I was out of the office and out of contact with the markets on Thursday and Friday in order to attend a memorial service. Therefore this weekend’s piece will be quite a bit shorter than usual...and there will only be one “version” (plus a “Table of Contents)......The format is also a little different in another way this week. I’ll be putting the “Summary of our current stance” in point #9...instead of #10 like I usually do. In this week’s final bullet point (#10), I’ve included a great story about Art Garfunkel that a very good friend of mine sent to me this morning. It won’t take you very long at all to read it, so I hope you will take the time to check it out. It’s a very inspirational...and I thought we all need stories like these in the crazy times we live in right now.

Finally, as a reminder, I will be presenting at the MoneyShow's Virtual expo in two weeks. Click here to sign up for this conference for free. Thank you and I look forward to the Show! Thank you very much.

THE WEEKLY TOP 10

Table of Contents: 1) The stock market usually rallies just before the Presidential Election. 2) A move to 1% on the 10yr note yield would signal an important change in trend. 3) Any further steepening in the yield curve would confirm a change in trend as well. 4) Banks looking to breakout, but not quite there...yet. 5) The dollar acts very poorly, but its “positioning” is still bullish near-term. 6) AAPL at a key technical juncture. They report earnings on Thursday. 7) Bitcoin breaks out, but it’s quite overbought on a very-short-term basis. 8) Politics.....Contested elections? Self pardons? You can’t make this stuff up! 9) Summary of our current stance. 10) “Hello Darkness My Old Friend.”

