THE WEEKLY TOP 10

Every weekend, we write a piece we call "The Weekly Top 10". However, this is NOT a regurgitation of Barron's or the weekend edition of the WSJ. Instead, we try to cover the issues most people are not focusing on...and when we do talk about the mainstream issues, we try to look at them from a unique angle......Below, you will find two of our bullet points (#'s 1 & 5) from this weekend's edition (both the "Short Version" and the "Long Version" of those bullet points). If you would like to see the full edition...and see what our subscribers get every weekend (along with our "Morning Comment" on a daily basis during the week), please click here to subscribe to "The Maley Report" (TheMaleyReport.com)......Thank you very much.

THE WEEKLY TOP 10

Short Version:

---1) We have been involved in the markets too long to believe what many pundits are trying to argue today. They’re not using the phrase, “It’s different this time,” but they ARE still using this argument. They’re just using different words to describe it……....We understand that the Fed is providing loads of liquidity right now, but they also know that they cannot control bubbles once they develop, so they will still do what the need to do to avoid one. In other words, this liquidity will not last forever.

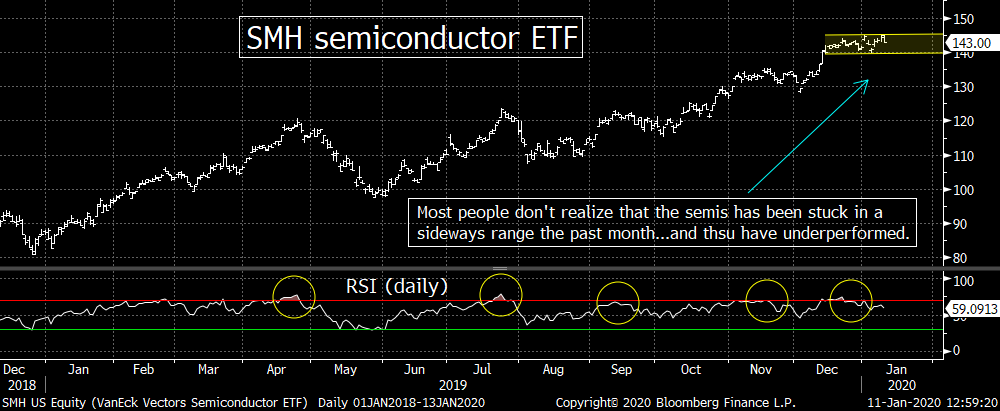

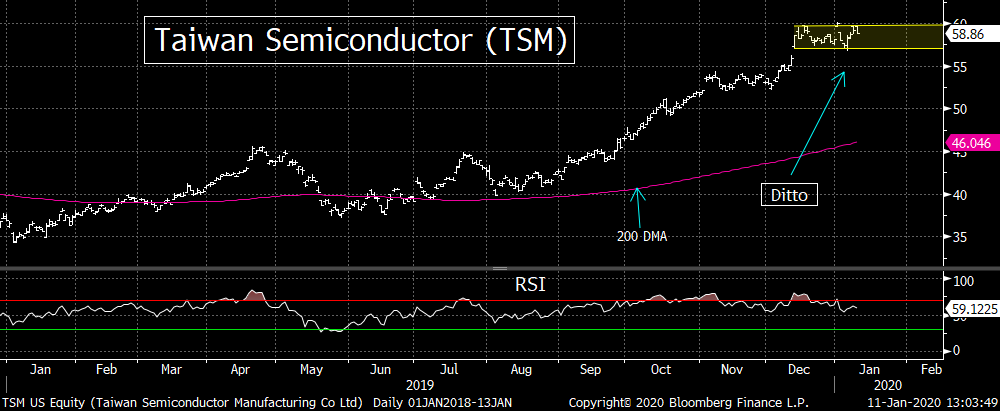

---5) Believe it or not, the chip stocks have been underperforming over the last month. That’s right, the SMH semi ETF has rallied “only” 1.8% vs. a more than 6% rally in the broad XLK tech ETF (and +3% in the S&P 500). This is NOT a major problem…given how well the group outperformed for much of last year. However, the group did get quite overbought recently…and thus could be do for more of a pull-back…rather than just a sideways “breather.” TSM’s earnings (Thursday) could/should give us a good idea of how things will break in this group over the near-term.

Long Version:

---1) The Federal Reserve is providing ample amounts of liquidity through their “not QE” QE program. We’re not sure if you really need to know anything else over the near-term. That said, QE programs in the past HAVE seen pull-backs that were much larger than the recent 0.7% decline we saw right after the attack on Iran’s top military leader (Soleimai). Therefore, those looking for a continued rally straight up from here are throwing caution to the wind…..More importantly, since this rally is being fueled almost entirely by Fed liquidity, it’s going to end very badly on a longer-term basis….especially if the rise does not end soon.

We have been doing this too long to believe what some pundits are trying to argue today. We keep hearing why higher valuations will be justified (even though interest rates cannot move much lower...without killing the banking system). We hear why improve technology will keep inflation low forever. We also hear some pundits try to say that earnings growth of mid-to-high single digits is “great”. (Those kind of earnings are not “great”…when they come after a 30% rally on zero earnings growth.)…..In other words, these pundits are trying to say “it’s different this time”…without using those exact words. (They don’t to use those words….because those who used them 20 years ago ended up looking so foolish.)

