THE WEEKLY TOP 10

Quick Note: I will be participating in the next "MoneyShow Virtual Expo" that runs from October 27-29. I will be presenting early in the afternoon on October 28th and I hope you will join me. They have a fabulous line-up with people like Steve Forbes, Ed Yardeni, Kristina Hooper, Peter Schiff, Gene Munster and Steve Moore. I will be talking about the benefits of both long-term and shorter-term investing...and how using a portion of your investment money to take advantage of signifiant short and intermediate-term moves in the market place can help maximize one's returns and one's long-term investment goal. I hope you will join me and the rest of the presenters in two weeks. It should be a very informative three days.

THE WEEKLY TOP 10

Table of Contents:

1) Last week action bodes well for a further pre-election rally in stocks.

2) Longer-term this very expensive market is going to have a tough time rallying a lot further.

2a) The present fiscal plan is already priced-in...and a second one will be back-end loaded.

3) A crack has developed in the all-important trucking stocks.

4) Watch the currency markets (DXY...and AUDJPY) for clues on the stock market.

4a) That said, some correlations can (and do) change over time.

5) A look at the key support/resistance levels on the mega-cap tech stocks.

5a) Their MACD charts could be very important going forward as well.

6) The European banks are still a big concern for us.

7) Consumer staples & utilities acting quite well. That’s actually bearish.

8) China/Taiwan is going to be a HUGE issue next year. Be prepared!

9) Growing disgust for political candidates...AND the political press.

10) Summary of our current stance.

Short Version:

1) A week ago, we said that the upcoming week was going to be a very important one for the stock market...and the way things developed as we moved through the week bodes very well for a further rally going into the election. In other words, the quality the “internals” during the mid-week pull-back/breather were quite good...and that should be setting us up for further gains into early November.

2) Despite the fact that we’re more constructive on the stock market over the near-term, we want to reiterate our stance than any near-term rally will not be underpinned by the kind of fundamental growth that will justify much further gains over a longer-term period. Earnings estimates for 2021 are flatcompared to 2019 AND 2018...and “multiple expansion” is hard to achieve when we’re already at 21x earnings and rates are at 0.7%.

2a) We’d also argue that much of a new $2 trillion fiscal plan is already priced into the market. The first one was passed when the market was 35% lower and consumption had come to a halt. This one is coming when the market is at all-time highs and expectations are that consumption will continue to grow.....Also, history tells us that if we get another stimulus package in 2021, it will likely not kick-in to a large degree until later in the next President’s term. (Believe it or not, Ronald Reagan’s first term is actually a good example of this.)

3) We have been watching the truckers this year because they were a great leading indicator for the better-than-expected economic rebound of the early Spring lows. On Friday, JBHT reported disappointing earnings...which led to a severe drop in both the stock and the group. If (repeat, IF) this group continues to decline, it could be a signal that the trajectory of this economic rebound is flattening out. Thus we’ll continue to watch JBHT and the rest of the truckers closely over the coming days and weeks.