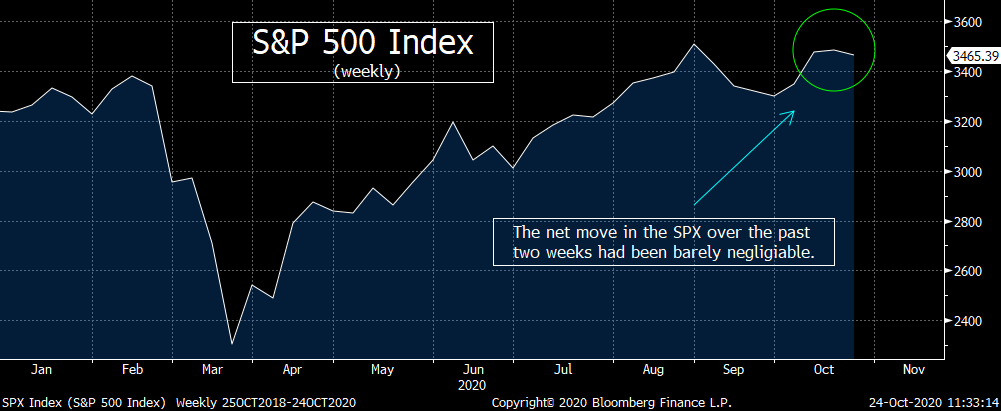

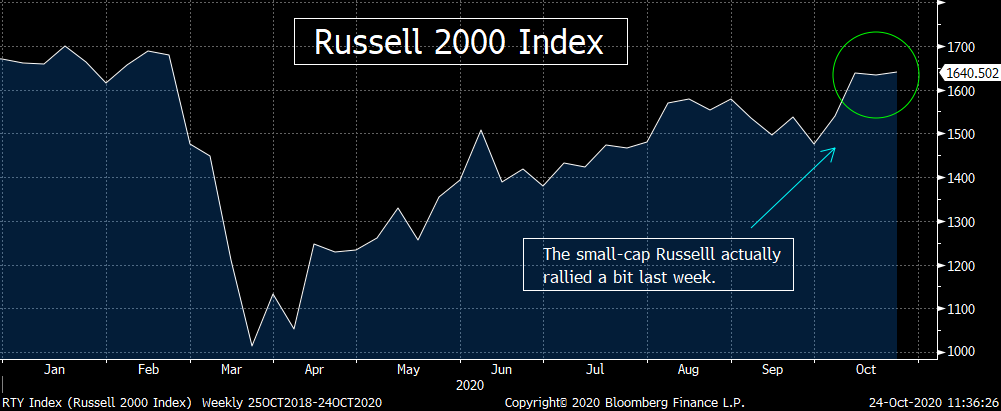

Long (and only) Version: 1) The stock market did not see any upside follow-through from the previous week’s positive action last week, but it certainly didn’t get hit hard at all. In fact, it both the S&P 500 and Nasdaq Composite closed almost exactly where it stood two weeks ago...and the small-cap Russell 2000 actually closed the week with a mild gain. We’d also note that the S&P 500 equal weight index and the NYSE Cumulative Advance/Decline line both saw gains last week as well. We do have to admit that the all-important SMH semiconductor ETF fell 1.3% last week, but that’s hardly a disaster...and the HYG high yield ETF saw a mild gain. So even though the S&P saw its first down week in three weeks, it’s not something that would raise a yellow warning flag by any means.

It is interesting...although the stock market fell 1.9% over the seven days of trading in 2016, you have to go all the way back to 1988 to find another time when the stock market did not rally over the last week and a half of the election campaign. (In other words, from the second-to-last Friday before the election...until Election day.) Yes, we have seen the last stock market dip in mid-October several times, but until 2016 it had been almost 30 years since the market did not rally during the last full week before the election and the first two days of the actual week of the election. The average return since 1988 was 3.8% in those up six examples from 1988 to 2012. We do admit that that 3.8% average is skewed by the big 10% gain we saw in the fall of 2008...when the stock market was seeing some HUGE swings...but the average is still +2.5% if you exclude that one year.

Of course, this year has been ANYTHING but normal....and nothing is ever guaranteed in the markets...but our point is that history does tell us that the odds are high that the market will rally between now and Election Day. Based on the action in the stock market we’ve seen over the past two weeks (including the “internals” of the market)...it seems to us that it will take some serious new-news to fuel a significant decline over the next week and a half...and the line of least resistance is higher over that time frame.

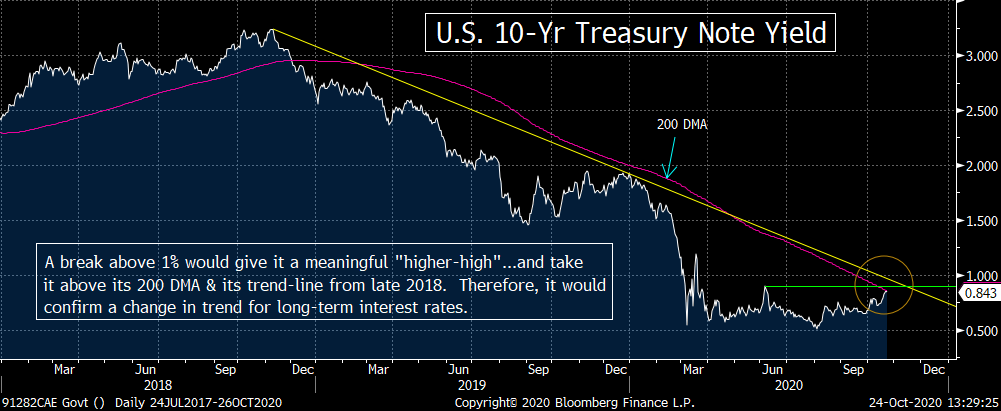

2) The yield on the U.S. Treasury note got very close to the 0.90% resistance level we’ve been harping on recently on an intraday basis on Friday...before pulling back a little bit. That level was the closing highs from June (on both a daily and weekly basis). So a move above 0.9% would give it an important “higher-high” and thus would be quite bullish for long-term Treasury yields (bearish for their prices) and so it will be a very important level to monitor over the coming days and weeks.

However, we always want to guard against a “head fake.” Therefore, the 1.0% level on the 10yr note is something most people will be watching more closely. Not only is a round number...and thus it will get more headlines...but a rise to that level would confirm that a “higher-high” has indeed been made. More importantly, a move above 1% would also take it well above its 200 DMA...AND above its trend-line from late 2018! Given that the yield had been trading in a sideways range for eight months going into October (thus forming a nice “base”), at move above the 1% level would confirm a change in the intermediate-term trend for long-term interest rates...EVEN THOUGH they’d still be very low on an historical basis.

