THE WEEKLY TOP 10.....2021 Preview

Two quick notes: First, due to the holiday, we will not be sending out a weekend piece next weekend. Second, this weekend’s piece deals with our macro outlook at next year. Thus we talk about our view on the broad stock market and several other asset classes. In our next edition (New Year’s weekend) will deal with some other macros views...as well as some thoughts on the outlook for several groups in the stock market. (We do talk about the bank stocks this weekend, but we’ll wait until the next edition to touch-on several of the other sectors/groups.).....Thank you very much and have a great holiday!

THE WEEKLY TOP 10

Table of Contents:

1) Victory laps for 2020....Turning more neutral now....Remain quite cautious on 2021.

1a) Less stimulus next year will likely lead to a deep correction.

2) Strong YOY growth for GDP & earnings will not help this expensive stock market much.

3) Given the existing bond bubble, the Fed cannot afford another stock bubble.

4) Long-term rates on the cusp of changing their mult-year downward trend.

5) Any further yield curve steepness will be compelling (& bullish for banks).

6) Look for a “tradeable” bounce in the dollar early in the new year.

7) Commodities on the cusp of confirming a major change in trend.

8) Bitcoin: Continue to ride the wave, but it’s going to see a major correction soon.

9) A major negative surprise on the pandemic front will be very bearish.

10) Summary of our 2021 outlook

Short Version:

1) We’ve had a hot hand for several months now...making excellent calls on the stock market...several groups...and several other asset classes. We’ve been quite bullish recently, but several developments are leading us to turn more neutral right now. We still think the stock market can rally further over the coming weeks, but the gains will be harder to come by.....We also think that things will be even tougher as we move through the first half of 2021. Next year’s fiscal stimulus will not be as strong. Most of it will not be additive...as most of any “additive” fiscal stimulus will come in later years...not in 2021.

1a) As for monetary stimulus, we think it will also be a bit less plentiful next year. As the pandemic subsides, they will have to pull-in their horns in order to avoid another huge stock market bubble. The bursting of another bubble will be all but impossible to control...given the massive levels of debt around the globe. The Fed wants to avoid that, so they will slow down the flow of stimulus to some degree next year...when that happens (and fiscal stimulus is wanting), a deep correction will become quite likely.

2) We DO believe that economic growth and earnings growth will be much stronger next year than it was in 2020. However, that will not be enough to help the stock market rally a lot further next year. The simple reason is that although growth will be a lot better for both than it was in2020, the growth won’t be any better than it was prior to the pandemic. Since the stock market has already rallied in a massive way...and become very expensive...it will take the kind of growth that is much stronger than it was before the pandemicto fuel a further significant rally. Mere strong YOY growth (from a VERY weak year) will not be enough.

3) Some people think that if the Fed creates another bubble, it’s no problem...they’ll just hit the QE switch in a more powerful way and the markets and economy will bounce-back nicely. However, the huge increase in corporate debt to another new record...especially since so much of it is on the cusp of becoming rated as junk bonds...will make stock bubbles even more dangerous than they have been in the past. So we believe the Fed will want to avoid that kind of development in 2021.

---4) The text books tell us that low interest rates validate higher valuations. However, long-term rates are starting to rise. The rise is unlikely to be substantial, but it won’t take much more upside follow-through in the yield on the 10yr note to confirm an important change in trend for long-term interest rates. That could certainly have an impact on the broad stock market...and it should have a big impact on some stock groups.

5) We’d also note that they yield curve (as measured by the 2yr/10yr yield spread) has steepened to a level that is also on the cusp of confirming an important change in trend. Thus if the yield curve steepens much more at all, it will give us the confirmation we need. That, in turn, should be quite bullish for the bank stocks.....The banks are getting overbought near-term, so they may need to take a breather, but like them longer-term.

6) The dollar has been falling out of bed recently. However, it is also becoming very oversold...AND it has become VERY over-shorted by the dumb money “specs” (as can be seen by the COT data). Therefore, although we think the dollar could/should fall a bit more over the near-term, we do think it is getting ripe for a “tradeable” multi-week bounce. That could/should have an impact on several other asset classes, so investors will need to be very careful and very nimble going forward.

