The Weekly Top 10:

THE WEEKLY TOP 10

Table of Contents:

1) New uncertainties surrounding a July rate cut, but that will be resolved next week.

1a) The recent rally has not been fueled by economic or earnings growth…nor by an impending trade deal.

1b) Who has the upper hand in the trade war? Look at Huawei vs. U.S. Ag products going forward.

2) History shows that equating “rate cuts” with “QE programs” is a mistake.

2a & 2b) “Don’t fight the Fed” is only a good rule to follow…well after the initial rate cut.

3) “QE programs” & “rate cuts” have two different targets; thus the timing of their impact is much different.

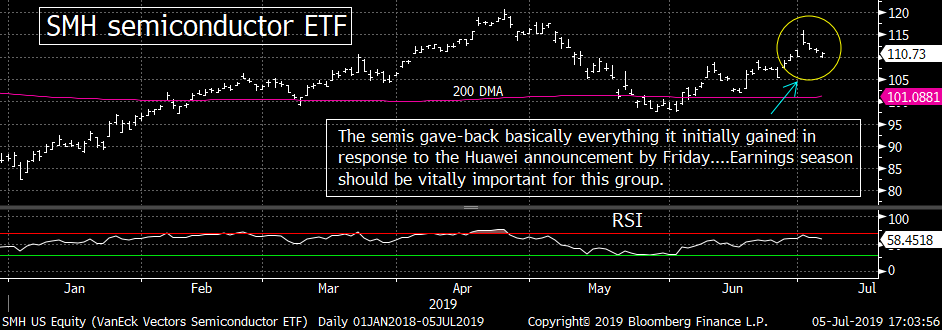

4) The Chip stocks gave back virtually all of Monday’s gap-opening gains by Friday.

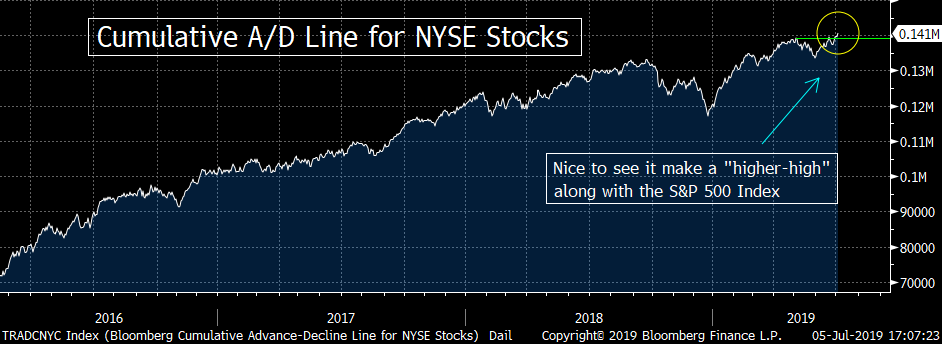

5 & 5a) The S&P 500 is at a critical technical juncture. Further upside follow-through will be quite bullish.

6) TSLA…Strong bounce off of $180. It now has to break $250 to give it another leg higher.

6a) Ford Motor still has a lot of potential. A meaningful break above $10.50 will be very bullish.

7) The U.S. economy is the strongest in the world…but it IS still weakening!

8) Great call on the infrastructure stocks. Take some profits & raise sell-stops.

9) A simple fact: Full-year earnings estimates for the S&P are falling towards zero.

10) Summary of our current stance.

Short Version:

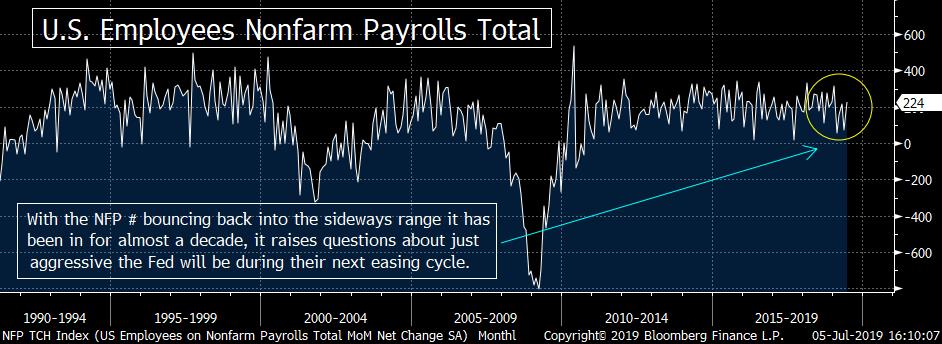

1) Friday’s strong employment report raised some uncertainties about how aggressive the Fed’s will be in their upcoming easing policy. Luckily, a lot of that uncertainty should be resolved by Chairman Powell’s testimony to Congress mid-week next week. Since we have long believed that the Fed is more “market dependent” than they let-on…and the fact the market is at record highs, I believe the Fed will signal that they won’t be as aggressive in cutting rates than the markets have been pricing-in.

1a) This poses a problem for the markets…because expectations of an aggressively easing Fed has been they vital fuel behind the recent rally to new records. The rally has not been fueled by economic growth (which continues to slow…despite the NFP data)…nor has it been driven by earnings (whose estimates keep coming down). It’s also not coming from the odds of a trade deal…which still seems far away.

1b) One more comment on the trade war. If you want an idea of who has the upper hand in the negotiations going forward…just look at how many restrictions are lifted on Huawei vs. how many Ag products are purchased by China…..I’ve said all along that Xi has the upper hand…and that President Trump will have to give in (but still declare victory) eventually (and thus any deal will be a weak one). However, it sure seems like that won’t happen for a while.

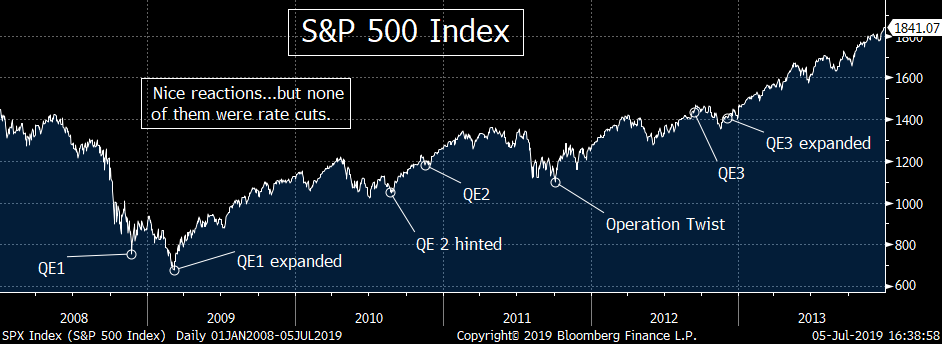

2) Moving back to the Fed, I believe that investors are making a mistake by equating “rate cuts” with “QE programs.” They keep pointing to the fact that that every time the Fed has been accommodative over the last decade, the stock market has rallied. This IS true. HOWEVER, NONE of those easing moves involved a rate cut! They were all QE (or Operation Twist) programs. This is important because history shows that “QE programs” have an immediate impact on the markets…while the initial “rate cuts” are actually (usually) followed by stock market declines…and the positive impact tends to come much later!!! (QE injects liquidity directly and immediately into the system. Rate cuts frequently have a significant lag.)

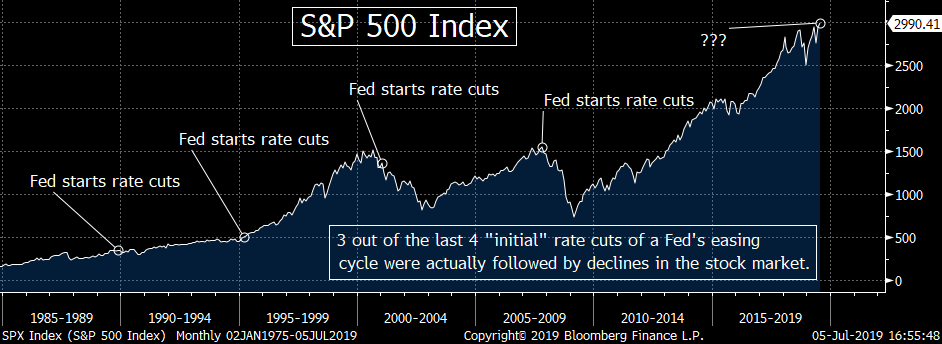

2a & 2b) In other words, “Don’t fight the Fed” is NOT always true. It only becomes an excellent rule to follow once the Fed moves further into its easing process (additional cuts)…not after the initial rate cut!!!