However, it’s never different this time. Pundits (most of whom are paid to be bullish) will continue to do their best to keep investors in the markets…because once it rolls over, everybody will go over the waterfall together. These pundits figure they won't get too much grief because most of them have all said the same thing. They’ll all say that “nobody could have seen this coming.” That’s what they said after the credit crisis. Heck even Ben Bernanke tried to day that. However, some people DID see it coming…just like some people did in 1928 and 1999......Basically, these pundits know that if they turn bearish, they'll lose their jobs...and when they're wrong in a colossal way, they'll be wrong with everybody else, so it won't matter (and they'll keep their jobs).

No, we’re not trying to say that today’s market will be followed by the kinds of major bear markets we saw from 1929-1932, 2000-2003 or 2007-2009. However, we ARE warning investors that this is not a healthy market. The underlying fundamentals have not been strong enough to justify this rally…and therefore, when it ends, it’s going to end very badly…not just another mild correction.

To end our opening point this weekend…which is designed to warn investors of about buying too aggressively in today’s stock market…we’ll also say that the Fed will not always have the market’s back. People keep calling the Fed’s tightening policy of a couple of years ago a “mistake.” They argue that economy was not strong enough to handle that kind of tightening. Those people are dead wrong.

Yes, they made a “mistake” if you believe the Fed’s goal is to always keep the stock market rallying, but we do not believe that is their goal for a second….The entire purpose of the last Fed’s tightening cycle had nothing to do with inflation and nothing to do with an overheated economy. In fact, much of the reasoning behind why they engaged in that tightening cycle was in order to slow the rise in asset prices. They didn’t (and don’t) want asset prices to go too high…because they will lose their ability to control a down-turn…like they almost did in 2008.

Even though many people believe that the Fed will never let a recession take place again…and that they want to prevent any bear markets in the future, we believe that their goals are very different.......We believe they will not let another bubble inflate to the degree it did in 1999 and 2007. So investors had better be prepared IN ADVANCE for a serious decline in the stock market at some point in 2020. You don’t have to ACT on that plan now, but if you have one in pace IN ADVANCE, you will be able to avoid losing your head when others around you are losing theirs.

---5) As we all know, several very important tech stocks have continued to rally strongly into the New Year (which we touched-on in terms of AAPL in point #2). However, believe it or not, the semiconductor stocks have actually underperformed the broad tech group over the past month. That’s right, since December 12th, the SMH semiconductor ETF has rallied only 1.8%!!! That compares to a more than 6% in the broader XLK tech ETF (6.13% to be exact)!!! (BTW, the S&P 500 index has rallied just over 3% over that time frame.)

No, this is not a major development…at least not yet…but it IS STILL something we need to keep a close eye on…especially as we move through earnings season. The recent action of the chip stocks over the past month would be much bigger concern if it had actually declined. Instead, it’s underperformance has involved being stuck in a sideways range…with a slight net gain…not an alarming drop. Given the groups fabulous performance throughout most of 2019, the fact that is has underperformed for a while is not a glaring problem (especially since it has not rolled over).

Earnings season for the semis begins this Thursday…when Taiwan Semiconductor (TSM) reports. TSM has the largest weighting in the SMH (13.3%), so if it’s earnings come-in much differently than expected (in either direction), it could/should have an impact on the entire group. Don’t get us wrong, there are many chip stocks that will continue to have an important influence on the group going forward, so we’re certainly not saying that TSM’s earnings report is a “make or break” situation for the SMH. We’re just saying that both the SMH & TSM have been trading in a fairly sideways range over the past month…and if they break-down below those ranges, it could cause some short-term investors/traders to take some profits in the group.

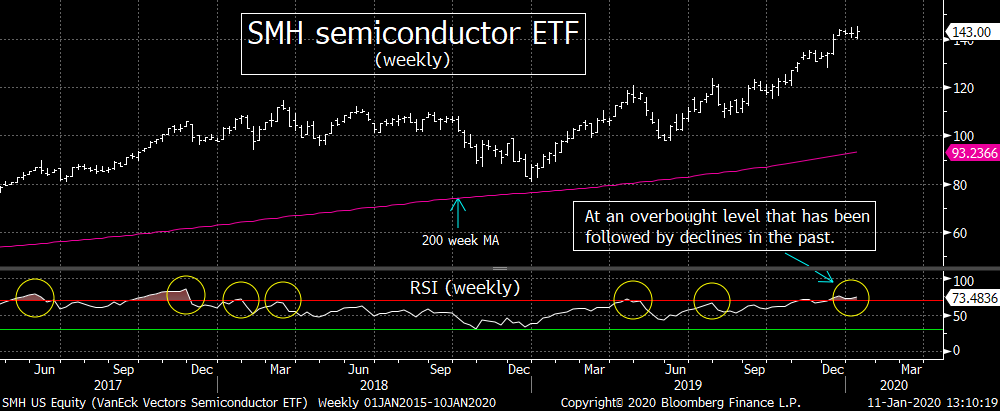

Again, since the group was SUCH a good one in 2019, a pull-back (or even a correction) would not be a big surprise…and it could actually be seen as normal and healthy. Let’s face it, the SMH saw TWO corrections last year (of 18% in April/May…and 12% in July/August)…and its weekly RSI chart has reached a level that has been followed by pull-backs/corrections in the past. Yet the semis rebounded to new highs on both occasions (AFTER they corrected), so long-term investors can take solace in the group's recent history. However, if (repeat, IF) the SMH does indeed break-down…due to some earnings reports or anything else…it will probably weigh on the rest of the tech group…and the broad market in general…at least for a little while.

Matthew J. Maley

Managing Director

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464