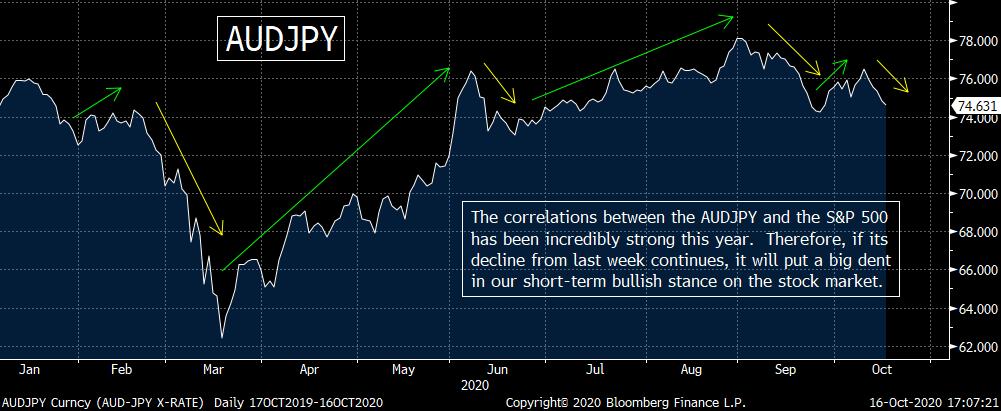

4) The movement in the dollar since May has been a GREAT contrarian indicator for the stock market.....Even though we think we’ll see more dollar weakness eventually (and in 2021), the “positioning” in the dollar is still extremely short. Therefore, it could rally further over the near-term...which, in turn, should be bullish for stocks (again, over the very-near-term).....However, we’ll also be watching another area of the currency markets...the AUDJPY. This has been a great indicator for the “carry trade”...and it’s looking weak, so that could cause problems for stocks at some point going forward.

4a) We just want to take a quick second to point out that the correlation between the dollar & the U.S. stock market is a very uneven one over time. We’re merely pointing out that it has been a strong (contra) indicator in recent months. At some point the correlation will change...and even completely reverse.......In other words, the dollar has been an inconsistent indicator for the stock market historically, so it is not at the very top of our list of indicators right now, but we’ll still be keep an eye on it.

5) Mega-cap tech....We’ve been saying these stocks will be fine, BUT that people should pare back their holdings a bit and rotate to some other tech areas (like the cloud). What if we’re wrong? What if they are going to take-off again...OR what if they’re going to fall out of bed? Well luckily, the resistance/support levels for these names are well defined, so if any of these stocks break either of those lines, we’ll know right away. In the “Long Version” below, we highlight those key resistance/support levels for each of the FAANMG stocks.

5a) We’re also watching the MACD charts on all of these stocks. We only provide the chart on AMZN (so that we don’t inundate you with FAANGM charts), but they’re all very similar. If one or more of them sees a negative MACD cross soon, it will give those crosses a “lower-high”...which will not be good at any of those stocks on a technical basis.

6) The European banks continue to have problems. Investors are now worrying about their sovereign debt holdings once again...as well as the impact of another lock-down in that part of the world. The STOXX Europe 600 bank index is down back within 5% of its $80 “line in the sand” level...which, if broken, will be VERY bearish for the European banks on a technical basis.

7) Back in January, we highlighted the outperformance of two defensive groups (consumer staples & utilities) as a reason to be concerned with the rally at that time...because that kind of outperformance had been a warning signal for an upcoming top of significance in the past. Well, sure enough, they’ve been outperforming recently once again. Thus if these defensive groups continue to rally, it should raise concerns in investors’ minds.

8) We still (strongly) believe that one of the biggest threats to the markets and the economy once we get into 2021 is going to be the situation in Taiwan...and the U.S./China relationship. No, we don’t think that the coronavirus is going to go away as an important issue after the election...or after we move into the New Year. However, as we have all been focusing on the pandemic and the election, the situation in Taiwan continues to escalate. We are a long way from being on the brink of anything, but the tensions continue to rise...so we want to keep investors’ attention on this issue.

9) The unethical moves by Facebook and Twitter late in the week...and the ridiculous bias shown in the “Town Halls” at the same time...most likely gave the President a boost to his chances for pulling a rabbit out of a hat once again. It also raised the odds that the GOP can hold the Senate as well. However, it’s Biden’s election to lose......Since we’re disgusted with both the political candidates AND the political press, we’ll leave it there this weekend.....Next weekend, we’ll take a close look at the key battle states...and what is likely to happen in each one of them.

10) Summary of our current stance......The quality of the “breather/pull-back” we saw in the market mid-week last week tells us that the recent rally off the late September lows will continue through the election. However, we do not think a Biden victory or a blue wave will be bullish on an intermediate term basis. We also believe that fiscal plan that is being negotiated right now is already priced into the market...and that any new fiscal stimulus that might come from a new Administration will likely be back-end loaded. Therefore, we think 2021 will be a tough year for the (very expensive) U.S. stock market. As for the time between the election and the end of the year, it should be quite volatile. Therefore, investors and traders will want to remain nimble over the last two months of the year. As we move closer to the end of the year, investors should start to start to raise cash and get more defensive.