3) In other words, “QE programs” and “rate cuts” are two different types of easing programs that have two different targets. “QE PROGRAMS” are DESIGNED to have a positive impact on RISK ASSETS (which in turn, will EVENTUALLY help the economy grow)….”RATE CUTS”, on the other hand, are DESIGNED to have a positive impact on THE ECONOMY (which in turn, will EVENTUALLY have a positive impact on risk assets). The BIG difference is that the INITIAL effect of a “QE program” takes place much, much, much more quickly than the INITIAL impact of “rate cuts”! Therefore, I believe investors are making a mistake by assuming that the stock market will rally significantly if/when the Fed first begins to cut rates.

4) There is STILL a lot of uncertainty surrounding how many restrictions will be lifted on Huawei. This was not lost on the chip group…as the SMH semiconductor ETF gained more than 5% on Monday’s opening (after the initial Huawei announcement), but gave back basically all of those gains by Friday’s close…..Remember, this group was already lowering guidance BEFORE the trade talks broke down, and BEFORE the Huawei restrictions were imposed. Therefore, whichever way this key leadership group moves after this past week’s “failed rally” should be quite important.

5 & 5a) Having said all this, the stock market has made new record highs…and it has come along with new higher-highs for the A/D line, so that is quite positive. Therefore, although I am cautious right here, I am not pounding the table with that cautious stance. If the S&P 500 can finally break more meaningfully above its old highs (which it has failed to do each of the past three times)…it will also enable the index to regain its trend-line going all the way back to the 2009 lows!!! Therefore, the S&P 500 stands at a critical technical juncture…and thus, investors are going to need to stay quite nimble as we move through the month of July!

6) Tesla has rallied nicely since it hit the level we said was attractive ($180)…and it has broken above its trend-line from the beginning of 2019. However, if it’s going to see another “leg” to this more recent rally, it’s going to have to break back above the key ($250) level (“old support” becomes “new resistance”). If it can do that, it will be very bullish for the stock, but after 32% rally in just four weeks, investors need to wait to see if it breaks that level before they add to positions. (They should also raise their “sell stops” on any of their longs from the $180 level.)

6a) Even though TSLA is getting all this attention, I still believe that Ford (F) is a stock to keep an eye on. It’s been a dog for five years, but it has broken above its trend-line from early 2018. NOW, it is close to testing its longer-term trend-line…going back to 2014…AND is close to making its first “higher-low/higher-high” sequence in five years!......Also, I just think President Trump is going to have to do something for the auto industry over the next six months or so. If not, he won’t win all those states he won in the upper Midwest in 2016. Without those states, he will not be re-elected…period.

7) Many pundits keep saying that our economy is strong…and after Friday’s employment report, they have a point. However, most of the recent data show that our economy is weakening. Who cares if the PMI Manufacturing data is still above 50…and it’s much higher than most other countries??? It’s still only 51.7…and it’s down from 60.8 less than a year ago. There’s no question that the manufacturing sector in the U.S. has also been slowing in a material manner for quite a while now. This reinforces my belief that the stock market’s record highs are based almost solely on help from the Fed and other central banks.

8) Very early in the year this year, I highlighted how the infrastructure stocks were breaking out broadly & said they had a lot of upside potential. Since then, stocks like JEC, TTEK, VMC, MLM, ACM, GLDD & KBR are all up 45%-85% from their December lows (and +30% to +50% since we turned bullish on the group)…..However, they’re getting quite overbought on both a short & intermediate-term basis. Therefore, this should be an excellent place to take some chips off the table & raise “sell-stops” for those who went long the stocks when we first turned bullish.

9) I’d like to finish this week’s piece (before we give our summary) with one of the most important issues facing markets right now: Earnings. We might be able to avoid an earnings recession, but the guidance during the upcoming earnings season is going to be crucial. Full-year consensus estimates are already down to 2.7% for the S&P 500…and THAT’S assuming Q4 will have growth of almost 7%. If the second half guidance falls, it will provide another headwind for stocks. Lower rates help provide multiple expansion, but earnings are still an essential part of that equation.

