Morning Comment: Can the bounce in the bank stocks hold?

It was great to see the stock market bounce strongly yesterday…and we liked the fact that the breadth during the pop was quite good. (It was 5 to 1 positive for the S&P 500…8 to 1 for the NDX Nasdaq 100…and 7 to 1 for the Russell 2000). If there was one disappointing aspect of the “internals” of the market, it was the volume. The composite volume was almost 20% lower than it was when the market was falling in a significant way on Monday and Tuesday. We’d also note that the volume for the SPY (S&P 500 ETF) was almost 30% lower than it was on Tuesday…and it was more than 45% lower for the QQQ (the Nasdaq ETF). Usually, when the market sees a big washout bottom, the volume is strong on BOTH the down days AND the up days…so the fact that yesterday’s big bounce came on much lower volume is a bit of a disappointment.

Of course, one of the big catalysts for the bounce in the stock market was the powerful decline in crude oil. This drop in oil was spurred on by comments that Ukrainian President Zelenskiy is willing to compromise on certain issues with Russia. There was also news that UAE indicted that they’d encourage other members of OPEC to increase production going forward. However, as much as most pundits rarely give technical conditions they deserve for a big move in any asset (especially when that move is a bullish one), experience tells us that the fact that crude oil was EXTREMELY overbought on a short-term basis did indeed play an important role in the size of yesterday’s move.

The reason we (strongly) believe that it is important to understand what drove yesterday’s 12% drop…is that it means that oil traders do not necessarily think that the situation in Ukraine has gotten a lot better (or will get a lot better any time soon). In other words, whenever a certain market sees an outsized move, we always ask ourselves, “What does that market know that the rest of us don’t know?” If the oil market had not been extremely overbought…and yet it still fell more than 10%...we’d be asking ourselves is there is something better is going on in the geopolitical negotiations…than just the mild announcements we got yesterday. However, since the oil market WAS extremely overbought, we’re do not think that we’re on the cusp of a resolution to the crisis in eastern Europe.

We continue to have a hot hand when it comes to the markets. Yes, we were a little early in calling for a pullback in crude oil, but we were spot-on this week…when we started pounding the table with this call. The question now is whether oil will bounce back to its recent highs immediately…or if it will settle in at its current (still very elevated) level. If it does, there’s a good chance that the energy stocks will have to fall a bit further. They got hit fairly hard yesterday, but the 3% drop in the XLE energy ETF and the less than 1% drop in the XOP oil & gas ETF paled in comparison the huge drop in WTI crude oil. If these stocks had lagged behind crude during the recent rally, their outperformance yesterday would not have been surprising. However, since they did indeed rally in a parabolic fashion along with crude this year, they’ll have to pullback further if (repeat, IF) oil does not snap back towards its $130 highs quite quickly. In other words, we’re still not chasing the energy stocks quite yet. They’re still overbought and we think there will be a better chance to get aggressive on the group in the days and weeks ahead.

Needless to say, the inflation data (the CPI report) will get a lot of attention this morning. Given that the yield on the 10yr note has spiked back close to 2% over the past week, it sure looks like the Treasury market is pricing-in a high number…..Actually, this move in the Treasury market makes perfect sense. Even if the number turns out to be a benign one, most people will say the number is from February…and the developments in eastern Europe since then will make March’s number much higher. Therefore, we won’t be surprised if the markets don’t react very to a soft number in a material way…..Of course, if it’s a worse number, it won’t be good at all. (We hate to say it, but it seems like we are looking at a lose-lose situation with the CPI # this morning.)

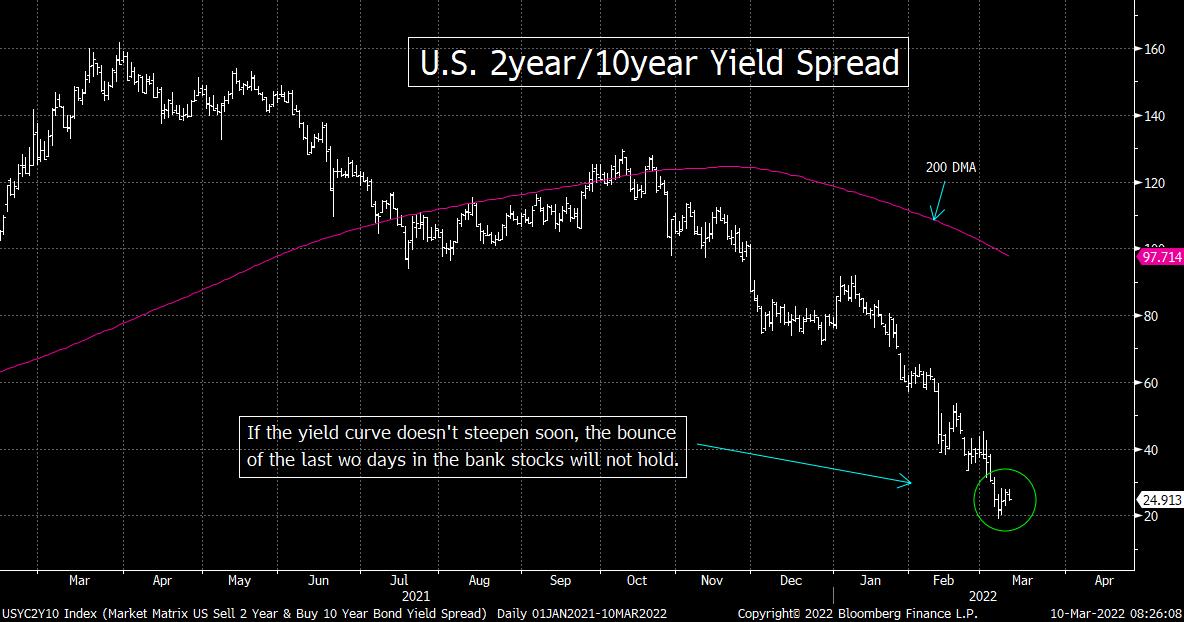

One final comment on the issue of interest rates. Keep a close eye on the yield curve. Even though the 10yr yield has bounced in a meaningful way this week, the yield curve has barely steepened at all. The 2yr/10yr spread still stands at 25 basis points, so it has barely bounced. The reason we highlight this is because the yield curve is more important to the action in the bank stocks than the 10yr yield. Therefore, if the yield curve des not steepen soon…and especially if it flattens further going forward…the bounce in the bank stocks is going to be a very short-lived one.

Of course, the headlines out of Ukraine will quickly take over as the dominate issue once we get past the CPI number at 8:30…so it’s hard to know how things will playout today. However, the futures are trading lower on the news that no progress was made at today’s negotiations between Russia and Ukraine. It’s great that President Zelenskiy is willing to negotiate, but he also said that they will not give up on Ukraine’s independence. Putin wants control of the country…and he’s not going to give up until he gets it…or he is removed. Neither one of those outcomes looks like it’s going to happen soon. Therefore, investors should expect to see plenty of continued volatility in the markets in the weeks ahead…and they should act accordingly.

Matthew J. Maley

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464