7) One of the asset classes that could/should be negatively impacted by a tradeable bounce in the dollar is commodities. HOWEVER, although they could see a “breather” in their recent rally, we continue to believe that an important change in the long-term trend in this asset class has taken place. If/when the CRB breaks above some (close-by) resistance levels, it will confirm the change.

8) Bitcoin.....Bitcoin could easily rally towards $30k before it tops-out. However, we believe this rally is being fueled by liquidity more than it’s fundamental story. (It’s no coincidence that when the FAANMG’s stalled out, the Bitcoin rally accelerated.) Therefore, when liquidity becomes less plentiful at some point next year (like we think it will), Bitcoin will get clobbered...even though we think it will rally even higher over the very long-term.

9) By far, the biggest risk for the markets next year is that a new variant of the virus becomes a serious problem. They seem to have discovered one in the UK and it has caused a big increase in the size and severity of new lockdowns. If this becomes more prevalent around the world...especially if it lasts for any meaningful amount of time...this over-valued stock market is going to get hit very hard...just like it did in the first quarter of 2020.

10) Summary of our outlook for 2021.......The main thrust for our call on the U.S. stock market for 2021 is that it’s going to be a tough year. Yes, we are going to see an enormous increase in both economic growth and earnings growth, but that will only be due to the fact that this past year’s growth (2020 growth) in both areas was incredibly weak. When you compare those GDP & earnings numbers to history (instead of comparing the “growth numbers” on a YOY basis), they won’t be as impressive as the seem at first glance.

If the stock market had also finished the year at a much weaker level than it finished 2020, we’d be using the 2021 growth expectations for reasons to be very bullish. However, since the stock market has, instead, rallied strongly...and now sits at new all-time record highs...and at VERY stretched valuation levels...we are taking the exact opposite tact. The only way the market can rally in a significant way next year is if the Fed and other global banks keep the pedal to the metal with their liquidity. That might indeed take place, but we believe they will pull-in their horns at least some-what once the pandemic subsides...because they will want to avoid creating another massive stock market bubble. It will be too tough for them to pull the economy out of the abyss once again if we get the bursting of another big bubble...given the massive levels of debt in the U.S. and around the world.

Long Version:

1) We’ve had a hot hand for several months now. We called for a correction in late August...and then as we moved into October, we called for a meaningful year-end rally. Both came to fruition quite nicely. We also did well with the groups...saying that the FAANGs would lead the market lower in September, BUT we did not jump back-on that band wagon in Q4. Instead, we said investors should look at two lagging groups, the banks and the energy stocks...and we also said they should look to rotate WITHIN the tech sector (especially the chip stocks). All of these calls have worked out very well.

In fact, these calls are merely several among the many great calls we’ve had this year. However, we don’t want to bore you by taking too much time taking a victory lap this weekend. However, we do want to highlight one more call...the one where we POUNDED THE TABLE back in late January and early February...telling investors to raise cash for what we (correctly) thought would be a deep decline in the stock market due to the global pandemic. Unlike the consensus, we saw that this pandemic was much different than the other once of the past few decades...and thus WOULD have a major impact on the markets.

Okay, now that we’ve dislocated our shoulders patting ourselves on the back...what are we looking for next year??? Well, although we believe the stock market can hold-up for several weeks longer (into the new year), we also believe that 2021 is going to be much tougher for the stock market than the consensus is thinking right now.

Our biggest concern involves something we’ve been talking about quite a bit over the past month or two. We believe that both monetary and fiscal stimulus is going to be less plentiful next year. No, it will not disappear. In fact, there will still be a high level of stimulus, but we do believe it will fall-off enough to have a negative impact on asset prices.

Let’s start with the issue of fiscal stimulus. It’s great that our elected officials in Washington seem to finally be close to agreeing on a relief package next week. It’s also nice to hear President-Elect Biden calls this new package just a down payment...and that there will be more relief to come. However, we question just how big any further relief packages might be in the future. It is taking a very long time to get this most recent package passed...so how much time will it take to pass another one...when the Democrats have a smaller majority in the House?

More importantly, this relief stimulus will not be very additive. It will merely be replacing existing stimulus (or stimulus that rolled-off recently). In other words, it will not help people spend a whole lot more money they has already been spending for the past 7-9 months...so we wonder how much it will help a stock market that has rallied tremendously over those 7-9 months (to new record all-time highs). Some people might try to say that since the last relief package caused a significant rally, the next one will too. The problem is that the first package was very additive...while this one is not. More importantly, the stock market was more than 60% lower back then...and quite cheap. Now it’s at a record all time high...and VERY expensive.