10) Summary of my current stance.....The stock market had another good week last week. If it can finally break “meaningfully” above its old highs (which would also enable it to regain its trend-line from 2019), it’s going to be quite favorable for the stock market. Therefore, even though we are cautious on stocks at these levels, I am not pounding the table in a bearish way…..However, I just believe that the market is relying too much on potential rate cuts to fuel a strong rally. It’s not going to get help from economic growth, earnings growth, or from a trade deal any time soon. Sure the Fed HAS helped the market rally strongly with their accommodation over the past ten years, but these moves did not involve “rate cuts” (which have not been instituted since 2008). They were fueled by QE programs that inject liquidity directly and immediately into the system/markets. “Rate cuts” don’t do that. They are much more gradual in their effect. In fact, the first/initial rate cut of an easing program is usually followed by a stock market DECLINE…….Again, a strong rally from here IS possible, but the odds are not as high as some pundits are trying to portray right now.

Long Version:

1) The most significant development of the holiday-shortened week was obviously the much better-than-expected employment report on Friday…as the non-farm payroll number showed an increase of 224k vs. the 160k consensus estimate. This raised questions about how aggressive the Fed will be in terms of cutting rates going forward. Some pundits think the number was strong enough keep the Fed from cutting rates at all during their next meeting at the end of the month, but the consensus still believes a 25 basis point cut is in the cards on July 31. However, the strength of the employment report was definitely enough to raise questions about how aggressive they’ll be after a first cut. (The NFP # took a 50 basis points cut in July off the table.)……For me, I am not as sure as the fed funds futures market is that we’ll get that 25 bps cut. Despite the way their words have been portrayed, if you read & listen to what they have actually said recently, they have not indicated a definite rate cut. Therefore, when you combine this…with my LONG-HELD belief that the Fed is much more “market dependent” than they admit to…I think the odds are down to at least 50/50 that they’ll cut rates……..The great thing about this issue is that we’ll know whether I'm wrong or not almost immediately. Fed Chairman Powell’s testifies in front of Congress on Wednesday & Thursday of the upcoming week…and this testimony will be incredibly important. There is no question that the Fed has followed the policy of telegraphing all their moves to the markets well in advance. In recent weeks, the Fed has set high expectations of a July cut, so if a 25 bps rate cut is no longer a certainty, Mr. Powell will NEED to send that signal immediately. In other words, Friday’s number DID add some uncertainty surrounding the Fed’s future actions, BUT that uncertainty should dissipate quickly after the Chairman’s testimony next on Wednesday……Even if I'm wrong, and he does signal that July cut is a sure thing, I believe that Friday’s number (and the record highs in the stock market and the 2% yield on the 10yr note) will lead Mr. Powell to signal that future rate hikes will not be as aggressive as the market had been pricing-in before Friday. As I will show in the next bullet point (#1a), the vast majority of this recent rally has been fueled by the expectations of a very aggressive easing policy going forward. Thus the change in expectations I expect mid-week next week should provide some headwinds for this current rally in stocks.

1a) As I just alluded to, any further significant rally in the stock market is pretty much dependent on the Fed’s generosity. It’s difficult to argue that the market can rally going forward based on improving economic growth, strong earnings growth or a resolution on the trade negotiations…so the Fed has become the only game in town as things stand right now. Even though the employment data came in stronger than expected, growth expectations continue to come down. The Atlanta Fed’s GDPNow estimate has fallen from 2.3% a couple of weeks ago…to just 1.3% now (although it should rise some-what at its next reading…after Friday’s NFP data). Also, firms like Goldman Sachs, Morgan Stanley & JP Morgan have either lowered their 2019 GDP forecasts or raise the odds of a 2020 recession (or both) over the last month! (More on this issue in point #7.)......Earnings also continue to fall…with the full-year consensus number for the S&P 500 is down to just 2.7% growth. (More details on the earnings issue in point #9.)…..Finally, everything we’ve heard from the President and his advisors…as well as from China…tells us that we’re not going to get a trade agreement any time soon. (Late in the week, China demanded that any final deal will have to include the lifting of existing new tariffs…while the White House said they need to stay to ensure compliance of an agreement. So that hasn’t helped things either. Therefore, since these other factors are weighted more to the bearish side of the ledger, if Chairman Powell (and other Federal Reserve representatives) signal that they’re going to go more slowly during their upcoming easing policy than the Fed Funds Futures had been pricing-in before Friday, it could/should create a headwind for the stock market before long.’

