THE WEEKLY TOP 10

Quick note: With the Thanksgiving holiday this upcoming week, things should be pretty quiet. By midday on Tuesday, the activity in the marketplace will slow down considerably and thus the moves in the market will not be very compelling. They’ll be skewed by a lack of liquidity rather than move on real fundamental or technical reasons. (We’re referring to a lack of liquidity due to what we will be a small of players who are active in the market place, not due to any decrease in monetary stimulus from the Fed.)......With this in mind, there will be no “Weekly Top 10” next weekend. Thank you and have a GREAT Thanksgiving holiday!!!

THE WEEKLY TOP 10

Table of Contents:

1) Last week’s “breather” was a good set up for a further rally.

2) “Performance fear” will help if the market continues to move higher.

3) “Dynamic hedging” could also play a role in a further advance.

4) That said, there are always some items on the bearish side of the ledger.

5) The economic outlook does not bode well for the stock market in 2021.

6) Neither does the earnings outlook...in this expensive market.

7) Many areas in the tech sector still look quite good.

8) The action in the bank stocks las week was quite constructive.

8a) The energy stocks could run further before long. (After a “breather”?)

9) Gold is close to testing a very important support level.

9a) Bitcoin is overbought, but that doesn’t mean it cannot rally further.

10) Somebody seems to be bearish about a Brexit deal.

11) Summary of our current stance.

Short Version:

1) The stock market played out much like we thought it would last week. It took a “breather” to work-off its overbought/over-loved condition. This should set it up nicely for a return to a rally mode...which should take stocks higher through the rest of this year and into early next year. The main catalyst for this further rally should be the Fed...who will keep the spigots open as the newest wave of the pandemic hits the U.S.

2) Therefore, we’re sticking with our 3,800 target on the S&P 500 for late Dec/early Jan. One item that should help any year-end rally is “performance fear.” When the stock market is rallying as the end of the year, most institutional investors have to keep buying aggressively...no matter what their longer-term opinion on the fundamentals might be at that time. Their year-end bonus (and sometimes their jobs) depend on them staying aggressively fully invested during year-end rally...and the whole thing feeds on itself.

3) Another factor that could help the market rally in the face of the new wave of the pandemic is the issue of “dynamic hedging.” When uncertainty is high, some institutional investors like to hedge their gains in a given year by using over-the-counter put options (or “collars”). Those options are not fully hedged by the broker who sold them...because they are usually well “out-of-the-money.” However, if the market rallies strongly at the end of the year, these firms become “forced buyers in a rising market”...which can fuel a larger than normal rally. (More details in the Long Version below.)

4) Even though we’re still bullish on the stock market for a further year-end rally, we’re always watching for reasons to think we could be wrong...especially with a market that is as expensive as this one. We’ve seen a couple of developments that DO concern us. One is the recent rise of bullish sentiment...and another one is some sizeable action in the VIX options. This is not enough to change our bullish short-term stance, but it’s something that we’ll continue to keep a close eye on.

5) Before we stray too far from the fundamentals, let’s review the economic outlook right now. Although we did see some more positive news on the housing front, there is little question that the rate of growth is slowing...and that the new wave of the pandemic will have a negative impact on the first half of next year. We actually believe that the net level of stimulus next year will shrink...and when you combine that with the slow-down...and it’s a good reason to think 2021 will not be a great year for the stock market.

6) Looking at earnings, even some of the more bullish estimates for next year will leave the stock market very expensive...and thus leave the market with little justification to rally in a significant way next year. When you combine that with what we think will be lower levels of stimulus on both the monetary and fiscal side of things, and it’s not something adds up to a great year for the broad market next year.