Therefore, we are going to need a lot more fiscal stimulus in order to push the stock market higher...because it’s going to take a lot more growth to justify a further rally of any consequence. More “relief packages” that only replace what was already being provided won’t do the trick...given how expensive the stock market has become.

Don’t get us wrong, unless some new major catastrophe hits the world, the economy WILL improve significantly in 2021 compared to 2020, BUT the economy will not improve significantly over where it was before the pandemic. Therefore, it will take a lot more stimulus...stimulus that is actually additive...to fuel the kind of growth that will give us a much stronger economy than we experienced in 2018 and 2019...and thus justify a much further rally than the market has already given us. If the economy is not going to be any better than it was in the two years before the pandemic...and earnings growth is not going to be any better than those two years...how in the world can one justify a pronounced (further) rally in the stock market from its very expensive levels????? (As we’ve highlighted many times recently, the consensus number of $169 for the S&P 500 in 2021 is basically the same as the actual earnings number were in both 2018 and 2019!)

Some people are trying to argue that we WILL get a lot more than just another relief package from the Biden Administration next year. Well, that certainly could be true. However, it’s going to be a lot harder to achieve if the GOP wins one (or both) of the Georgia senate seats, but we would argue that even if/when they DO get some more stimulus passed, it’s not going to move into the economy for more than a year......We won’t totally rehash our argument that says any new (additive) fiscal stimulus will be back-end load...since we have put forth this argument ad nauseam for several weeks. However we will quickly reiterate the main trust of that argument. Basically, we believe that the Biden Administration will back-end load their fiscal stimulus so that it will kick-in during the third and fourth year of his administration (like fiscal stimulus usually does for a new administration)...so that he (or some other Democrat) will get re-elected four years from now.

Therefore, we do think that the issue of fiscal stimulus will help the stock market to the degree that the consensus seems to think right now. It could/should in the years to come, but we do not think it will give the kind of help next year than many people think it will.

1a) On the monetary side of things, we are not as sure as most pundits are that the Fed will keep the pedal to the metal with monetary stimulus next year.......Again, we don’t want to bore you by regurgitating the full argument we’ve been putting forth for several weeks recently, but we DO want to reiterate the gist of the bottom line our thesis.

We believe that the Fed’s biggest concern is the credit market...and it continues to be quite stable. Yes, they’ll provide enough liquidity to keep it stable, but once we get past this current period of lock-downs, it will not take as much stimulus to keep those markets steady and calm.