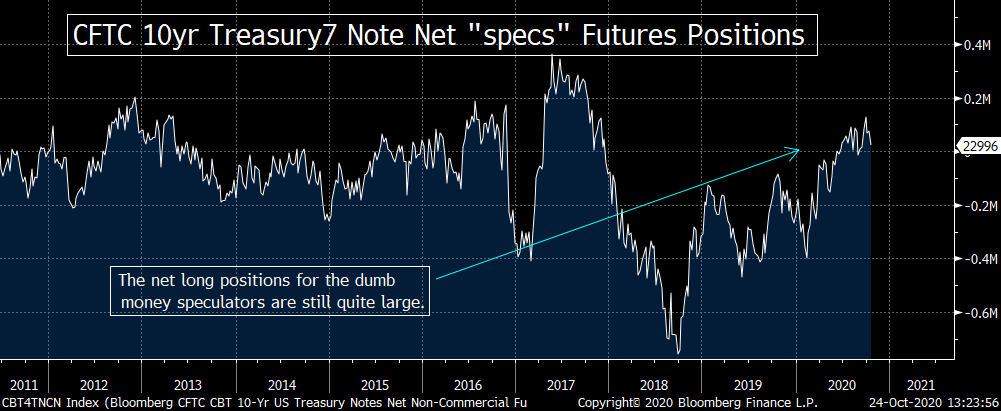

Finally, we’ll highlight that we’re finally seeing a mild change in the positioning by futures traders in the COT data...but it’s still pretty extreme and thus conducive to a further decline in bond prices and a further rise in yields. Also, the bullishness in the DSI data is firmly in the 50% range...so it’s not extreme at all. So it’s not out of the question that 1% could be reached sooner rather than later.

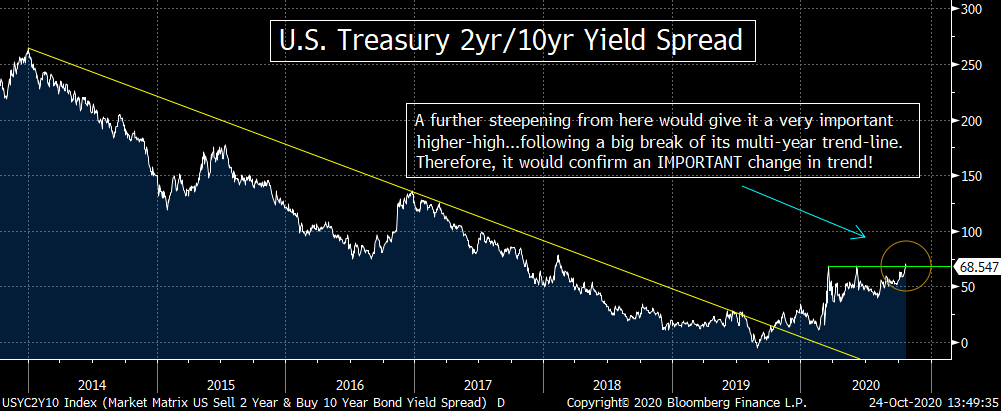

3) We’d also note that the yield curve stands at an important technical juncture. The 2yr/10yr spread stands at 68.5 basis points as of Friday’s close. That’s slightly above the highs from both March and June of 68 bpts. Therefore, if the curve steepens more going forward...and makes a more meaningful “higher-high” (“steeper-steep”)...it will be confirmation of a VERY IMPORTANT change in the trend of the yield curve...because it has already broken above its trend-line going all the way back to the beginning of 2014 in a substantial way!!!

4) These moves in the Treasury market have been quite positive for the banks stocks. The KBE bank ETF rallied 6.4% last week...and has gained over 20% in the last three weeks! Looking at the chart, this move has taken the KBE well above its “symmetrical triangle” pattern...and has it testing its August intraday highs. (It has already broken above its closing high from August...as well as its 200 DMA.) Therefore there is no question that the group is finally looking good...especially since the Treasury market acts in a way that is conducive to a further rally.

