Internalization And Why It Matters To Everyone

Internalization was a word used by the SEC in an effort to explain the Flash Crash of May 6, 2010 (page 58 of the document, page 61 of the .pdf) fallout of liquidity and subsequent computer driven mayhem which reared its head again during the Flash Crash of 2013 in April. The SEC defines internalization in summary as the brokers ability to match its clients orders against their own inventory, never routing your order to the market, which is where you see the price you wish to execute at. Ever place an order for a round number say $17.00 and get filled at $16.9999 or $17.0001? Internalized. Here’s a schematic of a simple internalizer:

Now within this complex mess of fiber-optics lies The Fix, which is a complex mess designed to enable special-order types to pick off Mom and Pop or Retail participants, something the brokers are paid to allow in exchange for the volume. I addressed The FIX on Zerohedge and highlighted the complexity added at that specific level of the internalizer. I said there:

“Not surprisingly, NYSE leads the global exchange group in Largest Value of Trades at $13 trillion while Indian NSE (the same one with the freak trade that set off price gyrations) takes the cake for Volume with 1.4 trillion trades… no surprise given the push by HFT into unregulated, emerging markets. “

There is absolutely no way for anyone outside of the literal structuring of the market to understand how their order is handled/filled/executed and it’s unacceptable. Mutual Fund houses and others who manage your or your parents 401(k)’s certainly are not fulfilling their fiduciary responsibly to ensure the best execution on behalf of their clients. I’m sure the CFA has some ethics rules about this too that are being broken.

The SEC, in all their wisdom, issued this warning in their Investor Tips: Trade Execution document:

“…your broker may direct the order to that exchange, to another exchange (such as a regional exchange), or to a firm called a “third market maker.”

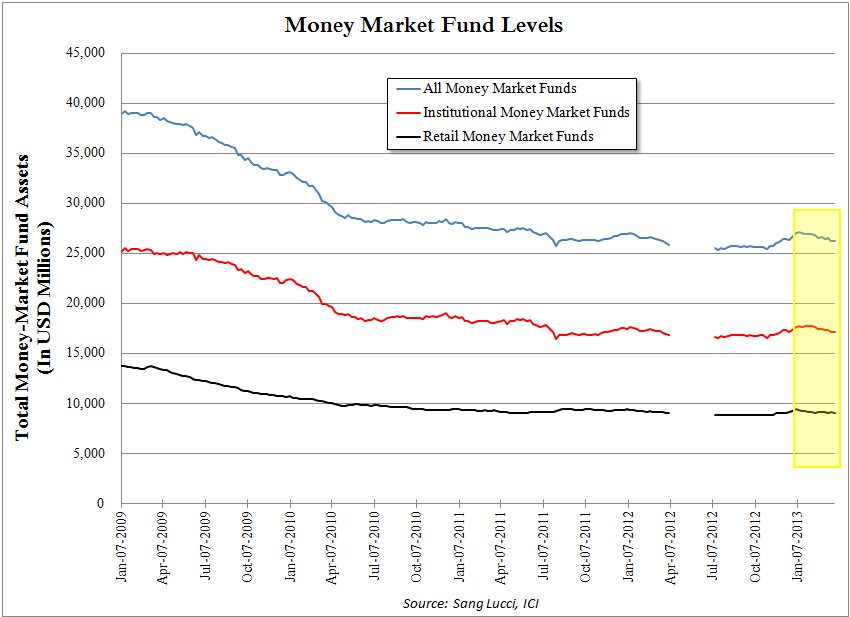

For most people, the broker taking a spread by offering to trade with you at your price, instead of their in house price (for the sake of profit) is a built in issue regulators and other participants expect everyone to accept. This practice is unacceptable and brokers ought to be helping their clients, not ripping them off. This is the main reason I’ve come aboard Sang Lucci, because of their real desire to bring educational material of real value to their relationships. Regulators aren’t going to help us, we need to band together and help ourselves take back the integrity of our markets. Retail Money Market Funds are on the borderline of their lowest levels since 2009:

A dominate reason for the evaporation in retail volume is that the biggest institutions dominate the most historical market center in the US. According to NYSE program trading data for April 13th to April 19th of 2013 Program Trading accounted for 28.9% of volume, a slight decrease from the usual 30-31%. Of note, the Non-Index Arbitrage column constitutes trades not identified as being an arbitrage between the index basket and the derivative. The Non-CS2 column represents trades not marked for the 4:00-6:15 PM EST time period. More on that here and here.

Now couple this level of activity in American markets with the data from Canada that 27% of the interaction between retail and HOT Users (High Order to Trade ratio users) and you can see how much room there is for internalization growth. This is crucial because in Canada, where HFT manipulation is less rampant than in the States thanks to Canadian regulatory backbones, retail-to-retail interaction is a miniscule 4%, highlighting the general inability or lack of willingness to recognize the damage to retail participants:

This is a very serious problem we face and as a group, we need to come together and work to take back the integrity of our financial markets.

Recent free content from Sang Lucci

-

A Squeaky Wheel…

— 5/23/13

A Squeaky Wheel…

— 5/23/13

-

NYMEX Light Sweet Charts

— 5/17/13

-

Exchange Coddling Of HFT Firms Brought To Light Again

— 5/17/13

-

Margin Credit Driving Market Performance

— 5/04/13

-

[Webinar] Trading With Twitter

— 5/03/13

[Webinar] Trading With Twitter

— 5/03/13

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464