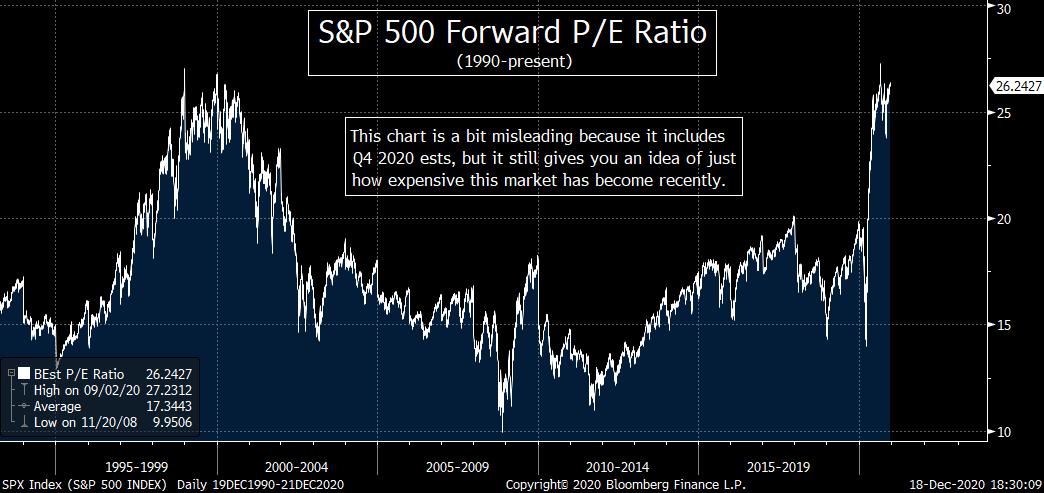

We’d also note that the Fed likely wants to avoid creating another major stock market bubble...by pushing the stock market a lot higher from current levels. The S&P is already trading at 22x forward estimates, so if the market rises to 4500 (the way one bulge bracket firm thinks it will), that will take it to over 26x the consensus estimates for 2021. In fact, even if earnings on the S&P can rise to the unlikely level of $200 next year, the index will still be trading at almost 23x earnings. Therefore, if the Fed keeps pumping like it has over the past 8-9 months, it will create the kind of bubble that...once it bursts...will make the fallout all but impossible to control. The record levels of debt in the global system today (MUCH more than existed going into the financial crisis) will make it much more difficult to recover from another bursting of a stock market bubble.

Therefore, we believe that the Fed is likely to pull-in its horns to a certain degree next year. Again, they won’t take it away completely...and they will do it in a very quite way. However, it’s going to be difficult for the stock market to rally in a significant way if/when the Fed closes the spigots somewhat as we move through the winter months and into the spring. This will be particularly difficult given that any additive fiscal stimulus will unlikely to be forthcoming next year either.

2) Let’s look at the issues of economic growth and earnings growth in another way...and in a bit more detail. We keep hearing from many, many pundits that growth next year is going to be SO good that it will fuel another strong rally in stocks. As you can tell from our comments above, we don’t think this is likely.

Let’s look at economic growth first. The consensus is looking for GDP growth to be about 4% next year...and Goldman Sachs made headlines last week by stating it could be more than 5%. Those are very strong numbers, but we have to realize that they are “growth” numbers, not absolute numbers. Those 4% and 5% numbers are YOY numbers...so the growth will be merely be 4% or 5% better than 2020...which was a very poor year for growth! Yes, Goldman claims that the economy will get back to pre-pandemic levels, BUT the economy wasn’t exactly spectacular in 2019. Despite the big rally in the stock market that year, GDP growth was just 2.3%...and only 2.1% in Q4 of that year (just before the pandemic hit the economy hard). Those aren’t bad numbers, but they’re not great numbers either...and we question whether a return to 2019 growth will be enough to take the stock market a lot higher...given that it is already 13% higher than it was at the end of that year.

As for earnings, the consensus estimate for the S&P 500 for 2021 remains at about $168-$169 range. Again, that will be a lot higher than the earnings growth for 2020 (20% higher), but it will be less than 2% better than the full-year earnings were in 2019. In fact, it will only be 1.5% better than 2018...and the S&P is now more than 40% above where it ended 2018! So the stock market is 45% above where it stood in 2018 (and 24% above its highsfor that year)...even though the odds are high that earning growth for the 4-year time span from 2018 to 2021 will likely be no better than ZERO!!! (We say “no better than zero” because earnings estimates at the beginning of a new year are almost always too high. The actual earnings numbers for any given year are almost always lower than the estimates were at the beginning of the year.)

What we’re saying is that we hear some pundits say that the stock market can rally double digits next year because earnings are going to grow by 15%-20%. To that we say, so what??? That top-end of that YOY earnings growth estimate for 2021 only takes it to the same level as it was in 2018 and 2019. So how does that equate to further double digit gain for the S&P 500...when it is already 45% higher???

So this leads us to ask once again, how in the world is the stock market going to rally in a significant way next year...when the underlying economic growth has been (and should continue to be) relatively mediocre compared to long-term historic levels...and earnings growth has been (and should continue to be) non-existent...AND yet the stock market has already rallied in a substantial way???

Of course, it is certainly possible that the stock market could continue to rally in a pronounced manner throughout most of next year. (The Fed might just keep on pumping like crazy.) However, anybody who is being honest with you will have to say that any major (further) rally from current levels would merely mean some more extensive “multiple expansion”. Given that it’s already 22.5x forward earnings (and more than 28x stated earnings), any more “multiple expansion” is going to take the stock market into bubble territory...................Some people might think that would be great....we do not.