Having said all this, the RSI chart on the KBE is getting overbought. In fact, it has reached a level that has been followed by meaningful pull-backs over the past three years. This is particularly important because we still think the dollar has another rally-leg left in it (more on that in the next bullet point). Therefore, it wouldn’t surprise us if the banks did not see a major breakout quite yet. It might (and we think probably will) need to see a short-term pull-back before it move higher.

However, if the KBE does break above $35...and especially if it can break above its June highs of $36.65 (either now or after a pullback)...it’s going to finally give the banking stocks the kind of upside technical momentum they haven’t seen is many years.

5)Speaking of the dollar, it really doesn’t act well at all. It tried to experience a mini-breakout in late September, but that stalled-out quickly...and the greenback has been sliding lower since the very end of last month. This has taken the DXY dollar index below its 50 DMA...and within shouting distance of its August/September lows of 92.00. If it does break below that level in any meaningful way, it should be a signal that another important leg lower is upon us.

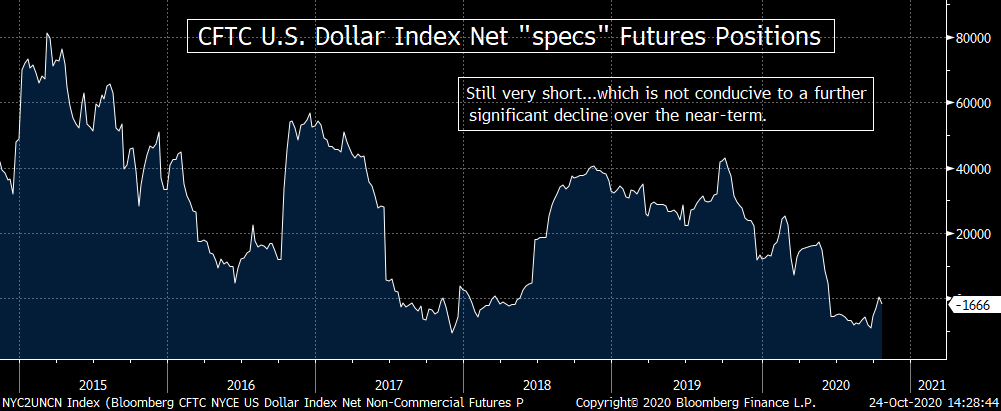

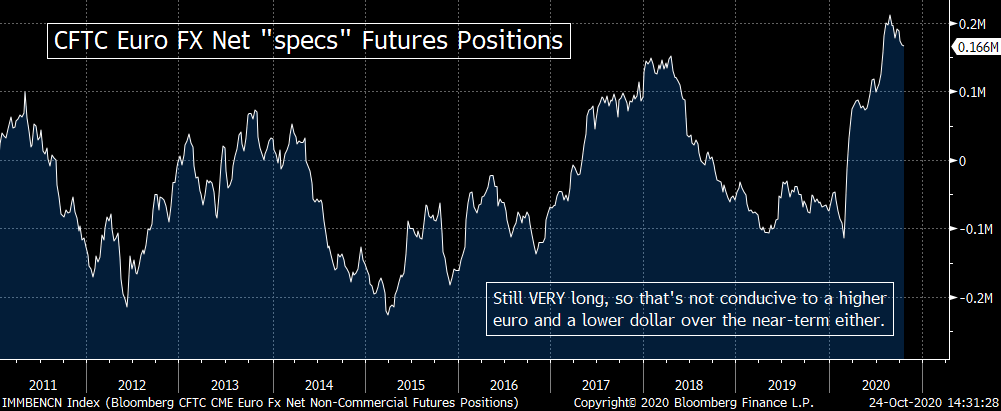

HOWEVER, as we alluded to in the previous bullet point, the positioning in the currency market tells us that a substantial decline from current levels is not as likely as the fundamentals might tell us...at least over the near-term. The net short position for the speculators (“specs”) in the dollar is still very, very large...and the net long position for them in the euro are similarly large.

When you combine all this with the uncertainty surrounding another wave of the coronavirus, the fiscal stimulus plan...and even the election...we could still see a lot of volatility in the currency market, the credit market and the equity markets before the next big trends for any or all of them become widely evident. That said, any significant break below 92 on the DXY is going to be quite bearish...no matter what the positioning is telling us.