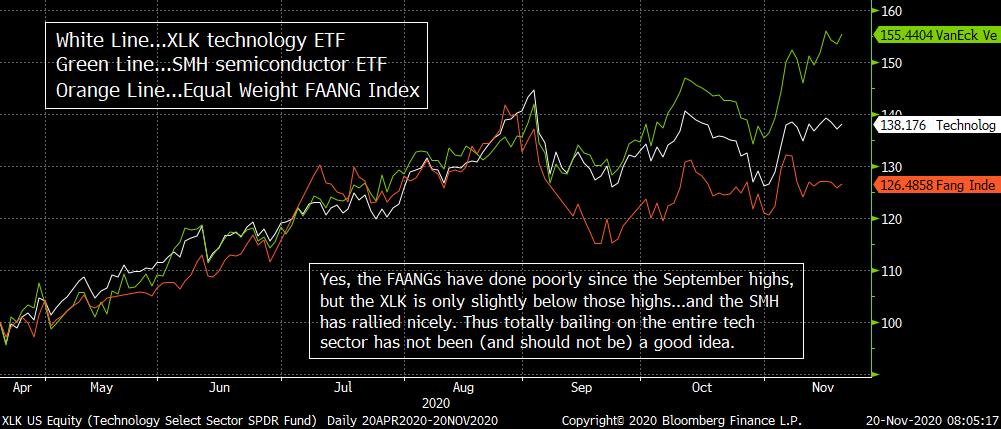

7) We continue to believe that investors should be scaling back their mega-cap tech exposure, BUT we think only a portion of it should be going to value stocks. Some of that new cash should be rotating WITHIN the tech sector. The SMH has been outperforming the S&P since September and the XLK would be doing the same if were not weighed down by AAPL. Looking at the charts of many of these “other” tech names (like QCOM, LRCX, KLAC, INTU, etc.) you can see that plenty of tech stocks are STILL doing quite well!

8) The action in the bank stocks last week was very bullish. It did take a bit of a breather at one point, but it held up VERY well in the face a lower 10yr yield and a flatter yield curve. If the KBE bank ETF can follow up its recent “double-bottom” with a nice “higher-low/higher-high” sequence, it’s going to be VERY bullish for the group on a technical basis...and lead it to attract a lot of momentum based money.

8a) The same is true for the energy stocks. They’re getting overbought on a very-short-term basis, but if the XLE & XOP can make a nice “higher-low/higher-high” sequence, it’s going to be very bullish for the energy sector as well. This will be especially true given that the sector is VERY under-owned. Institutional investors will have no choice but to flock to this group if it starts to rally more meaningfully into the end of the year.

9) While everybody was watching Bitcoin this week, gold slid lower again...and it is now close to testing the bottom line of a “descending triangle” pattern. If the yellow metal breaks below the $1,850 level in any meaningful way, it’s going to be quite bearish on a near-term basis.....We’ll also be watching the dollar. If the DXY bounces strongly off the 92 level again, it’s likely to exacerbate any decline in gold.

9a) Bitcoin saw another big rally (of 18%) last week. It has become very overbought, but it is not as overbought as it has been on a couple of other instances in the past, so it looks like it wants to rally past $20k before this leg in the rally comes to an end. We think it will then correct between 20%-30%.....BTW, we definitely do not believe it will become as euphoric as it was in 2017 before its sees its next significant correction.

10) We saw a big bet made last week in the options market last week...where an investor bet that the British Pound will fall 4% in the next month. (4% is a big move in the currency market.) Therefore, the fact that somebody is betting almost $1 million that the British currency will fall in a substantial way over the next month tells us that they are very confident in their bet. (Let’s face it, the bet will go to zero in just 4 weeks if it doesn’t work out.)....This begs the question as to whether something thinks they know that a Brexit deal is not going to get done.

11) Summary of our current stance....This past week’s “breather” in the stock market was exactly what we were looking for...and it since it helped work-off some of the very-short-term overbought condition in the stock market...it actually raised the odds that the year-end rally that we have been calling for. We’re sticking with the 3,800 target for the S&P 500...and we believe we can reach that level despite some of the growing concerns surrounding the newest wave of the coronavirus and the lockdowns that are going with them.....HOWEVER, we believe that that when the fundamentals finally do turn up from their very low levels, they’ll merely be playing catch-up with a stock market that has been pushed well beyond a fundamentally justified level by monetary & fiscal stimulus. Therefore, any improvement in these fundamentals will not be enough to help the stock market rally much further in 2021. This will be especially true because despite the fact that there will still be lots of stimulus available, it won’t be as plentiful next year (on either the monetary or fiscal side of things).