3) Let’s cover the “interest rate” issue that we alluded to in point one more deeply.....There is no question in our minds that the Fed will keep short-term interest rates at zero for the foreseeable future. However, it’s going to be hard for long-term interest rates to drop more...since they’re already below 1%. More importantly, as we highlighted earlier, we question if the Fed really wants to fuel another stock market bubble given the situation we face in the corporate bond market.

It was easy for the Fed to come-in and save the day after the 1987 crash and the 2000 tech crash. However, it wasn’t so easy in 2008 and 2009...and now that the certain areas of the credit markets (like corporate bonds) have reached bubble proportions, it’s going to be VERY difficult to pick up the pieces...if another stock market bubble is created...and then bursts.

When we refer to the corporate bond market bubble, we’re talking about the $10.5 trillion in corporate debt that now exists in the U.S. That’s 30 times higher than in 1970s...and is now half the size of our country’s GDP! Just over $7 trillion of that debt is rated BBB to AAA and $3.6 trillion of that number is rated BBB (one notch from junk). Therefore, another big round of downgrades will likely mean more than half of the U.S. corporate bond market had junk ratings! We question if the Fed really wants cause that from taking place. Letting the stock market skyrocket and then crash will make that scenario a likely one.

In other words, it is our belief that the Fed HAD no choice but to flood the system with massive liquidity last spring in order to defrost the frozen credit markets...and the stock market rally was merely a side beneficiary of that bailout. However, now the credit markets have calmed down and thus they don’t need the same kind of liquidity to keep those markets running. (Or at least they won’t after this most recent wave of shut-downs passes.) In fact, we would argue that by continuing to provide loads of liquidity, they’ll be sewing the seeds for another major crisis within just a few years. If the stock market moves a lot higher...and is allowed to reach bubble territory...something will eventually pop it. When that happens, the entire system will collapse in a way that will rival the 2008 crisis. (In fact, some believe it will be even worse.)

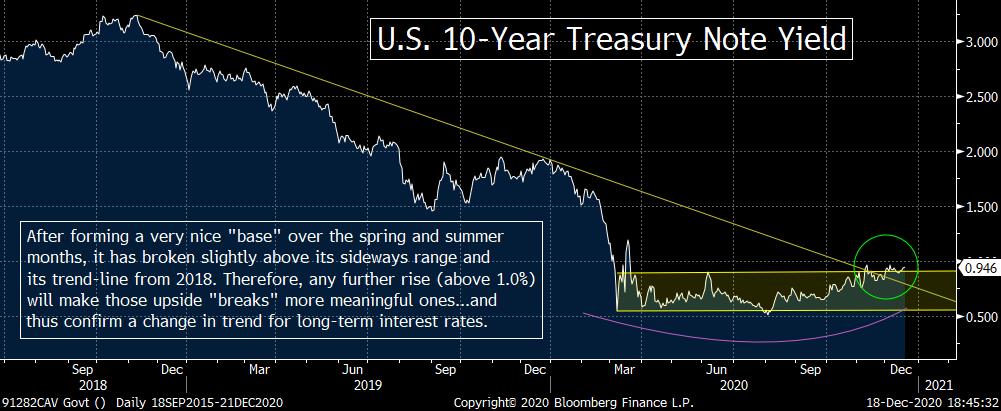

4) With the year coming to an end, this would be a good spot to highlight the longer-term chart on the yield for the U.S. 10-year note. It continues to stand at a critical juncture as we move into the new year, so we want to make sure that as many people as possible realize that long-term yields are at the cusp of signaling an important change in trend.

We keep highlighting the 1.0% level as the key resistance level. The real number is 0.96%. That was the closing high on November 10th and December 4th, so any break above that level would give it an important “higher-high.” However, since we always want to see a “meaningful” higher-high to confirm the breakout, we’ve been using the round number of 1.0%. Therefore, this 1.0% level is much more than just a round number.

However, we’d also note that a move above 1.0% would also take the U.S. 10-year yield above its trend-line going back to 2018! We’d also note that the “set-up” for a breakout is much more compelling that it has been in the past. In other words, a lot of people might ask why this move might be more compelling than many other moves in recent years? Well, one of the very important reasons we think this “set-up” is a more compelling one is that the 10yr yield formed a very strong MULTI-MONTH “base” over the spring and summer of this year. The forming of this “base” by trading in a relatively tight range for so many months also included a nice “double-bottom” in March and August (at the 0.5% level on a closing basis). Whenever any asset breaks-out of a range and then breaks above a multi-year trend line (especially if that range includes a “double-bottom”)...it’s a very bullish development on a technical basis.