Long Version:

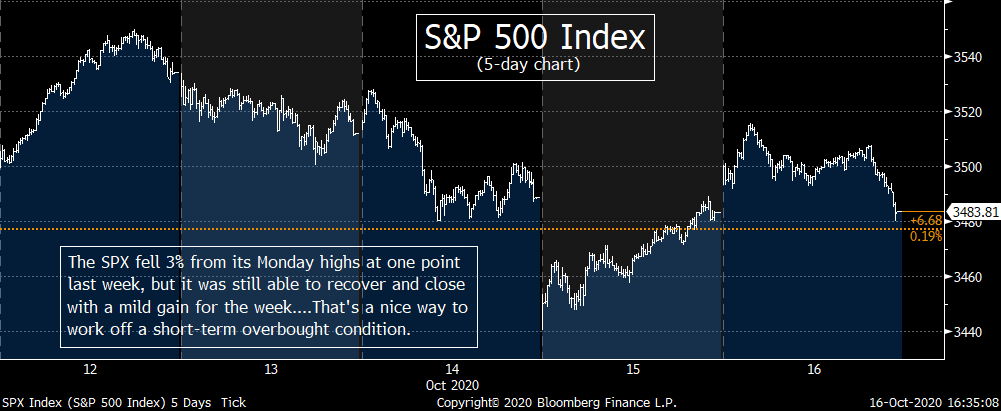

1) A week ago, we said that the upcoming week was going to be a very important one for the stock market...and the way things developed as we moved through the week bodes very well for a further rally going into the election. After a sharp (options-induced) rally during Monday’s quasi-holiday session, the stock market then engaged in the kind of decline that we were expecting...due to the fact that the market had become overbought on a very-short-term basis late in the previous week. As we said last weekend, the “quality” of the upcoming “pull-back/breather” in the stock market was going to be very important. Well, the “quality” of the pull-back was quite good...and that set us up for the nice rally on Friday...and it should be setting us up for further gains into early November.

To be more specific, the declines we saw on Tuesday and Wednesday were not small ones, so they were not just slip blips on the radar screen. However, they came of VERY low volume (about 2.6bn shares on the composite volume)...and breadth that was quite benign. Then, on Thursday, the market fell for the third day in a row...and gapped lower by well more than 1% on the opening. However, that opening level was the low for the day...and the stock market was able to bounce-back strongly and retrace the vast majority of its opening decline by the end of the day. On top of this, the breadth was actually positive on all of the major indices for the day!

We’d also note that we’ve seen a big change in the “gap-down” openings recently. During the September correction, when the market saw a gap-down move, it continued to decline after the opening on many occasions. However, since the late September lows, those gap-down openings have seen no downside follow-through as the day went on. Not only did we see this on Thursday, but we saw that on October 2nd as well. In other words, the “buy on weakness” crowd took a short vacation during September, but they seem to have come-back strongly this month. Again, this bodes well for stocks near-term.

We do admit that a nice midday rally on Friday DID fade at the end of the day...and the S&P 500 & DJIA finishing with only mild gains...and the Nasdaq & Russell 2000 closing the day slightly into negative territory. However, Friday was an expiration day...and there were some artificial moves in the market that day. (The volume jumped a whopping 46% to over 3.7bn shares on Friday...so you can see there was a lot of artificial action that day.) Therefore, the disappointing late-day action on Friday should not be a problem going forward.

We’d also note that several of the uncertainties that were overhanging the market in September started to become “no lose” situations over the near-term. First of all, it is becoming more and more accepted that there will be no fiscal plan passed by the election...so if we DO get one, it should help the market rally further. Second of all, even though some pundits are trying to say that a “blue wave” will be positive for the markets, most people agree that a successful re-election bid by President Trump will be more bullish for the stock market. Therefore, if the polls start to show that the race is tightening up (like they frequently do as we get closer to Election Day), the market could/should be boosted by that news as well.