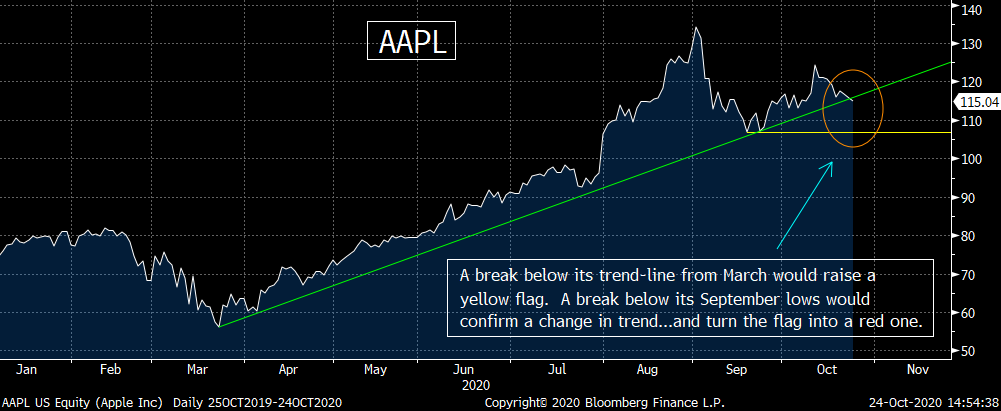

6) We think we’d all agree that AAPL is one of the most important stocks in the stock market...and it has come a long, long way from May/June of 2019...when many pundits were saying that the company was not longer innovative enough to help its stock outperform the market in any material way. Well, after a 210% rally from that time until its highs on September 1st, the stock made those nay-sayers from the spring/summer of 2019 look quite silly. (Of course, all of them turned bullish on the stock long before it topped out, but it was pretty amazing how many detractors this company had just 18 months ago.)

Having said this, this stock has not acted very well over the past two weeks. It has fallen 7.5%...and now stands more than 14% below its September all-time highs. In other words, while stocks like FB and GOOGL were all over the news over the past two weeks, their stocks have actually rallied nicely...while AAPL has continued to decline!

This disappointing action in AAPL is not a major problem...at least not yet. However, they DO report on Thursday...and the stock is now sitting RIGHT ON its trend-line from the March lows. Therefore, if (repeat, IF) their earnings/guidance are a catalyst for a further decline, it’s going to raise a yellow flag on AAPL on a technical basis......We readily admit that it would take a meaningful drop below the September closing lows of $106.75 to change the flag to a red one. Thus it’s going to have to fall another 7%+ for that to take place. However, if it did, it would confirm that its intermediate-term trend had changed from up...to down. Given how poorly it has acted over the past two weeks, a retest of those September lows is not out of the question.

In other words, this is a long-winded way of saying that AAPL’s earnings report (and the guidance that goes with it) could/should be VERY important for how the stock acts over the rest of this year. This is especially true given that a Biden victory could cause some added selling due to concerns over a change in the capital gains tax.

7) As you’ve all probably heard by now, Bitcoin broke above the key $12,000 resistance level we’ve been harping on recently...so that’s very positive for this cryptocurrency on a technical basis. The main catalyst was the news that Paypal was launching its own cryptocurrency, allowing people to buy, hold and sell digital currency on their site...but there are plenty of other reasons to be bullish on this asset class.

Looking at its chart, Bitcoin closed above both its intraday highs from 2019...AND above its highs from June 2019. However, it did not rally above the intraday highs from 2019, so that level ($11,850) could/should provide near-term resistance. We definitely tend to look at closing levels for guidance...rather than the intraday ones, but since Bitcoin is becoming quite overbought on a short-term basis, that level could/should still provide some near-term resistance.

Having said this, Bitcoin has certainly become more overbought before it saw a short-term or intermediate-term top in the past, so maybe it can climb into the $14,000’s before it sees a compelling pull-back. Either way, we are long-term bulls on Bitcoin and think it should be a part of everyone’s portfolio to one degree or another....we just think it will probably pull-back before long...and thus investors should hold-off being aggressive on the buyside after its recent jump. (Much more on this subject in the coming days and weeks.)