As we always say, we HAVE to wait for this 1.0% level to actually be broken before we can raise a big green flag on interest rates (and a red flag for bond prices), but the potential is very much out there. If (repeat, IF) that does indeed take place, it will have important implications for the interest rate sensitive stocks like the banks. (More on the banks in the next bullet point.)

Before we move to the next point, however, we want to reiterate two things. First, we do believe that the Fed WILL keep short-term rates at zero for a very long time. We also think that although long-term rates are likely to rise, we do not think they will shoot to the moon (to 2% or higher) next year. We’re just saying that they can rise in the kind of way that should have a positive impact on the bank stocks...BUT it will likely have a negative impact on valuations. No, not a profound one...but one that (along with other items) could still help cause a correction in the stock market...one that begins in the first half of next year.

Therefore, a rise in rates will be a “good news/bad news” situation....but the “good news” has two parts and the “bad news” only has one. The bad news is that higher long-term rates could be one of several developments that could cause a correction next year. The first part of the good news is that it should be quite positive for the banks. The second part of the good news is that a correction will actually be normal and healthy...and help the stock market rally further in the years ahead. (A straight up move into bubble territory would be a disaster for the long-term health of the markets...and the economy.)

5) We had been cautious on the bank stocks for almost 3 years as we moved through the summer, BUT we became much more bullish on the group as we moved into September. Both of those calls worked very, very well...as the banks underperformed the broad market over most of the past three years...and they have outperformed quite nicely over the past four months.

This call looks even better this weekend...after we got news after the close on Friday that the Fed will allow banks to resume stock buybacks with certain limitations. This had many/most banks trading 3% or more higher in after-market trading on Friday...and several banks (like JPMorgan) have already announced share repurchase programs (that will begin in Q1 next year).

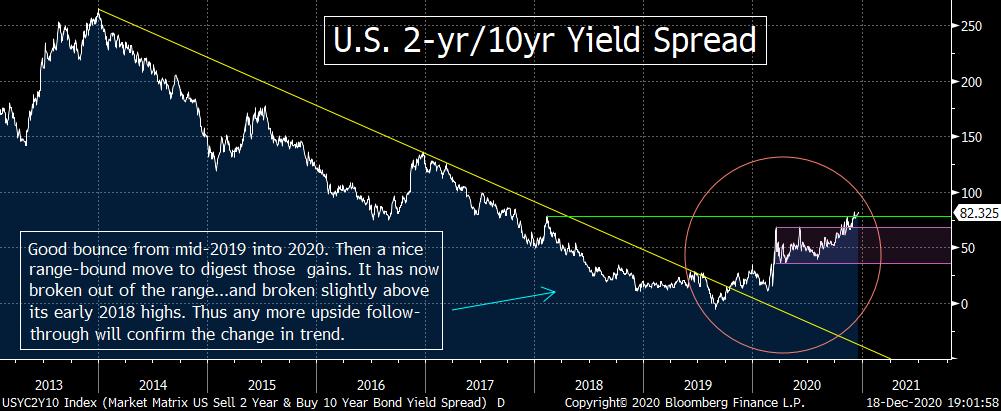

The main reason we turned much more bullish on the bank sector was due to the rise in long-term interest rates and the steepening of the yield curve. Of course, interest rates had popped several times for a little while over the past three years...and the yield curve steepened for a short period of time as well...and yet we maintained our cautious stance through all of those moves. The time that changed our stance on the group was the action in the Treasury market was different leading up to their moves in September.

We have already described the what has already taken place on the 10yr yield...and the breakout that will take place if that yield moves much higher from current levels.......However there is another reason to think this group can rally further...the steepening of the U.S. yield curve. The yield curve actually bottomed and started steepening in mid-2019. What we liked about the action in this area of the Treasury market was the fact that it was able to stabilize at a higher level...after the wild volatility we saw in March. In other words, instead of rolling back over (and flattening again), the 2yr/10yr spread traded in a sideways range over the rest of the spring and summer this year. THEN, it broke-out to the upside (to the steeper side) as we moved into September and October. Again, the “set up” we saw over the summer gave us much more confidence that the steepening of the yield curve could continue for quite some time.

