I Like Energy and Emerging Markets for Q2

How about that for a headline? Did I get my point across?

I don’t know many participants who are positioned for Energy and Emerging Markets to rip in the second quarter as the US Dollar continues to weaken. And that’s a good thing. I don’t like crowded trades, and if anything, this trade is crowded on the opposite side of that, which I love. In addition to the sentiment data suggesting this, I’m seeing the fundamental sell side analysts lowering estimates on energy stocks talking about oil this and oil that. What I’m not seeing is discussion about energy stocks rallying on higher oil prices this quarter. Again, I love that.

Last month I was fortunate to have Crude Oil play out as I was hoping (see here). I had been staying away from oil for a long time and constantly answering the question of “Where is Oil going?” with, “I don’t know”. But I had a road map where if prices made new lows in March and momentum diverged positively, we could see a squeeze if prices were able to get back above the January lows. So far this is playing out in my favor. Let’s see if this continues to follow through to the upside.

To me, I think the more important development after last month’s market behavior is not even in Crude Oil. To me, it’s the highly correlated stocks, sectors and countries NOT making new lows in March as Crude Oil hit levels not seen since early in 2009. This bullish divergence between the equities themselves and the oil futures really got my attention. With sentiment hitting historic bearish extremes in both energy stocks and emerging markets, this unwind could potentially be epic.

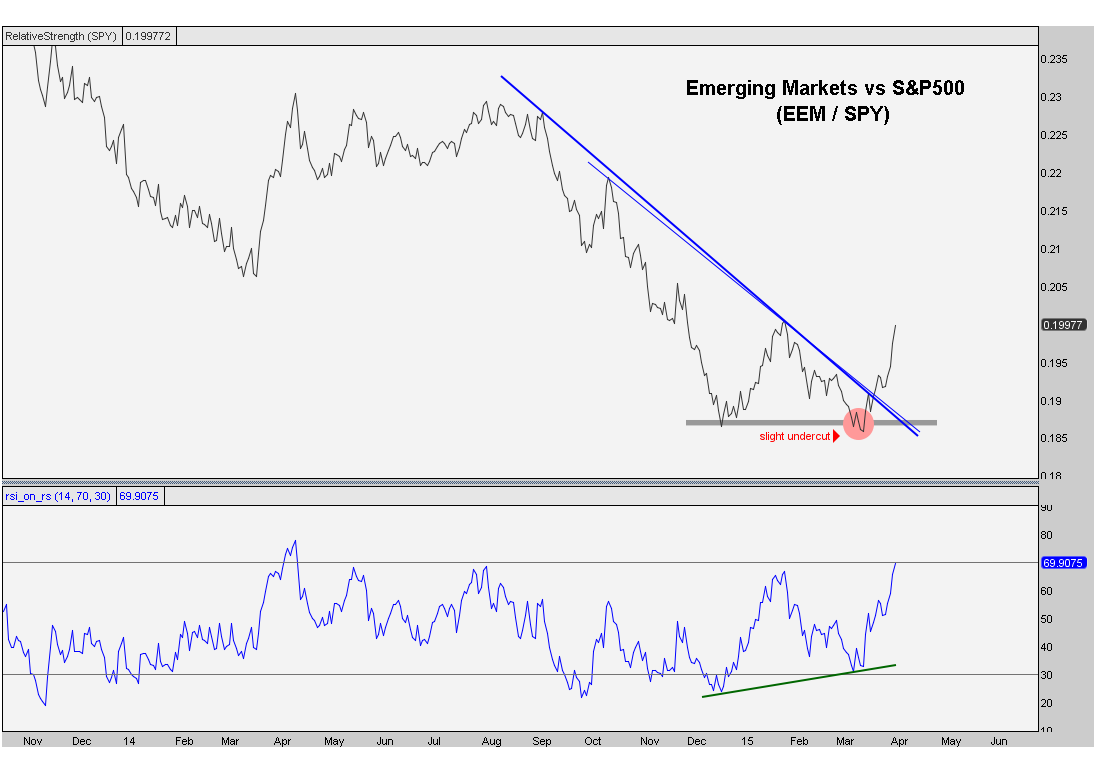

First, here is the Emerging Markets ETF $EEM vs the S&P500. Look at the brief new low in this ratio last month as momentum put in a bullish divergence. This is one of my favorite combinations. But now we are also breaking out above a downtrend line from the September highs in this ratio. I think this continues into Q2:

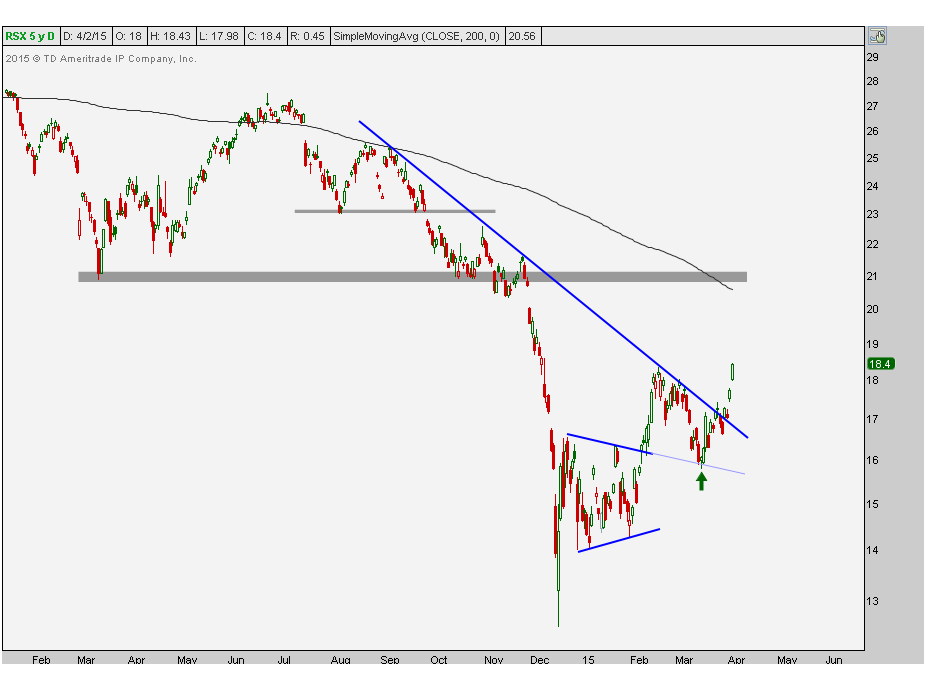

This Emerging Markets ETF represents a specific basket with difference weightings. I would just like to add that not all emerging markets are created equal, and although they all should benefit from a weaker Dollar, there are a few that to me stand out as better risk/reward opportunities. Lately I’ve been pounding the table about getting long Russia, and so far this is working out well (See here). I think we have a date with the 200 day moving average near $20.50 and ultimately see $23 which was former support in 2011 and 2012. Look at all the higher lows in Russia since December as Oil put in lower lows:

It’s hard to be bearish on Emerging Markets when you have China exploding to highs not seen since 2011. We are quickly approaching our short-term target above 46 based on the 161.8% Fibonacci extension from the September/October correction, but ultimately I think we have much more room to the upside based on the breakout of such a large multi-year base:

Now look at the potential in Thailand and Taiwan. We want to be buying a breakouts above the downtrend line in Thailand. We also want to be buying a break above the 2011 highs in Taiwan. These don’t get much cleaner and the risk is very well-defined as we only want to own them above their overhead supply just mentioned:

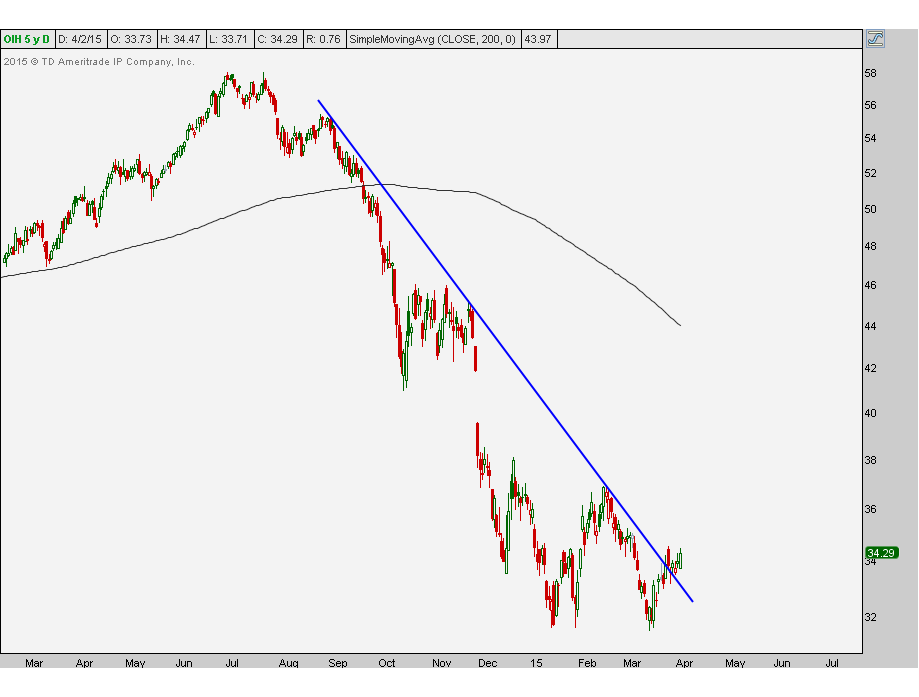

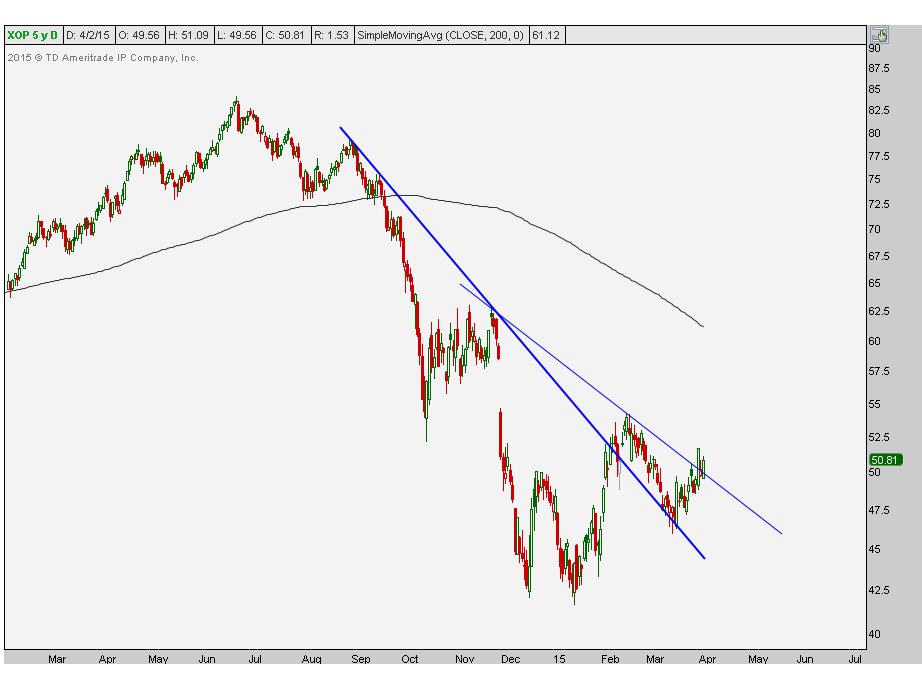

Looking here in the United States, I like the energy sectors. None of them made new lows last month as Crude Oil did. I think all 3 mean revert back towards the downward sloping 200 day moving averages where I would be selling into that strength. Of the 3 here below, I think the E&P names look the strongest. Notice how last month prices got no where near new lows. Reminds me of Russia.

S&P Energy:

Oil Services:

E&P:

If you need a catalyst for all this, I think it’s further US Dollar weakness. Here is the post I wrote the day before the US Dollar hit its peak last month March 12, 2015. I’ve never seen so much unanimous love for the US Dollar in my entire career. That was crazy. Meanwhile, I was also pointing to the key Fibonacci extensions that were being hit on March 11th. This was the 261.8% Fibonacci extension of the January – February consolidation, and more importantly this level coincided with the 161.8$ Fibonacci extension of the entire 2009-2011 sell-off in the Dollar. It’s really when these Fibonacci targets cluster together that they get my attention. Here is the weekly chart:

I don’t think there are many out there positioned for this sort of behavior in the next few months. I really like this theme. I’ll do my best to follow up if anything dramatically changes in the coming weeks. Members of Eagle Bay Solutions already receive all of this in their inbox. Make sure you’ve signed up for the package that is best for you.

***

Recent free content from J.C. Parets

-

Miami This Week For The Finance Festival

— 11/04/15

Miami This Week For The Finance Festival

— 11/04/15

-

The Nasdaq Flirts With All-Time Highs

— 11/02/15

-

Video: Technical Analysis Webinar by JC Parets

— 9/29/15

Video: Technical Analysis Webinar by JC Parets

— 9/29/15

-

Overhead Supply in Healthcare & Biotech

— 9/22/15

-

Thinking Out Loud Heading Into Q4

— 9/22/15

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464