8) Politics......Every four years, this is the time that gets very exciting for me. I have always loved following politics...and this year has been one of the most fascinating of my life. However, it’s hard not to lose at least SOME enthusiasm this election year. “Trump fatigue” grew in a major way over the summer, but I still get very frustrated over the fact that these two candidates are the best we could do. So I believe both sides deserve the blame.

As frustrating as President Trump can be a lot of the time, there is little question in my mind that Joe Biden’s son benefited financially in significant way simply because his father was Vice President. In other words, the “insiders” in Washington DC are deplorable. Joe Biden might be the nicest guy in the world, but he does the same scumbag things that 95% of them do......On top of all this, the vast majority of people who cover politics for news outlets cannot be called journalists any more. They’re a complete joke. No, political bias by journalists is not a new phenomenon, but to see SO MANY mainstream political journalists engage in blatant bias is beginning to make the profession look ridiculous.

Anyway, we’ve talked a lot about what could happen in this election, but we’re going to stick with something we said at the beginning of the year. Even before the global pandemic wreaked havoc on the U.S. and global economy, we said that it was going to be tough for Trump to win re-election. He had won in 20116 by drawing a straight flush...and it was going to be very difficult to do it again. However, we ALSO said that although the states in the upper Midwest would indeed be important, the two most important ones were going to be Pennsylvania and Florida. If Trump can win those two states, he has a real chance of winning again. (We still believe Biden will win, but Trump still has a shot. He’s still the outsider...not Biden...and people are still sick and tired of the insiders in DC......Yep, I just used the word “still” four times in two sentences.)

If the outcome is close, it will definitely be contested. I won’t matter who seems to be the victor, a close election will be contested by the other side. That will not be good for the stock market.

The only thing we feel comfortable about predicting is that President Trump WILL pardon himself...whether now...or four years from now. His critics have been saying for months that the President should be ashamed for questioning the integrity of the electoral process. What he has said about mail-in voting and other aspects of the election is bad for the country, they declare........They might very well be correct. However, President Trump is not doing this because he thinks it will help him get re-elected. He is doing it because he wants to make sure he has the “cover” to pardon himself at some point...and it’s something he’s been working towards for many, many months.

None of what I have said here should be construed as evidence to which candidate’s policies are the ones I think would be best for the country or best for the stock market. I’m merely saying that I think Joe Biden will win...but the President still has an outside path to re-election. If Biden does win, I think President Trump will pardon himself.............It’s just my opinion about what I think WILL happen. It’s not a statement about my view on who should be elected...or whether I think a president should be able to pardon himself or herself.

9) Summary of our current stance......Since we were away from the markets late this week, we spent most of our time this weekend talking about the charts...and the shorter-term outlook for several different assets (although we did talk about the potential intermediate-term moves for such things as bonds, bank stocks, AAPL, some currencies & Bitcoin).

On a longer-term basis, our view has not changed. The stock market is WELL ahead of its underlying fundamentals...and we do not seeing those fundamentals playing catch-up with stock prices over the next few years to keep stocks rallying much from current levels. Could they go higher at some point between now and the first part of next year? Sure they could! However, we believe 2021 will be a tough year for the stock market overall.

First of all, a second wave of the coronavirus is likely to have a big impact on the economy in the first half of next year. That means that the “E” side of the “P/E ratio” is going to come down...which will make an already expensive market even more expensive if the “P” part of the equation remains the same. We also believe that history tells us that new presidents (and even second term presidents) tend to back-end load any stimulus to the second half of the term...so that they can get re-elected (or so that the party in the White House can keep their policies going after a second term). It’s too hard to keep an economy chugging along in strong way for 4 full years. Too many things can go wrong...as Mr. Trump has found out this time around.

Finally, we believe that the Fed does not want to push asset prices higher...to the same degree that they did after the financial crisis. For many years after 2008, the stock market was still quite cheap, so the Fed could continually push the markets higher with their liquidity without the fear of creating another big bubble. This time around...with the S&P trading at 21x 2021 earnings...a big rise in stock prices WILL cause another bubble. Since we already have a bubble in the corporate credit markets, the bursting of another stock market bubble will lead to the kind of melt-down that the Fed will not be able to control. Therefore, we believe that they will merely provide a safety net underneath the market (in order to keep the credit markets stable, open and working)...and not push asset prices higher in the way they have in the past.