Long Version:

1)The past week played out pretty much how we thought it would...as the stock market took a “breather” by declining about 2% from its Monday highs to Friday’s close. The market had become overbought on a short-term basis by the end of the previous week, so it was no surprise that stocks pulled-back a bit to work-off this condition and digest the 11% gain the S&P 500 had experienced over the previous eleven. In other words, this was a normal and healthy reaction to the condition the market faced on Monday...and it should actually help the market rally into the end of the year and into early next year. (If it had kept rallying in a straight line, it would have stretched things too far...and kept the rally from continuing for more than a couple of weeks in our opinion.)

The biggest concern in the market place, of course, is the big increase in Covid cases in the U.S. and around the world...and the renewed lockdowns that are being announced and/or hinted-to by government officials due to this new “wave.” However, we actually think this development is likely to be bullish. Remember 7 or 8 years ago...when weak economic data meant that the Fed was going to provide more liquidity...and thus help the stock market rally further? Well, that is what is happening now with the coronavirus in our opinion. As the lockdowns rise, it will create a further slowdown in growth in the economy. That, in turn, will raise the odds of a pickup in stress in the credit markets before long...and the Fed has stated that they will do “whatever it takes” to prevent THAT from happening. Therefore, even though the goal of the Fed’s current QE program is not to push stock prices higher (like it was in the years following the financial crisis), their QE program will still help stocks rally for at least a while longer...in an indirect fashion (just like it did in Q4 of last year).

Back in late 2019, it was their “not QE...QE program” that was designed to offset the effects of the blow up in the repo market that autumn...and the stock market was an indirect beneficiary of that stimulus program. This year should be quite similar...as the massive QE program that started in March will remain in place...in order to keep the credit markets stable during this new wave of the virus and new wave of shut-downs. In other words, the stock market should again be the indirect beneficiary of the concerns the Fed has about the credit markets...as we move into the end of this year and very early next year.

2) Of course, nothing ever happens exactly as it has in the past...so it’s safe to say that the action over the last six weeks of the year will almost certainly be different than last year in some respects, but we do believe the net moves will be very similar. Therefore, we believe that a move to 3,800 on the S&P 500 is very possible (and actually quite likely) by late December/early January. In other words, even though we agree with those who say the fundamental outlook is slowing down, sometimes other factors...beyond the fundamentals...can drive markets for a period of time...and we think this is one of those periods.

There are some other factors besides Fed stimulus that could/should help the market rally further as well. The first one is “performance fear” (and we’re not talking about anything having to do with Viagra). It has to do with the investment performance of institutional investors. ALL institutional investors become short-term oriented at the end of the year. (Even the ones whose fiscal year is different than the calendar year. Most of their customers only care about the calendar year, not the investment manager’s fiscal year.)

The portfolio managers who are underperforming so far HAVE to keep buying if the market is rising at the end of the year. If they fall further behind, they’ll lose their jobs. Even the ones who are beating the market HAVE to keep buying. They want to STAY well ahead of the market...because it will mean a bigger bonus for them!......This is true even if those PM’s think that a major bear market is going to start in the 1st quarter of the following year!!! They cannot afford to miss a year-end rally no matter what is coming around the corner. They can shift their portfolios early in the next year, but raising cash at the end of a year when the market is rallying is a cardinal sin in institutional investing.

Year-end buying is never assured, so we cannot say that this kind of buying will absolutely take place. In other words, this kind of buying will only act to accelerate the rally, it won’t cause it. However, with the Fed’s liquidity spigots wide open as the newest wave of Covid-19 takes hold, we things like “performance fear” will enhance the rally even more.

