Buying Time - March 24, 2015

Click Here for this Week's Full Letter - March 24, 2015

Greetings,

Time is the most valuable commodity in the world, especially if you’re a central banker. Last week Janet Yellen bought the Federal Reserve some time by opening up the possibility of a rate hike as soon as June, while simultaneously lowering expectations for further increases down the road. The median path of the projected fed funds rate stands at 0.625% at the end of 2015, 1.875% at the end of 2016 and 3.125% by December 31, 2017. This unlikely scenario would be the most gradual tightening cycle in US history. The Fed also anticipates the unemployment rate leveling off while economic growth accelerates – again, this scenario has never occurred in US history. However, it’s what the market wanted to hear in order to grant the Fed more time.

It’s the same story in Europe. This is an actual headline from Friday: “Greece – a deal was reached to comply with the old deal, which itself was not an actual deal.” That’s a good example of what makes investing in these markets so treacherous. ECB President Mario Draghi famously said he would “do whatever it takes” to save the Euro in 2011. It turns out he didn’t have to do anything until 2015, when QECB was initiated, but those words bought valuable time.

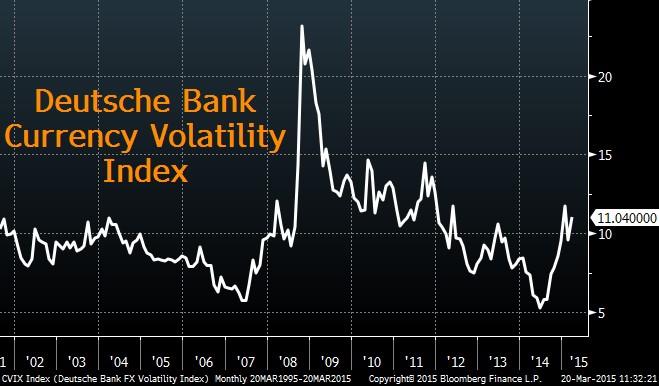

It’s still unclear when time will expire and central bankers are forced to confront massive imbalances in the global economy. At the moment it looks like the clock is ticking on the FX market. The Deutsche Bank Currency Volatility Index reached the highest levels since 2011 last week.

As I’ve said before, the biggest impact from the Fed’s QE program(s) was the smothering of volatility across the board. When asset prices are stable, it gives investors the confidence allocate capital into risky markets. The problem is that when volatility appears it’s rarely confined to one asset class. I can easily envision a scenario where currency volatility spreads into credit markets – particularly those in emerging markets – before finally reaching the stock market. When that happens it will be time for central bankers to face the music.

The Cup & Handle Fund was up roughly 3% last week, back to flat on the year, and +14% since August. My last two investment recommendations, from February and March, have performed exceedingly well. The energy stock (yes, energy) from February is up nearly 30% since the letter went out on February 16. I’m almost disappointed because I wasn’t able to build more of a position. The March letter was sent out eight days ago and the ETF selected has rallied more than 11% already. I haven’t settled on a recommendation for April yet, but the bar is set pretty high. If you’d like to start receiving these letters click here.

Today’s letter will cover several topics, including:

- Euro: On Sale

- Higher Wages or Bust

- Big Data

- Chart of the Week

With that, I give you this week's letter:

March 24, 2015

As always, if you have any questions or comments or just want to vent, please send me an email at mike@cup-handle.com.

Until next time, tread lightly out there,

Michael Lingenheld

Managing Editor – Cup & Handle Macro

Recent free content from Michael Lingenheld

-

The Finale - April 21, 2016

— 4/20/16

The Finale - April 21, 2016

— 4/20/16

-

The Spring Freeze - April 6, 2016

— 4/05/16

-

Dependent on Friday's Data - March 30, 2016

— 3/29/16

-

Money For Less Than Nothing - March 23, 2016

— 3/22/16

-

Avoid the Crowds - March 16, 2016

— 3/15/16

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464