Needless to say, higher long-term rates and (especially) a steeper yield curve are bullish for the bank stocks...and therefore, these developments in the Treasury market led us to change our tune and turn much more bullish on the bank stocks. This has worked-out very well...as the KBE and KRE (regional bank) ETFs have wildly outperformed the S&P 500 since the official end of summer. Since then, the S&P has rallied 14%...while the KBE has rallied more than 45% and the KRE has gained more than 50%!!!

So what next? Well, the news on the buybacks is very positive and should lead to more upside movement over the short-term. Also, we think the yield curve will continue to steepen. In fact, if you read between the lines, we would say that Chairman Powell told us one of the goals for the Fed is to continue to help the yield curve steepen going forward.

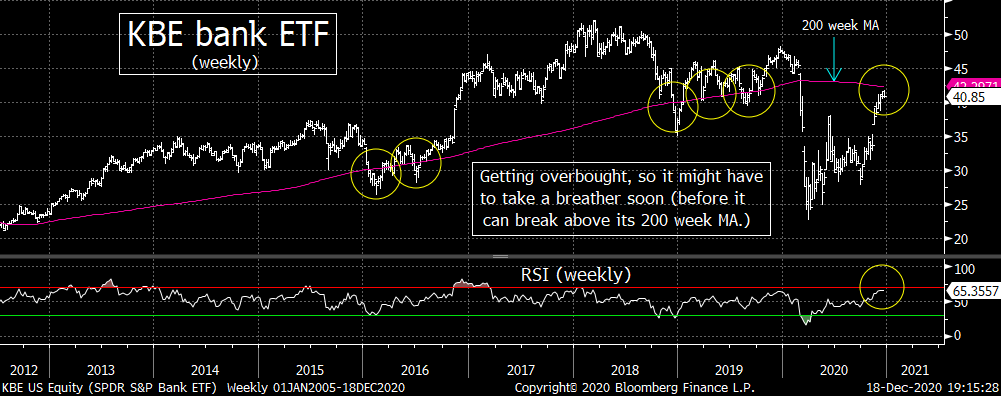

HOWEVER, we do need to point out that the group is getting overbought. First of all, the weekly RSI charts on both the KBE and KRE are becoming overbought. No, they’re have not reached extreme levels (like they did in late 2016 and early 2017), so they can (and should) certainly still rally a bit further going into the end of the year. However, we’d also note that these overbought conditions are being reached just as both ETFs approaching their 200 weekmoving averages. The 200 week MA’s have been very important lines for the bank stocks...for many years.

From 2011 until 2019, the 200 week MA provided excellent support for both bank ETFs on several occasions. (Yes, it broke below that moving average SLIGHTLY a few times, but it quickly regained that line each time.)....As we’ve said a zillion times over the years, “old support” becomes “new resistance,” so the 200 week MA should provide some tough resistance over the coming weeks. Both the KBE & KRE might break slightly above those lines for a short while, but give that they’ve both become quite overbought, we think they’ll probably have to pull-back for a little while...to work-off those overbought conditions...before they take a more powerful run at breaking above the 200 week MA in a significant way.

As we said above, we DO think these ETFs will rally further over time, so we DO think they’ll break above their key moving averages at some point. When they do, it’s going to be quite bullish for the group once again. Not only will that kind of move take the KBE & KRE above their key moving averages, but it will ASLO take them above their three-year trend-lines going all the way back to the beginning of 2018!!!

In other words, we think a pull-back or even a correction will likely begin at some point in Q1 (after a further news-related rally). However, any correction could/should provide a good buying opportunity for the bank stocks. So what we’re saying is that we’re getting close to a point where we don’t want to chase the bank stocks further over the near-term. Instead, traders should take some chips off the table...and both traders and investors should look for lower levels to buy these names. However, any substantial break above the 200 week MA in these ETFs will be very bullish on a longer-term technical basis...no matter when it happens. We just think it’s probably not going to happen immediately.

6) One of the most crowded trades in the market place right now is the “short dollar” trade. According to BAC’s most recent Fund Manager Survey shows that this “short dollar” trade is the second most crowded trade on the Street right now (behind “long tech”). Although

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464