3) There is another issue that has little to do with the underlying fundamentals that could fuel a further rally in the stock market over the last six weeks of the year. It’s called “dynamic hedging.” Long time readers have read our comments on this issue towards the end of some other years over the past decade.

This not something that is compelling every year, but it is when there are years when people worry about late-year declines. Most of the time, that takes place with the stock market has seen a huge rally during a year...and some investors want to hedge their gains against a late year negative surprise. This time around, however, it is possible that some investors have simply protected their gains from March...against the election results or another wave of the coronavirus.

That might sound a bit confusing, but this is what we’re trying to say. When institutional investors sometimes want to protect their gains against a late-year surprise...so they go into the market place and buy over-the-counter put options on the broad market (usually on the S&P 500). With everything that has taken place this year, it would make sense that these investors would have been worried about a negative year-end surprise this year during the late summer or early fall. So we think this kind of hedging probably took place this year.

Anyway, what they do is....they go out and buy put options to protect themselves. However, many of these institutions are too big to hedge themselves in the regular listed options market. Therefore, they go to a bulge bracket firm and ask them to sell them an over-the-counter put option...or “collars.” (Another reason they go to this OTC market is so that they can leave fewer...or at least smaller...foot prints.) They tend to buy put options that are well “out of the money”...because anything close to “in-the-money” puts would be way too expensive. These institutions are merely trying to protect against a major decline. They don’t care about a mild late-year decline...so they only buy well out-of-the-money puts that are more reasonably priced.

The bulge bracket firm goes ahead and sells these institutions the put options...and then they go out and short S&P futures as a hedge. However, since the put options are so far out-of-the-money...they do not hedge their entire position! They short a portion of the full position...say 20%. (The option is SO far out-of-the-money that there is no need to hedge more than that much of the position.) They don’t short (hedge) any more UNLESS the market falls in a meaningful degree. If that happens, they short more and more as the market falls and gets closer to the “strike price”...so that they are fully hedged if/when the market reaches that level. This causes “forced selling” into a “down market”...which is not good at all.

HOWEVER, if the market does not decline...and instead rallies...it can cause “forced buying” into a “rising market”!!! That’s right. If the market starts to rally, the bulge bracket firm is still short that original 20% hedge!!! So they have to cover that short if the market rises. If they don’t, they’ll lose more money on the short position...than they made in the commission (the premium) when they sold the put option to the institution in the first place. The traders at those firms are not there to bet against the institution. They’re merely there to collect the commission on an insurance policy (that will probably never go into effect). Therefore, if the market rallies, they will be “forced to buy into a rising market” so that they keep as much of the commission as they can. Of course, “forced buying” into a rising market is GREAT for most other investors!

We readily admit that we do not know if this kind of hedging has taken place this year to any significant degree...because we do not work at a bulge bracket firm any longer. (We also readily admit that there a many other hedging strategies that are much more complicated than the one we just described, but pretty much all of them still work on idea of “dynamic hedging”...and thus they all can have an outsized impact on the markets at the end of the year sometimes...IF the market sees an outsized move.).....Given that the VIX has been quite elevated for most of this year, there are certainly reasons that this kind of hedging was not very prevalent this year. However, when things are as uncertain as they have been this year, it’s still a good bet that at least SOME of this kind of hedging has taken place. Therefore, it could be something that helps the market rally more than the underlying fundamentals would provide for over the coming weeks.

4) As much as we believe that the stock market will rally further into the end of the year, we certainly admit that there are some reasons to be worried. First and foremost is the impact of the newest wave of the coronavirus. We’ll actually talk more about this issue...and the impact it will have on the economy in the next few bullet points, so we won’t touch on it here...except to say that we think it is more likely that this issue will have more of an impact next year. However, there is certainly a chance that the situation will deteriorate more quickly than we’re thinking...and will have a negative impact on the markets (and overwhelm the liquidity being provided by the Fed).