The one big risk, however, is that we if start to see a significant number of announcements about lock-downs in the U.S. and Europe due to Covid-19. There’s little question in our minds that we’ll hear more about this issue...given that places like London and Paris have already begun renewing some of the restrictions that existed in the spring. However, there’s also little question that things are not going to get a lot colder over the next 2.5 weeks, so the any negative impact from a second wave of the coronavirus is not likely to hit us in a powerful way until AFTER the election! Therefore, the odds that this issue will have a major impact on the stock market over the very-near-term are relatively low. The odds are not down to zero, so new-news on shut-downs around the globe could still create some headwinds for stocks, but it probably won’t have a pronounced impact until later in Q4.

Finally, before we move on with this weekend’s piece, we want to emphasize that our positive stance on the stock market is only a near-term one...leading into the election in 2.5 week. As you will see in our other points, we see further risks going forward, but after seeing the action during last week’s “breather,” the line of least resistance is still higher for the rest of October.

2) Despite the fact that we’re becoming more constructive on the stock market over the near-term, we want to reiterate our stance than any near-term rally will not be underpinned by the kind of fundamental growth that will justify the gains over a longer-term period. Therefore, the odds that we’ll see another serious correction in the stock market over the next 6-9 months is very high...and thus the risk/reward equation in the stock on a longer-term basis is much more skewed to the risk side of things than many pundits (most of whom are paid to be bullish) are telling you right now.

Let’s review a few facts. First, when the S&P 500 was topping out in February, it did so at a level that was 3% below where it’s trading right now. It had rallied almost 30% in 2019 even though earnings growth that year was ZERO!!!! Guess, what, earning expectations for 2021 are not better than they were in 2019!!! So the stock market is HIGHER than it was in early February...even though earning estimates for 2021 are no higher than the actual earnings were in both 2019 or 2018!!!!!

In other words, it’s very hard (for those who are not paid to be bullish to) to try to claim that a further rally of significance from current levels will be justified by the underlying fundamentals...when earnings will have gone NOWHERE for 4 years and yet the stock market has rallied more than 30%!!!! The existing fundamentals and the future potential fundamentals have already been priced-in!!!.....Of course, some pundits can always try to say that the market will rise further due to “multiple expansion”....but that’s really only saying that the market will rally further because it’s going to get more expensive. That doesn’t mean that the market cannot see a further rally of some significance. However, it DOES mean that a further big rally will not be justified by the fundamentals...and it will lead to a very ugly bear market eventually.

With all of this in mind, we believe that the upcoming rally further in the stock market before the election...and any further short-term pops over the rest of Q4 and into Q1 of next year...will provided great opportunities for investors to take some chips off the table...and rotate in to some more defensive areas in the stock market (and rotate withinthe tech sector for those who are still overweight the mega-cap tech names).

2a) We also have questions about how much of a $2 trillion fiscal stimulus package is already being priced into the stock market. First of all, much (most) of that stimulus will not be additive. It will only allow people and small businesses to maintain some sort of level of consumption...a level that will still be below the pre-coronavirus level. In other words, the first rush of stimulus was very bullish for the stock market...because the stock market was trading 35% lower than it is today...and was pricing-in an incredibly low level of consumption for an extended period of time!!!! Now, it’s pricing in a continued high level of consumption, so it’s hard to think that a new stimulus package will have anywhere near the same kind of impact...even if it’s a very big one.

