almost 10% below its 2018 highs...while the DJIA is testing new all time highs. That's quite a divergence...and certainly does not bode well for the people who follow the Dow Theory......Finally, the most important leadership group in recent years (and one of the most important over several decades)...the semiconductors...do not act very well either. The SOX semi index sits more than 10% below its April highs...so it has not bounced-back anywhere near as much as the broad market...which is yet another divergence.

3a) We do need to point out that despite this wide divergence between the semis & the SPX...the broader XLK technology ETF is testing its all-time highs. Therefore, this could simply be a situation where investors are swapping out of one area of the tech group and into another. However, they certainly are not piling into the FAANG stocks. Four of the five FAANGs have still more than 10% below their highs (FB -11%, AAPL -13%, NFLX -11% and GOOGL -13%)...and even AMZN is still 5% below its all-time highs. Again, this might just be a situation where people are simply doing some swapping...but history tells us that when these two sub-groups within the tech sector (semis & FAANGs) break-down, the rest of the sector tends to follow before too long. (Of course, most of the FAANGs have not been around very long, but it is quite telling that many of them began to break-down BEFORE the 4th quarter of last year...and ended up being a precursor to a deep correction in the entire sector later in the year last year.)

4) Needless to say, a lot was made of the drop below 2% in the U.S. 10yr Treasury note yield mid-week last week...and rightfully so (even though it bounced back and closed at 2.05% on Friday). The Treasury market had certainly become extremely over-bought on a price basis (oversold on a yield basis) just after the Fed's meeting on Wednesday...and still remains that way this weekend. Sentiment for this all-important fixed income market was also getting extreme...as bullishness among futures traders reached 90% on a couple of days last week. Therefore, this market is getting ripe for a short-term pull-back (short-term rise in rates). The "positioning" in that market is not extreme yet, so any bounce in rates might only last for 1, 2 or 3 weeks...but those betting only lower long-term rates immediately might want to be a bit careful over the near-term.....However, the real reason we're pointing this out is because the investment grade corporate bond market has become EXTREMELY over-bought (much more than the Treasury market). Looking at the RSI chart the LQD investment grade corp bond ETF, it moved above 87 on Thursday! In fact, its weekly RSI chart moved above 80 last week! This is the highest reading ever, so the high grade corporate bond market is the most over-bought it has been by this measure since the ETF came into existence in 2002. GIVEN HOW MANY VERY SUCCESSFUL FIXED-INCOME MANAGERS HAVE BEEN WARNING ABOUT THE HUGE AMOUNTS OF LEVERAGE THAT EXISTS IN THE CORPORATE BOND MARKET TODAY, THE FACT THAT IT HAS BECOME SO INCREDIBLY OVER-BOUGHT ON A TECHNICAL BASIS IS SOMETHING INVESTORS NEED TO CONSIDER WHEN MAKING ANY DECISIONS ABOUT THIS PART OF THE FIXED-INCOME MARKET GOING FORWARD.

4a) We'd also point out that although the HYG high yield ETF made a "higher-high" on Thursday, high yield market has been range-bound for about three years now. We'd also note that the relationship between the high yield & investment grade markets have actually been showing some stress all year...just like it did in the 4th quarter of last year and throughout late 2015 and very early 2016 (the last two times the stock market has fallen 20%). Therefore, we're not so sure that investors should be as complacent as they seem to be about the current state of the markets.

5) Gold broke above the all-important $1,380 level last week...which is very positive for the yellow metal. That said, it is getting very over-bought on a short-term basis...and very over-loved as well. Therefore, we think the commodity will pull-back over the very short-term...which means investors should avoid chasing gold over the near-term. In other words, we'd be a buyer of gold on weakness...rather than chasing it over the next week or two......That said, any break above last week's highs (especially on a weekly basis), is going to be VERY bullish for gold. Therefore, our "buy on weakness" call is definitely a short-term one. What we're trying to say is that if any short-term pull-back is followed by a nice "higher-high" (above $1,400), we wouldn't mind adding to positions at higher prices at that later date. In other words, it's okay to chase something to a certain degree once it has broken out. It's just in this case, we think it would be better to buy it on weakness...and THEN be willing to chase it a little bit after it has worked off its very-short-term-over-bought condition (as convoluted as that might sound)..........Looking at the long-term chart on the yellow metal, we can see that it has already broken above its trend-line going all the way back to its 2011 highs. On top of this, it had made some important long-term "higher-lows" (in late 2016 and mid 2018). Therefore, the fact that it has been able to break to a new "higher-high" above $1,380...which had been VERY TOUGH resistance for almost 3 years...is a very bullish development.........Of course, we always have to worry about a "head fake". If gold reverses sharply lower and cannot regain last week's highs, it will signal that its breakout was indeed a head fake and investors should step back....and look for another opportunity to go long gold. With that caveat, things look very good for the yellow metal.

6) The dollar broke below its first key support level last week...its 200 day moving average. This 200 DMA has been rock-solid support for the green-back all year...testing (and holding) that line five different times...before breaking below that line on Friday. Of course, one day does not make a change in trend...so we have to watch to see if the dollar bounces-back quickly. (As it is with gold, we always have to guard against "head fakes"). Also, as we have stated in recent pieces, we'll need to see a move below the 95 level on the DXY dollar index to give us more confidence that the dollar's upward trajectory was coming to an end. On top of this, we'd also need to see it break below 94 before we could confirm that an important change in the long-term trend of the dollar has taken place, but there's no question that Friday's break-down was important.........Needless to say, any serious break-down in the dollar should be positive for the above-mentioned gold commodity. If the dollar continues to fall immediately, any near-term pull-back in gold could/should be short-lived. Of course, any further weakness in the DXY would also have a positive impact on other commodities...and the emerging markets as well.

