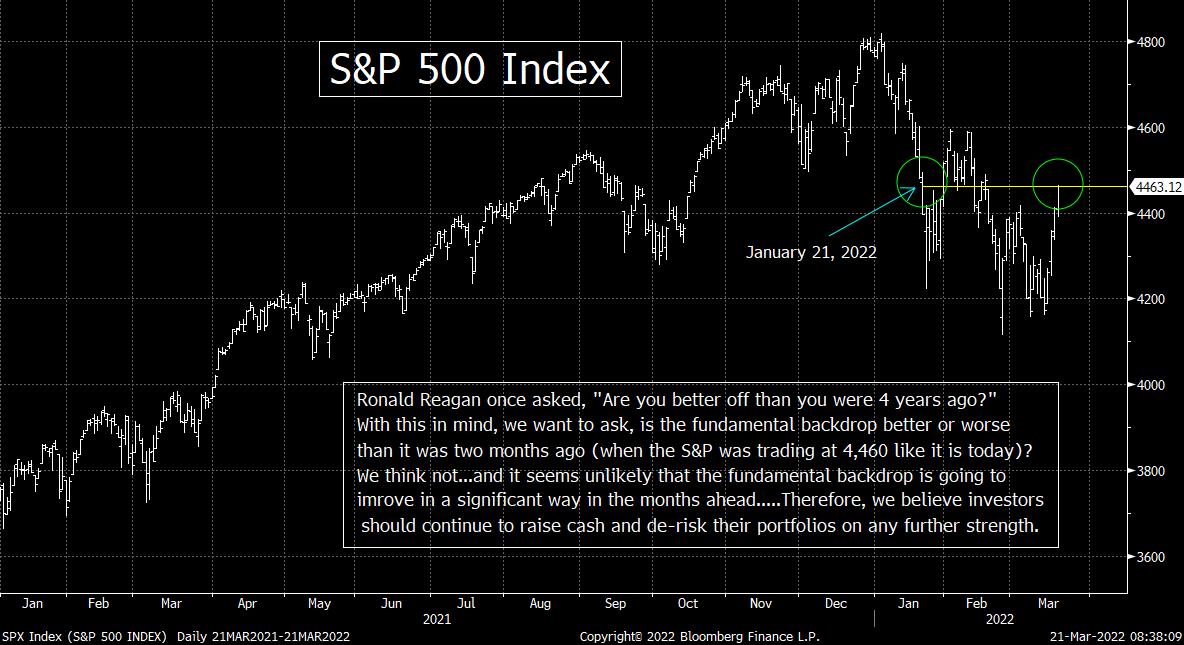

Morning Comment: Things have gotten worse on almost all fronts since January 21st

It was funny, the composite volume at 3:59pm on Friday afternoon was 4.9bn shares…but it finished the day with 7.9bn shares. So there is no question that the expiration definitely had an outsized impact on those numbers by the end of the day. Therefore, there are very few conclusions that we can draw from the “internals” from the market on Friday…which is always the case on a “quadruple witch” expiration. It’s also very hard to know how much of an impact the expiration had on Friday’s rally…or on the rally from earlier days last week.

However, after a 7% and 10% rally off the Monday lows for the S&P 500 and NDX 100 respectively, it’s a good bet that a lot of shorts were covered, and a lot of hedges in the options market were closed. This will should diminish the impact of “positive gamma” in the coming days…so at least some of the buying power that existed last week has likely been exhausted.

This does not mean that the stock market cannot rally further over the near-term. The last time we had a strong bounce in the stock market (back in late January…when the S&P 500 popped more than 6%), the rally did not end until it retraced a little more than 50% of the decline from the all-time highs. If that were to happen this time around, the S&P would move up to the 4485ish level…so it could still have more upside left in it. In fact, there’s no rule that says this bounce would have to end there. The end of the quarter is a week from Thursday, so “window dressing”…as well as some momentum factors could take the market even higher over the very-short-term.

The action over the next few trading days should give us some strong clues as to how the market will act over the next 2-3 weeks. After the big 4-day rally last week, it would not be a big surprise if the market took a breather today. However, the real question is what happens over the next couple of days. If any “breather” is short-lived…and does not involve much downside movement…it will raise the odds that we’ll see a further advance going into the end of the quarter. If, however, the market sees a significant decline over the next few trading days…especially if it comes on strong volume and breadth that is quite negative…it will raise a significant warning flag.

On an intermediate-term basis, however, we believe that the stock market is far from being out of the woods. Right now, the S&P 500 index stands at the same level it did exactly two months ago…on January 21st. Since then, GDP growth estimates have been cut in a material way (which means earnings estimate cuts are just around the corner)…and supply chain issues have become an even bigger problem. Also, the 10yr yield has jumped by 17%...and 2-yr yield has risen to its highest level since May of 2019 (which means the yield curve has flattened significantly…to under 20 basis points). On top of this oil prices have catapulted 25% higher…and inflation expectations (as measure by the TIPS market) have risen in a meaningful way. Finally, even though the Fed did not raise rates by 50 basis points (like the biggest hawks on the Committee wanted to), they are still looking for a six more rates hikes this year…and are going to start shrinking their balance sheet even sooner than they were saying they would back in January.

In other words, the underlying condition of the global economy and the global marketplace is much less supportive of this (still) very expensive stock market…than it was when the S&P was sitting at this same 4460 level back on January 21st. Sure, maybe the crisis in eastern Europe will calm down in the coming weeks. However, there is very little chance that Mr. Putin is going agree to create a situation that is similar to the one that we lived in before Russia invaded Ukraine. (Besides, even if they did, it would merely give the green light for the Fed to go forward with their aggressive tightening policy over the rest of the year.)

With all of this in mind, we believe that if (repeat, IF) the stock market can continue to rally as we move through the end of March and into the beginning of the 2nd quarter, investors should use it as an opportunity to raise some more cash and continue to de-risk their portfolios further.

Matthew J. Maley

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464