Besides, one of the big reasons for the rally off the late September lows has been the re-thinking behind a fiscal stimulus package before the election. Back in July and August, everybody assumed that there would be a fiscal stimulus package passed by the end of the summer...and that was one of the catalysts for a further rally. NOW, people are saying that one of the reasons the market will do so well next year is the new $2bn stimulus that will be passed after a “Blue Wave.” We DO understand why the somebody could “recycle” the fiscal stimulus issue as a reason for a rally...because the stock market declined 10% when the consensus went from assuming a plan would get passed this year...to assuming the issue was dead until after the election. Therefore, it makes sense that renewed speculation (and/or hope) that we’ll get a deal sooner or later would spur a rally off the lows. However, now that the market is back up near it’s all-time highs, how does that fiscal stimulus give the market another boost...when it’s already priced into the market????

This is why we continue to believe that a Blue Wave will create a headwind for the stock market in 2021. As we have highlighted a lot recently, if history is a good guide, even if we get yet ANOTHER NEW stimulus package (on top of the one that is being negotiated right now...and is already priced into the market), it will almost certainly be back-end loaded (to help the Dems get re-elected in 2024).

Again, it’s safe to say that if the stimulus plans that are being negotiated right now are not passed, we’ll certainly get a $2bn+ package if the Democrats sweep. However, THAT stimulus is already priced into the market. Therefore, people who are saying that the market will rally a lot next year due to the $2bn stimulus the Democrats will pass...are merely recycling what has already been priced into the market....and those looking for another fiscal package to do the trick will probably have to wait longer than they realize right now.

Maybe the long-term bulls ARE right. Maybe recycling $165 in earnings for the S&P 500 every year for four years has been one of the reasons the stock market has been about to rally 32% since the beginning of 2018, so why can’t recycling the same stimulus several time fuel a further rally as well??? However, this madness is going to stop at some point...and we think the first year of a new Presidency will be a likely time for that to happen.

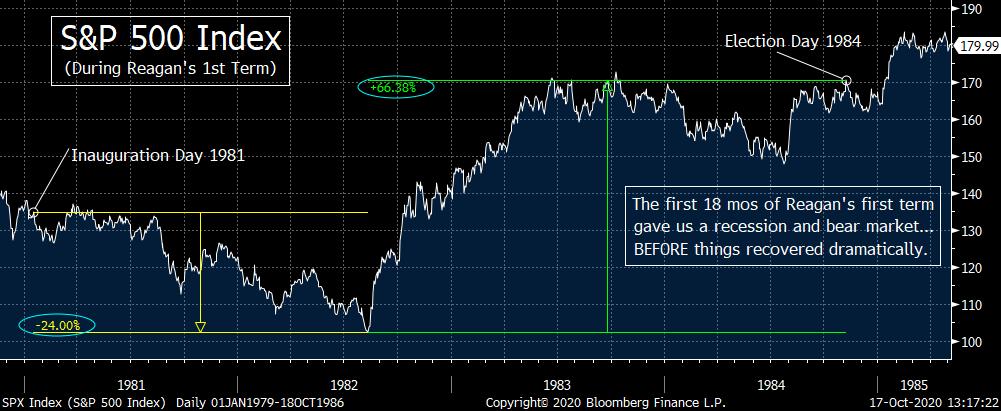

Voters decided to give an outsider a chance in 1976...but they threw-out Jimmy Carter after just one term. This was followed by a big resurgence in the American economy. Therefore, maybe throwing out another outsider (Donald Trump) after just one term will help the America regain its economic greatness as well. However, we should all know that the S&P 500 fell 25% from the beginning of 1981 (when Reagan took office) until the middle of 1982...BEFORE it rebounded 65% to new all-time highs by his re-election year of 1984!!!!!

Ok, ok...we realize that comparing what Reagan did...to what Biden will likely do...is a big stretch. However, history tells us that it takes time to turn things around after a deep economic down-turn. In fact, history also tells us that new administrations purposely set things up so that the rebound will not hit its full stride until the last two years of their first term. (As President Trump has learned, it’s way too hard to keep the economy hitting on all cylinders for all four years. To many things can go wrong...so the smart ones try to set things up in a way that the economy is booming at the end of their first term, NOT at the beginning!) Besides, they can always blame the previous President for problems early in their first term.