7) It's interesting to note that unlike many/most commodities, the relationship between the dollar and oil is not a compelling one. Sometimes they move in the same direction, but sometimes they move in the exact opposite direction. However, that doesn't mean crude oil is not at an important juncture too. IT IS! First of all, as we all know, WTI has seen two big moves this year...with its 55% rally off the December lows into April...and then its 22% decline into early June. There are varying opinions on where crude oil will go next...and the OPEC meeting (and the results of the G20 meeting)...as well as the situation with Iran...should have an important impact on the next big move (duh).......We'd just like to point out the technical picture. It was quite positive that WTI bounced off its 200 week MA during its recent decline (which also created a "higher-low")...so that's positive. However, it's now at a very neutral position. It's weekly RSI chart is in no-man's land right now...and the commodity sits right in the middle of a long-term "symmetrical triangle" pattern. So the direction in which WTI breaks this long-term pattern should be quite important......Over the shorter-term, that 200 week MA will obviously be the key support level...& the April highs of $68.30 will be important resistance......This is a long-winded way of saying the action in oil early next week is not going to be very telling in front of these two big meetings (and with the situation in Iran up in the air), but keeping an eye on these support/resistance levels should be helpful in the coming weeks.

8) We don't mean to beat a dead horse, but the European banks continue to act VERY poorly........Yes, they did bounce last week...but only by 0.85% (vs. a 1.6% bounce in the STOXX Europe 600 Index and a 2% pop in the German DAX index). The European Bank Index has fallen 12.8% from its April highs...and now stands less than 1% from its June 3rd lows and just 2.6% from its December lows. (It is also a whopping 32% below its early 2018 highs!!). This compares to the broad European stock index....which stands 4.2% above its June 3rd lows...16.7% above its December lows...and only 4.4% below its early 2018 highs.....In other words, despite the bounce last week, the divergence between the European stock market and the European banks is a VERY wide one. This would be a concern EVEN if the European stock market was acting well compared to the rest of the world's stock markets...but as we all know, just the opposite has been taking place.

9) We'd like to point out one thing to those who say the President Trump wants the stock market to go up every day...and in a straight line. This could indeed be true, but it's not what he SHOULD hoping for the stock market if he wants to get re-elected. (It's also not what his supporters should be hoping for if they want him to get re-elected.)....Just look what happened the last time a sitting president rant for re-election. That obviously took place in 2012. Back in the summer of 2011 (17/18 months before the election...which is where were stand right now), the stock market began an 18% decline from early July into early October of that year. HOWEVER, the stock market then bottomed out...and began a rally that took the S&P 500 up more than 33% over the next 12-13 months. Of course, even though the economy was still quite sluggish in 2012, President Obama was re-elected. In other words, the public completely forgot about the deep correction that took place during the summer before the election. They only cared about how things were going throughout the election year...and how things were going when Election Day came around. (The market did fade a slight amount just before the election, but it was still up almost 30% over the previous 12 months, so people were feeling quite good.)......No, we are NOT saying that the President can control the stock market. However, for those who DO think he can, they shouldn't assume he'd want it to stay elevated right now. If anything (and as crazy as this might sound), President Trump should be hoping that the stock market is in correction territory by Labor Day. Then it will have a lot more upside potential in the 12-14 months leading into the 2020 election.

10) Summary of our current stance......It might seem crazy for anybody to think that the stock market cannot go a lot higher now that the Federal Reserve has indicated that they will cut short-term interest rates if the economy continues to weaken. The problem in our minds is that there is a difference between the stock market & the economy...and the stock market could fall again (from its now over-bought condition) BEFORE the data gets worse (and before the next Fed meeting at the end of July). Also...and more importantly...history shows that the Fed usually has to actually "act" before it's positive for the markets...AND that QE programs are have a much more immediate impact on the markets than rate cuts do. In fact, when the Fed cuts interest rates, the market frequently (more often than not) falls quite a lot before the impact of the rate cuts helps turn things around......If you step back and look at the other issues facing the markets, it makes it hard to justify a stock market at record highs. The economy is weakening, earnings estimates are falling and there seems to be little hope of a positive outcome to the trade negotiations over the summer. (The best we seem to be able to hope for is "nice progress" in the negotiations.).....Having said this, if the market can break more meaningfully above its old highs (in a way it was not able to do in April), we will have to reassess our stance.......We were spot-on when it came to calling for a bottom in the stock market back in late December...calling for a pull-back in late April...and calling for a short-term bounce on the first day of trading in June. However, we turned cautious again a bit early this time around. We're not ready yet to turn bullish just yet, but we have to admit that we'll have to make a change if we see much more upside follow-through. If history is any guide, remaining cautious right now will turn out to be the right call.......Away from the broad stock market, we think gold poised to break-out and the dollar is poised to break-down, BUT we think they're take near-term "breathers" before they do. Finally, we're concerned about the technical condition of the investment grade corp bond market...and very worried about the action in the European banks. Therefore, there will be plenty to talk about this summer...no matter what happens in the stock market over the next week or two.

Enjoy the rest of your weekend!

Matthew J. Maley

Managing Director

Chief Market Strategist

Miller Tabak + Co., LLC

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22