If history is any guide, the market should rise between now and Election Day. This should be especially true if they pass a fiscal plan, but it seems that Sec. Mnuchin and Speaker Pelosi have become adept enough to keep “hope” alive for a while longer. Thus any failure to pass a deal in the next week will probably not hurt the market very much. However, after we move past Election Day, thing should become much more volatile than the past two weeks. That should be a great time for traders...and a great time for longer-term investors to set up their portfolio for what should be a relatively rough 2021.

10) “Hello darkness my old friend.”.......For those who are in their 20s, 30s or early 40s, you may not know how big Simon and Garfunkel were in the 1960s and 1970s. They were inducted into the Rock & Roll Hall of Fame in 1990...and deservedly so. In the early 1980s, the performed in Central Park in front of 500,000 people! (That’s not a typo.) If ever get a chance to check out the video of that concert, it is well worth it.

The history of Rock & Roll has many great bands and recording artists. Many male performers had great and iconic voices. Many female performers had the same kind of iconic voices...and some of those iconic female voices should also be considered beautiful voices. Maybe I’m old fashion, but I don’t think of any of the iconic male voices I just referred to as “beautiful”...except for Art Garfunkel’s voice. All you have to do is listen to “Bridge over Trouble Waters” to know what I’m talking about............However, after reading the following story, you’ll realize that Mr. Garfunkel is also a beautiful person. I’m sure he has his issues...like we ALL do...but this is a GREAT, GREAT, GREAT story.

HELLO DARKNESS MY OLD FRIEND - Simon and Garfunkel (Note attachment for their live performance along with printed lyrics)

The college roommate who went blind reveals the untold story:

It is one of the best-loved songs of all time Simon & Garfunkel's hit "The Sound Of Silence" topped the US charts and went platinum in the UK.

It was named among the 20 most performed songs of the 20th century, included in Rolling Stone's 500 Greatest Songs of All Time, and provided the unforgettable soundtrack to the 1967 film classic The Graduate. But, to one man, The Sound Of Silence means much more than just a No 1 song on the radio with its poignant opening lines: "Hello Darkness my old friend, I've come to talk with you again."

Sanford "Sandy" Greenberg is Art Garfunkel's best friend, and reveals in a moving new memoir, named after that lyric, that the song was a touching tribute to their undying bond, and the singer's sacrifice that saved Sandy's life when he unexpectedly lost his sight.

"He lifted me out of the grave," says Sandy, aged 79, who recounts his plunge into sudden blindness, and how Art Garfunkel's selfless devotion gave him reason to live again.

Sandy and Arthur, as Art was then known, met during their first week as students at the prestigious Columbia University in New York.

"A young man wearing an Argyle sweater and corduroy pants and blond hair with a crew cut came over and said, 'Hi, I'm Arthur Garfunkel'," Sandy recalls.

They became roommates, bonding over a shared taste in books, poetry and music.

"Every night Arthur and I would sing. He would play his guitar and I would be the DJ. The air was always filled with music."

"Still teenagers, they made a pact to always be there for each other in times of trouble.

"If one was in extremis, the other would come to his rescue," says Sandy.

They had no idea their promise would be tested so soon. Just months later, Sandy recalls: "I was at a baseball game and suddenly my eyes became cloudy and my vision became unhinged. Shortly after that darkness descended."

Doctors diagnosed conjunctivitis, assuring it would pass. But days later Sandy went blind, and doctors realized that glaucoma had destroyed his optic nerves.

Sandy was the son of a rag-and-bone man. His family, Jewish immigrants in Buffalo, New York, had no money to help him, so he dropped out of college, gave up his dream of becoming a lawyer, and plunged into depression.

"I wouldn't see anyone, I just refused to talk to anybody," says Sandy. "And then unexpectedly Arthur flew in, saying he had to talk to me. He said, 'You're gonna come back, aren't you?' "I said,: 'No.There's no conceivable way.'