1b) One more comment on the trade war. Last weekend, I said that President Trump “blinked first”…and that he gave away a lot…and received nothing in return. (Yes, he got them back to the table, but that’s something they wanted to do already…and there IS some sort of understanding that China will buy more of our agricultural products, but that’s something they were always going to do. So the President got nothing. 'Nuff said.) So how will we know who has the upper hand as the negotiations resume? I think this will be quite easy to determine. Watch to see how many restrictions are really lifted on Huawei vs. how much of our Ag products China promises to buy (and actually buys). If a lot of Huawei restrictions are lifted…and China doesn’t do much on the Ag products, it will confirm that Trump has indeed blinked…and will get very little in the upcoming agreement. (Yes, I DO think there will be an agreement…just nothing this summer. However, as I’ve said all along, Xi has always had the upper hand because he can withstand the punishment. President Trump has to declare victory at some point…due to the up-coming election…no matter what he really gets in the deal.)

2) Moving back to the Federal Reserve, my biggest concern is that even if the Fed keeps expectations quite dovish, I question if that will be as bullish for the stock market as most pundits are predicting right now. The Fed has several tools at its disposal, and the two biggest ones are rate cuts and QE programs. However, in our opinion, investors are making the mistake of equating these two tools. “Rate cuts” are much different than “QE programs”…and history shows that these two different types of easing programs have a very different impact on the markets when they are implemented. More importantly, there is also a BIG difference between HOW QUICKLY these two different easing programs impact the broad stock market……QE programs involve the purchase of securities that push liquidity IMMEDIATELY into the system. There is no lag. The banks put the money to work immediately (usually by buying securities, rather than loaning it out). Rate cuts, on the other hand, entice people and businesses to borrow more money (at least theoretically)…which eventually leads to economic growth (after they build more factories…hire more people…etc.) However, it takes time to build new factories (or retool old ones) and to hire and train new people. Therefore, it takes a lot more time for rate cuts to have a positive impact on the economy. (Yes, the markets WILL tend to sniff out these improvements early, but it’s hard to know how much rate cuts will help, so it’s still a muted response…especially when you compare it to the QE programs of the past decade.)

2a) One only has to look at history to tell you just how different the impact is for these two types of easing programs…especially when it comes to timing. Yes, the BOTH have a positive effect EVENTUALLY, but we have seen on many occasions (even most occasions) that the stock market actually DECLINES when we get the first rate cut. For instance, the first rate cut in September 2007 was followed by a horrible bear market. Similarly, the 1st rate cut in January 2001 was followed by a further decline of 40% in the stock market. In December 1989, the first cut was then followed by a 10% drop in the S&P 500…..….In 1995, the stock market DID respond by rallying after a rate cut. (It actually traded sideways for a month…and then began to rally again.) So that is the one exception over the past 30 years. So these examples tell us that while a stock market rally is not impossible after the Fed initiates its first rate cut…it ALSO tells us that a further rally is FAR from a sure thing (the way some pundits are portraying it right now). In other words, “Don’t fight the Fed” is NOT always true. It only becomes an excellent rule to follow once the Fed moves further into its easing process than just its first rate cut!!!

2b) One thing that people seem to ignore is that the Fed has not cut rates in over a decade!!! That’s right, even though they HAVE engaged in some serious easing programs over the past ten years, it has been with QE programs (or in 1 case, “Operation Twist”), but NOT with rate cuts. These DIFFERENT forms of easing have produced very contrasting results than the initiation of “rate cuts” have in the past. A 24% rally followed the inception of QE1 in 2008 in the stock market. (Of course, the market did see another down-draft in early 2009 before the crisis came to a close…after the “mark to market” rule was dropped…but QE1 helped the market rally a total of 61% from the day QE1 took effect until it ended in April of 2010.)…….After the end of QE1, the stock market immediately rolled-over and dropped 16% over the next two months! The market stumbled around for several months…until QE2 began in November of 2010. A 15% rally immediately followed in the stock market until QE2 came to an end in 2011. However, once QE2 came to an end, the stock market again stumbled around for a couple of months…until it finally declined 18% from early July until late December. THEN, “Operation Twist” was enacted. This direct intervention was again followed by a significant rally…of almost 30% over the next five months……Finally, after another decline in the stock market in 2012, QE3 began in December of that year, and it lasted for about 20 months…and helped the stock market rally over 40% over that time frame……..I am not saying that the QE programs were the only fuel that helped the stock market rally over the last decade. However, the evidence I just provided shows that the QE programs DID have a sizeable AND immediate impact on the markets. When you combine this with the fact that the Fed has NOT cut interest rates at any time since 2008…it shows how much more of an immediate impact these direct programs have on the markets…vs. the “rate cuts” of previous decades.