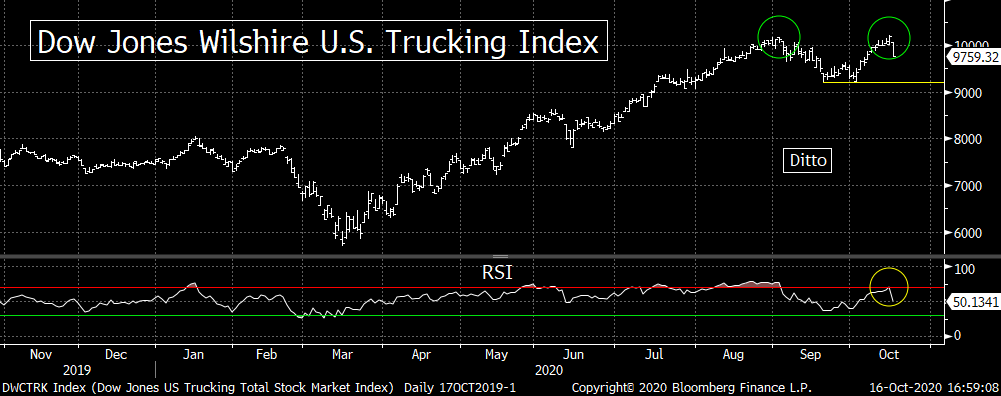

3) There was a big scare in the Transportation sector late last week...as one of the truckers, JB Hunt (JBHT) reported disappointing earnings on Friday. This knocked down the stock by almost 10% that day and led to a 4.3% decline in the DJ Wilshire Trucking Index and a 1.2% drop in the DJ Transportation index......Long-time readers know that the truckers have been a group has been an important one to watch this year...and thus we have played close attention to it...and will continue to do so.

JBHT stood more than 90% above its March highs before they reported earnings , so this decline could merely be something that is working-off an overbought condition in the stock. (The same could be true for the DJ Trucking Index...which was 77% above the March lows at last week’s highs.) However, 9% declines are not the kind of one-day declines that merely work-off extreme technical conditions. (The main reason for the decline seems to derive from their intermodal business lagging in the domestic market. Intermodal business involves the moving of parcels using two or more types of transportation (truck, rail, etc.) and expectations had been that this would be an area of growth for JBHT. So that fact that it lagged raises some concerns about the truckers...and the rails as well.

Having said this, the Cass Freight Index for Shipments saw a nice sequential (7%+) rise in September...and now stands almost 30% above its April lows. Also, Dr. Copper continues to hold-up quite well...and that commodity stands at its highest level since 2018. Therefore, the substantial declines JBHT and the trucking stock index experienced on Friday may indeed just have been due to their huge gains in recent months....and not to a significant change in demand in the U.S. or global economy.

However, since both JBHT and the DJ Wilshire Truckers index could be forming important “double-tops”...and since “double-tops” are frequently followed by substantial declines...we’ll be watching these two assets quite closely as we move through the rest of the 4th quarter. If they follow Friday’s deep declines...with a break below their early October lows any time soon...it’s going to raise a big yellow warning flag on the truckers. This will be especially concerning (IF it happens) given our concerns about what kind of impact any renewed lock-downs might have on the economy as we move through the all-important holiday season.

In other words, the outsized rally in JBHT (and the truck stocks in general) was a great indicator that the economy was going to come out its deep winter/spring slowdown much more quickly that most people had been thinking 6-7 months ago. Therefore, if these names continue to decline in a meaningful way over the coming weeks, it could/should be a signal that the trajectory of the recovery is going to flatten out in a more compelling way that the consensus is thinking right now. Therefore, investors (and economists) should be watching this sector closely going forward.

4) I has been interesting to see how strong the inverse correlation between the dollar and the stock market has become over the past 6-8 months. It started back in May, but the relationship has only strengthened as we’ve moved through the summer and into the fall. In fact, it’s become almost tick for tick in recent weeks. (Before we go into more details, we to say that in point 4a below, we discuss how things like the dollar can and do shift in terms of the types of indicators they are for the stock market, so investors need to remain nimble on these kinds of issue. Again, more on this below.)