"He was pretty insistent, and finally said, 'Look, I don't think you get it. I need you back there. That’s the pact we made together: we would be there for the other in times of crises. I will help you'."

Together they returned to Columbia University, where Sandy became dependent on Garfunkel's support. Art would walk Sandy to class, bandage his wounds when he fell, and even filled out his graduate school applications.

Garfunkel called himself "Darkness" in a show of empathy. The singer explained: "I was saying, 'I want to be together where you are, in the black'."

Sandy recalls: "He would come in and say, 'Darkness is going to read to you now.'

“Then he would take me to class and back. He would take me around the city. He altered his entire life so that it would accommodate me."

Garfunkel would talk about Sandy with his high-school friend Paul Simon, from Queens, New York, as the folk rock duo struggled to launch their musical careers, performing at local parties and clubs.

Though Simon wrote the song, the lyrics to The Sound of Silence are infused with Garfunkel's compassion as Darkness, Sandy's old friend.

Guiding Sandy through New York one day, as they stood in the vast forecourt of bustling Grand Central Station, Garfunkel said that he had to leave for an assignment, abandoning his blind friend alone in the rush-hour crowd, terrified, stumbling and falling. "I cut my forehead" says Sandy.

"I cut my shins. My socks were bloodied. I had my hands out and bumped into a woman's breasts. It was a horrendous feeling of shame and humiliation.

"I started running forward, knocking over coffee cups and briefcases, and finally I got to the local train to Columbia University. It was the worst couple of hours in my life."

Back on campus, he bumped into a man, who apologized.

"I knew that it was Arthur's voice," says Sandy. "For a moment I was enraged, and then I understood what happened: that his colossally insightful, brilliant yet wildly risky strategy had worked."

Garfunkel had not abandoned Sandy at the station, but had followed him the entire way home, watching over him.

"Arthur knew it was only when I could prove to myself I could do it that I would have real independence," says Sandy. "And it worked, because after that I felt that I could do anything.

"That moment was the spark that caused me to live a completely different life, without fear, without doubt. For that I am tremendously grateful to my friend."

Sandy not only graduated, but went on to study for a master's degree at Harvard and Oxford.

While in Britain he received a phone call from his friend - and with it the chance to keep his side of their pact.

Garfunkel wanted to drop out of architecture school and record his first album with Paul Simon, but explained: "I need $400 to get started."

Sandy, by then married to his high school sweetheart, says: "We had $404 in our current account. I said, 'Arthur, you will have your cheque.' "It was an instant reaction, because he had helped me restart my life, and his request was the first time that I had been able to live up to my half of our solemn covenant."

The 1964 album, Wednesday Morning, 3 AM, was a critical and commercial flop, but one of the tracks was The Sound Of Silence, which was released as a single the following year and went to No 1 across the world.

"The Sound Of Silence meant a lot, because it started out with the words 'Hello darkness' and this was Darkness singing, the guy who read to me after I returned to Columbia blind," says Sandy.

Simon & Garfunkel went on to have four smash albums, with hits including Mrs. Robinson, The Boxer, and Bridge Over Troubled Waters.

Amazingly, Sandy went on to extraordinary success as an inventor, entrepreneur, investor, presidential adviser and philanthropist. The father of three, who launched a $3million prize to find a cure for blindness, has always refused to use a white cane or guide dog.

"I don't want to be 'the blind guy'," he says "I wanted to be Sandy Greenberg, the human being."

Six decades later the two men remain best friends, and Garfunkel credits Sandy with transforming his life.

With Sandy, "my real life emerged," says the singer. "I became a better guy in my own eyes, and began to see who I was - somebody who gives to a friend. "I blush to find myself within his dimension. My friend is the gold standard of decency."

Says Sandy: "I am the luckiest man in the world."

Matthew J. Maley Managing Director Chief Market Strategist Miller Tabak + Co., LLC Founder, The Maley Report TheMaleyReport.com 275 Grove St. Suite 2-400 Newton, MA 02466 (617) 663-5381 mmaley@millertabak.com

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at 200 Park Avenue, Suite 1700, New York, NY 10166.