We’d also note that some sentiment measures are getting extended. For instance, the Investors Intelligence data shows that bullishness has reached 59.6%...with bearishness falling to just 18.2%. That 40% spread between the two is a warning flag for the markets. We usually like to see bullishness move above 60% before we send up a warning flag, but it’s certainly getting close. That said, the DSI data shows that bullishness among futures traders is still below 70%, so this is another reason to hold-off sending up a major warning signal about the issue of sentiment. However, there is no question that sentiment is starting to get extended...so it’s something we’ll have to continue to keep an eye on.

We’d also note that we saw a big pickup in the purchase of call options on the VIX. Needless to say, call options on the VIX are bearish bets on the stock market, not a bullish bet. Most of these bets were for a big rise in the VIX by January...and it was very reminiscent of what we saw last year...when a lot of VIX call buying took place during the fall months. In last year’s example, the VIX did not start rising in significant way for quite a while after these options were purchased. In some case, the positions were rolled forward until later months before the market tanked. Therefore, this might be something to worry about further into the future...than about a significant rise in the VIX over the next couple of weeks. However, when investors spend millions of dollar betting that volatility is going to jump substantially at some point over the next two months, it’s always something that makes us say hmmmmmm.

As you will read in point #9, we also saw some interesting activity in the options on the British pound last week, so this has our antenna up looking for reasons that could disrupt our bullish stance. Right now, we still think that the coronavirus will cause the Fed’s liquidity spigots to stay wide open...and that will push stocks higher over the coming weeks. However, we will be watching closely for signals will tell us that this expensive market is going to roll-over sooner than we’re expecting right now.

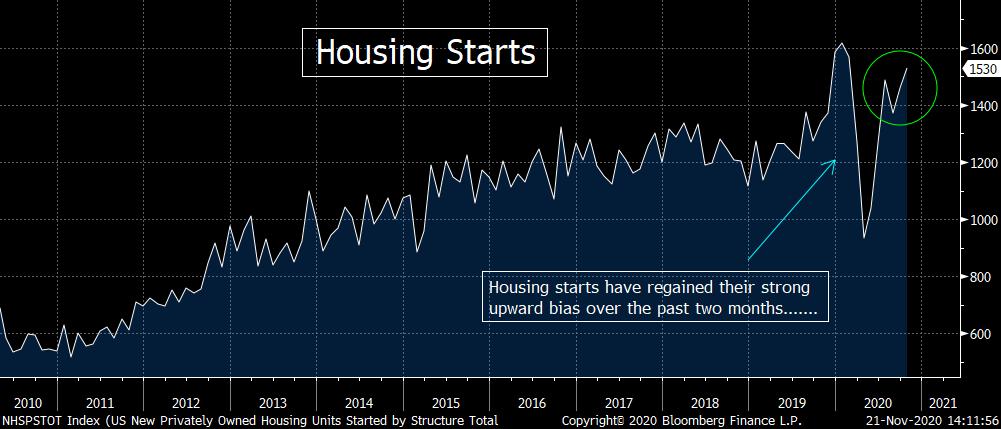

5) It’s ALWAYS important to look beyond the fundamentals...like we just did in the first three bullet points this weekend, but we don’t want to overdo it either. Fundamentals ARE critically important. With this in mind, let’s look at some of the key fundamental indicators we look at on a consistent basis. On the positive side of the ledger, we got some good data from some areas last week. First of all, the data on housing starts and existing home sales were much better than expected...as was the NAHB (National Association of Home Builders) survey. The housing sector is obviously very important to the broad economy, so this was certainly good news.