Anyway, the movement in the dollar since May has been a GREAT contrarian indicator for the stock market (and for gold and other commodities as well). The drop in the dollar in May & early June went along with a further bounce in the stock market off the March lows. Then, a two week bounce in the greenback in the second half of June corresponded to a dip in stocks.

As we moved through the summer months, this (contrarian) relationship remained the same. A steady decline in the DXY dollar index during July and August corresponded very strongly with the nice rally in stocks we saw during those two months. When the dollar bounced in a meaningful way in September, the stock market fell in a significant way. Then...as we moved into this month...the dollar has slid lower again...and sure enough, stocks have rallied. (DXY dollar chart attached below.).....Heck, it was even a great indicator yesterday...as the strong one-day bounce in the greenback corresponded with the first down day in the stock market in five days.

We still believe that the “positioning” in the currency markets (especially the dollar and the euro) will make it very tough for the dollar to fall significantly more (and for the euro to rally significantly more) over the intermediate-term. The net positions in the dollar & euro in the COT data are just too extreme right now in our opinion for that to happen. HOWEVER, that does not mean that they cannot continue on their most recent trends (lower for the dollar, higher for the euro) over the near-term (between now and the election). Therefore, if the dollar can fall further, the stock market can certainly rally further over the coming weeks.

We also want to keep a very close eye on the Japanese yen as well. This has been a key indicator for the “carry trade” for a long time...and the weakness in the USDJPY and AUDJPY currency crosses last week coincided with the mid-week drop in the stock market. The AUDJPY has been a particularly important indicator this year, so we’ll be keeping a close eye on that one as well in the days and weeks ahead.

4a) We want to highlight that these kinds of strong correlations between the stock market and other assets are common...and can last for a long time. HOWEVER, these correlations (which are sometimes inverse correlations...like this one is right now) tend to eventually fade away. We remember a few years ago when the stock market traded almost tick-for-tick with crude oil for many months, but crude oil is now non-existent when it comes to moves in the stock market.

We’d also note that things like the dollar and crude oil are sometimes great indicators for the stock market and other times they are great contrary indicators (like the dollar is right now). We’ve seen many times over the past few decades when stocks traded lock-step with these other assets...and many times when they’ve traded in opposite directions. (And we’ve seen times when the stock market ignores these other assets classes.) Therefore, following the dollar will work...until it doesn’t...so we need to be careful when we follow indicators like these.

5) We have spent a decent amount of time recently suggesting that investors should pare-back their exposure to the mega-cap tech names (that’s “pare-back”...not “dump” the shares completely) and look to “rotate” WITHIN the tech sector. We believe that the cloud computing area is still in the early innings of its long-term bull market, so that should be a good area to rotate towards over the coming weeks. Therefore, investors should use rallies in the market to cut back their exposure to the FAANMG names...use pull-back to add exposure to the cloud.

In other words, we believe the mega-cap tech names will be fine...we just don’t think they outperform to the degree they have in the past. However, what if we’re wrong? They could regain their incredible leadership status (due to another serious lock-down?)...OR they could fall out of bed and get hit much harder than we are thinking right now (due to larger than expected regulatory issues?). Luckily, the levels to watch in terms of BOTH of these possibilities are well defined for each of the mega-cap tech stocks.

With this in mind, we thought we’d review these key support/resistance levels on all of the FAANMG names. The charts we’re about to present are not overly intricate at all. Sometimes technicians try to make things more complicated than they need to. In the case of these stocks...at least right now...their support/resistance levels are not complicated at all. Therefore, these charts should be a good resource to go back to in the coming weeks...as we go through what could be a very volatile period of time.

