Morning Comment: WAKE UP, the FED has become more hawkish!

Despite the consensus narrative after the Fed announcement/press conference yesterday, we would argue that the one thing that everybody is missing is that the Fed keeps confirming lately that it has changed its policy...and has become more hawkish. It’s only a subtle change, but it is a change none-the-less. This change in policy will create headwinds for the stock market...and will likely create a correction in the stock market over the coming weeks and months.......This does not mean that long-term bond yields will continue to move higher immediately. In fact, as we will cover later in this piece, bond prices have become extremely oversold and thus likely to see a short-term bounce...which means long-term yields have become overbought and are likely to decline at some point soon. (The problem is that the catalyst for the decline just might be a sharp fall in the stock market.)

We realize that we’re standing on an island by ourselves by saying that yesterday’s comments from the Fed did not indicate a more dovish stance...and that they indicated that their stance has shifted to a more hawkish one, but we still think we are correct. Of course, we could be wrong. We’ve been wrong before and we’ll be wrong again...but we don’t think we’re wrong this time...and we hope you will read-on to hear the other side of the consensus argument. (Then we’ll move-on to explain why we believe long-term rates could/should see a short-term pull-back...even thought they’ll head higher again before too long.)

Think about it for a minute. In early January, we had a situation where the Fed was saying that they were not even thinking about...thinking about...raising short-term rates. Also, there was absolutely not hint that they might taper back on their present (massive) QE program. On top of this, the yield on the 10yr note was still below 1%...so nobody was even asking the Fed about whether they were concerned about its rise off of the summer lows of 0.5%. Finally, the Fed was hinting that they would let inflation run hot (even though inflation were still quite subdued).

Well, some of those conditions are still the same. The Fed is still saying it’s way too early to raise short-term rates. They’re also still saying that they’ll let inflation run hotter than their 2% target. These are things Fed Chairman Powell has said many times in this new year...and he reiterated them once again yesterday.

However, SOME things HAVE changed. First, members of the Federal Reserve have started talking about the need to taper back on their QE. They’re saying it won’t take place until 2022, but they ARE talking about it. (In other words, they’re laying the ground work.) THAT’S a change. More importantly, the Fed Chairman continues to tell us that they are will to let inflation run hot...and now that inflations concerns have increased substantially, this is also an important change in policy.....Put another way, by saying that they’re willing to let inflation run hot at a time inflation concerns are rising is another way for the Fed to say that they are willing to let long-term interest rates rise further. THAT is an important change as well.

What we’re saying is that if you just look at the facts, there should be no question in anybody’s mind that the Fed is now more hawkish than they were at the beginning of the year. Yes, one can argue that the change in stance is so subtle...and will take place so gradually...that it will not have a negative impact on the stock market. However, they CANNOT say that the Fed is more dovish...or even AS dovish...as they were when the year started. (If they do, they’re dead wrong...which is what the Treasury market is telling them this morning...with a new high for this move in the 10-year yield.)

As you can probably surmise from what we have stated in our comments recently, we would not agree with those who would say that this subtle change in policy will not create at least SOME headwinds for stocks. Don’t get us wrong, we admit that it’s possible that the Fed’s unmistakable change in stance will not have a material impact on stocks. However, we just think that the history of the past 40 years tells us that whenever long-term rates rise in a significant way over an extended period of time, it has always had a negative impact on the stock market eventually...and thus we think it will have the same effect this time around as well.

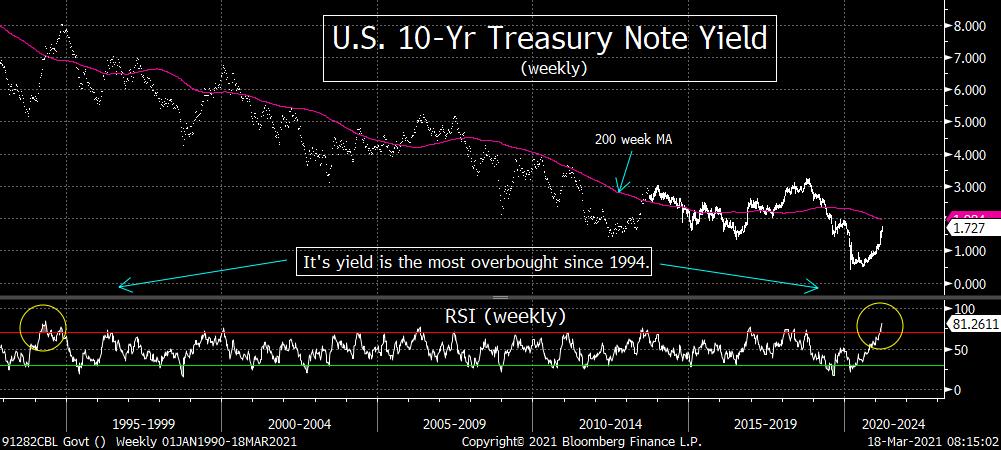

HAVING SAID ALL THIS, the technical condition of the 10yr Treasury note is becoming extreme. If you look at the TLT Treasury ETF (which measures price, not yield), it’s weekly RSI chart has reached its most oversold reading EVER. It’s reading is now below 23...which is the lowest reading since its inception in 2003. (First chart below.).......On the flip side, the weekly RSI chart on the yield of the 10yr note shows that it has the most overbought reading since 1994.

THEREFORE, the long-term Treasury market is getting ripe for a short-termreversal (a short-term bounce in price and a short-term pull-back in yields). This might give investors the belief that they should remain bullish...because as rates pull-back (even if it’s on a short-term basis), it will give the stock market (especially the Nasdaq) some relief. HOWEVER, if the catalyst for any upcoming reversal in the bond market ends up being a sharp decline in the stock market (in a flight to safety trade)...we could easily have a situation where the bond yields are falling at the same time that stock prices are falling............Caveat Emptor!

If you want to continue to get these unique insights on a regular basis during these fascinating times in the investment world, please click here to subscribe to “The Maley Report.”......Thank you!

Matthew J. Maley

Managing Director

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464