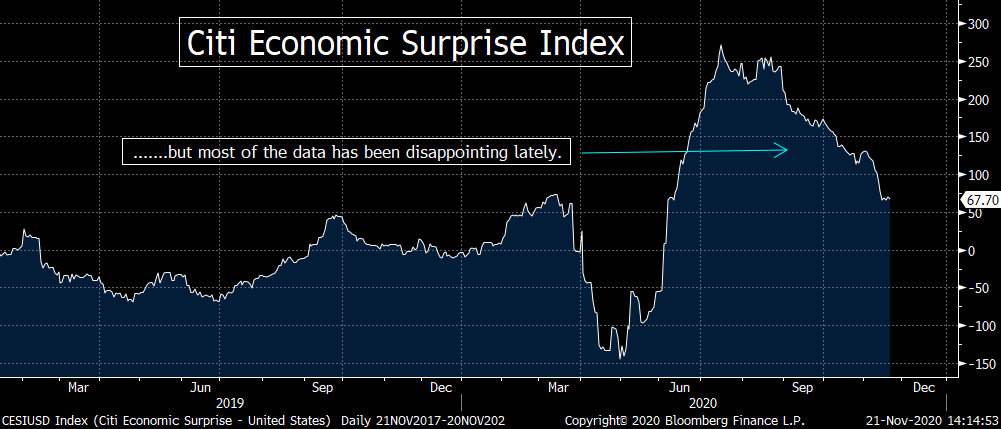

However, we also got some lower-than-expected data from retail sales, the Empire manufacturing number, and jobless claims. In fact, the Citi Economic Surprise Index has fallen 75% from its July highs, so there is no question that the big increase in growth that the majority of Wall Street was looking for in Q4 is not going to come to fruition. Of course, that’s becoming more obvious due to the big increase in Covid cases and lockdowns across the globe. (How most of the mainstream economists on Wall Street didn’t see that coming a long time ago is beyond us.) Well, this is all changing...as estimates are coming down all over the street...with firms like JP Morgan not only worried about the current quarter, but they’re saying we’ll see a decline in growth during Q1 of next year!

On top of the more traditional economic indicators, we’re seeing a slow-down in the high-frequency data. As our economicst, Paul Shea, points out, mobility is showing signs of slowing. As Paul stated in his piece this week, “To identify the impact of the fall covid-19 wave, we compared the recent changes in mobility by state to the number of new cases. For each additional 30 cases per 100,000 residents (which corresponds to 100,000 more new daily cases nationally), households have reduced their movements to retail and recreational locations, groceries, and pharmacies by about 3%. They are also reducing their movement to workplaces by about 1%.”.......So there is no question that the healthcare crisis is creating more headwinds for the economy again...much like we have been saying it would for many, many months.

The retail sales data was particularly concerning...especially since several credit card issuers (like Citi and Chase) have said they’ve seen a decrease in spending recently. (We’d also note that gasoline purchases have fallen to their lowest levels since the spring...and several airlines are reporting a pickup in reservation cancellations and a slowdown in new reservations.) Therefore, if the renewed negotiations in DC between McConnell, Schumer and Pelosi don’t bear any fruit, the holiday selling season will be a disappointing one..........Not only will all of these issue have an impact on Q4 growth and earnings, it will almost certainly have a similar impact on 2021 growth & earnings (especially in the first half).

This is one of the key reasons why we are much less bullish than the consensus on the upside potential for the broad stock market for the full year next year. The stock market can ignore these fundamental issues for a while. In fact, we think they can and will continue to do just that (due to the Fed’s liquidity). However, as the vaccines and improved treatments ease the impact of the pandemic on the economy, we believe stimulus will become much less plentiful.

Therefore, since the stock market is already pricing-in the level of growth we’re likely to see...even when you include the better potential for the second half of next year...it will make it very difficult for the stock market to rally in a significant way next year. It is just too expensive to justify a further rally of significance without an INCREASE in stimulus. Instead, although there will still be a lot of stimulus next year, it is likely to be less plentiful in 2021. THAT will not be good for the stock market.

6) Let’s look at this fundamental picture in another way...by using the most important factor in fundamental analysis...earnings. We’re sorry, but the situation for earnings is not a good one for the stock market in 2021...no matter what some pundits try to say. The consensus earnings estimate for 2021 on the S&P 500 is between $168 and $169. So right now, the stock market is trading at more than 21x those forward (2021) earnings. THAT is expensive. Needless to say, if the S&P 500 rallies to our 3,800 year-end target, that will give the market a 22.5 multiple!.....The biggest problem is that the vast majority of the time, earnings estimates FALL as we move through any given year. So we will be looking at a precarious situation in 2021 when it comes to valuations.