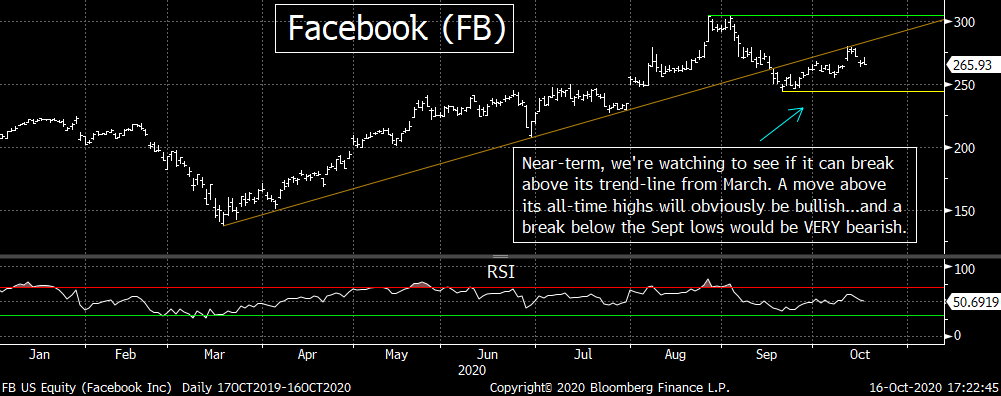

We’ll go in order...starting with Facebook (FB). The support/resistance levels on FB are pretty straight forward...they’re the lows and highs from the second half of the summer. However, the other line we’ll be watching is the trend-line from the March lows. That comes-in at $280 right now. If it FB can break above that level, it will be bullish and if it fails at/near that level will obviously be bearish. However, the major resistance level to watch is $304...the highs from late August and early September. The important support level is $248...the lows from early August and late September. Any significant moves above/below these key levels should be followed by significant moves, so we’ll be watching these levels very closely over the rest of this year.

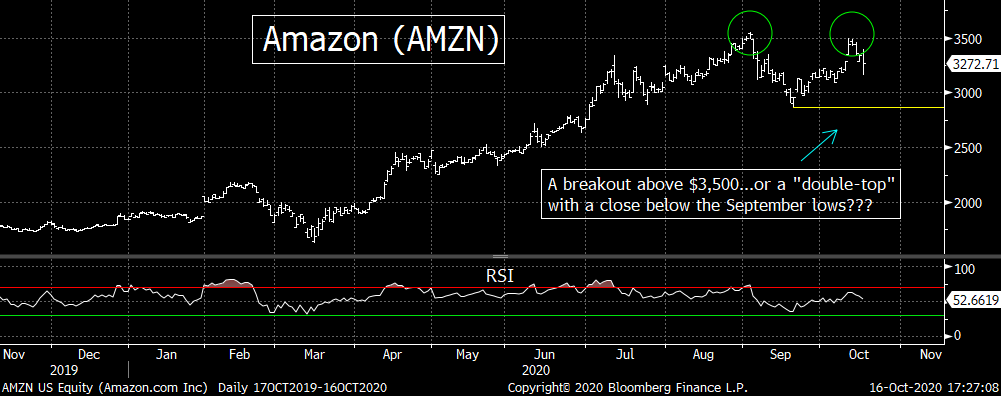

Amazon (AMZN).......AMZN is actually one name that is trading near a critical level. The 3,500 level is the high from both early September and early this past week. Therefore, it could be making an important “double-top.” Since it made a major “double-top” in 1999...just before the stock fell out of bed in a powerful way, a meaningful failure at this level would not be good at all. However, if it can break above the $3,500 level in any meaningful way, it’s going to be quite bullish for the stock.......Of course, the stock could churn around for a while, so we don’t want to try to say that the stock is about to see a major move. We’re merely saying that the potential is high...and we’ll be watching how AMZN plays-out over the next few weeks.

Apple (AAPL)......Although it broke below its trend-line from the March lows for a couple of days late last months, it has been able to regain that line (as well as its 50 DMA). We are a bit concerned that it dropped 5% from its Monday highs last week, so we’ll be watching to see if it can continu

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464