Of course, earnings estimates do not always fall as we move through a given year. Sometimes (very infrequently) they DO rise...and given that we should be coming out of a global pandemic next year, we could indeed see estimates move higher as we head through 2021. The problem is that we heard one estimate that says earnings could go as high as $180 (or even $185) next year. That’s great, but that would still leave us with a P/E ratio above 20x forward earnings if the market stays at/near 3600...and close to 22x forward estimates if the S&P gets to their target of 3,900. The market could rally a little more from those valuation...but a lot more??? We think not.

In other words, we don’t buy the argument that earnings can be a legitimate “driver” for a higher stock market next year. Earnings growth is going to have to be A LOT more powerful than $180-$185 to give the stock market a legitimate reason to rally in a meaningful way next year. Of course, then again, we can see further “multiple expansion”...but that term is merely something that gives perma bulls a reason to say that it’s okay that the market has become more expensive. Besides, even though interest rates are VERY low on an historical basis, they’re still higher than they have been for all but two months of this year.....It’s hard for a stock market to rally in a substantial way on “multiple expansion” when it’s already very expensive on an historical basis.

This all goes back to what we’ve been saying for a while now. The stock market has already priced-in the growth in earnings we are likely to get next year. The market has done this though the artificial stimulus provided by the Fed and the government. In other words, the fundamentals are merely playing catch-up with the huge rally that has already taken place in the stock market! The fundamentals are still behind the price of the stock market, so they won’t be able to fuel a further rally in stocks from current levels (or where they’re likely to end the year). At best, they’ll merely continue to play catch-up to a stagnant stock market in 2021.

7)We want to reiterate our view on the tech sector. We continue to believe that rotating out of some of one’s exposure to the mega-cap tech names is a good idea. We also believe that rotating towards some of the value groups/stocks is a good idea. However we ALSO believe that rotating WITHIN the tech sector is something investors should be doing as they set themselves up for 2021 as well.

There is no question that the mega-cap tech stocks have underperformed the broad market since the September highs. They fell further during the September swoon...and have not retraced as much of their losses in the gain from the late September lows. However, most of the rest of the tech area has done quite well. This is especially true for the chip stocks...as the SMH semiconductor ETF has outperformed the S&P quite nicely. (The SMH is up 9.5% from its September highs vs. a flat S&P 500...and its up 22% from its September lows vs. a 10% gain for the SPX from its own September lows.)

Therefore, the action in the semis has been better than the SPX, but it has been FAR better vs. the mega-cap FAANG stocks (much better). Looking at an equal weighted index of the FAANGs, they still stand more than 10% below its late August/early September highs (vs. a 9% move above its September highs for the SMH)! So these mega-cap tech names are still feeling the effects of their much deeper (-18%) decline during September.

We’d also note that the broad XLK tech ETF has been acting better than the FAANGs. No, it is not above its September highs...like the SMH is...but that’s because AAPL is more than 23% of the XLK. AAPL still stands almost 12% below its September highs, so that is holding back the XLK. If it was not for AAPL’s outsized weighting, the XLK would be doing much better...and this shows that many other tech names are acting quite well.....Just look at Accenture (ACN). It has rallied almost 14% over just the past three weeks...and is now close to testing its all time highs. The stock made a “double-bottom” in September & October, so if it can follow that up with a “higher-high,” it’s going to be very bullish for the ACN.

What we’re saying is that investors need to avoid throwing the baby out with the bathwater when they are thinking about “rotating” their exposure within the stock market. Tech is FAR FROM dead...and investors should definitely be using some of any proceeds they garner from the sale of a portion of their mega-cap tech positions...to move the money WITHIN the tech sector.

8) Like we just said, we DO think investors should rotate some of their holdings towards the value plays...but which ones? Well, the action in the bank stocks was FABULOUS last week! Yes, the did see a mild decline, but like it was with the broad market, this is exactly what the bank group needed to do after its HUGE

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464