3) In other words, these two different types of easing programs have two different targets. “QE PROGRAMS” are DESIGNED to have a positive impact on RISK ASSETS…which in turn, will EVENTUALLY help the economy grow…….…….”RATE CUTS”, on the other hand, are DESIGNED to have a positive impact on THE ECONOMY, which in turn, will EVENTUALLY have a positive effect on risk assets. The BIG difference is that the INITIAL impact of a “QE program” takes place much, much, much more quickly than the INITIAL impact of “rate cuts”! Therefore, although the “eventual” outcome for the markets tends to be positive in both instances, it comes MUCH more quickly when they engage in QE. In fact, as I highlighted above, the first “rate cut” of an easing policy is frequently followed by a decline in stocks (sometimes a severe decline). THEREFORE, I BELIEVE INVESTORS ARE MAKING A MISTAKE BY ASSUMING THAT THE STOCK MARKET WILL RALLY STRONGLY IF/WHEN THE FED FIRST BEGINS CUTTING RATES.

4) A week after the announcement, there is STILL a lot of uncertainty surrounding Huawei. Nobody seems to be able to tell the public just how many of the restrictions will be lifted from U.S. companies who want to sell products to the Chinese giant once again. Peter Navarro said last week that only a “small amount of low level chips” will be available to be sold to Huawei…and Larry Kudlow that that the decision was not a “general amnesty.” What does that all mean??? We don’t know…because we haven’t received any details………This uncertainty has not been lost on the chips stocks. After a sharp gap opening to the upside on Monday, the SMH semiconductor ETF has given back basically EVERYTHING it gained Monday morning. Therefore, after opening more than 5% higher on Monday morning, the SMH finished the week with a very slight gain on the week. The lack of upside follow-through to Monday’s gap opening was quite disappointing for this key leadership group. This is a group that had already seen earnings guidance come down (due to lowered demand & pricing expectations) BEFORE the restrictions were put-on Huawei and before the trade negotiations broke-down in early May. Therefore, if the bounce we saw early last week was only a short-lived breather…and the Huawei news does not give it a sustained rally, the bears are going to regain control of the semis. That kind of development would be negative for both the group…and the broad stock market…given how much leadership the semis have provided (in both directions) in recent years.

5) The S&P 500 Index has done very little over the past 18 months, BUT it has rallied almost 9% since early June and more than 25% since Christmas Eve…so the momentum is clearly with the bulls right now! I'd also highlight that NYSE cumulative Advance/Decline Line made a new all-time high last week as well. In 2000 and again in 2007, the A/D line did not create new highs along with the S&P…so this recent “higher-high” for the A/D line also bodes well for the broad stock market. (Of course, the S&P and the A/D have made new highs together just before smaller corrections in the past…just not at the beginning of a bear market. Therefore, this confirmation from the A/D line doesn’t mean we cannot see a short-term pull-back, but it DOES seem to indicate that the great bull market overall isn’t over yet.)………On top of all this, the S&P is re-testing its trend-line going all the way back to the 2009 lows! That’s right; it broke below that line during last year’s deep Q4 correction. The bounce off those lows took it back up to this 10-year trend-line in April (actually moving slightly above it)…only to roll back over. Well, it has moved back up to that line over the past few weeks! So if it can break more meaningfully above that line, it will be quite positive for the stock market. If, however, it rolls back over (like it did in May), things could get rather ugly…rather quickly…..This is a long-winded way of saying that the action over the rest of July should be important for the stock market over the rest of the third quarter. It’s also a long-winded way of saying that even though we are very cautious about the upside potential for the stock market, we are NOT pounding the table on this cautious stance. I readily admit that the market could rally further this summer (even if it shouldn’t). Therefore, investors will HAVE to stay nimble over the coming weeks.

5a) This goes back to what I talked about last weekend with the technical picture for the S&P. Remember, we pointed out that the SPX has broken above its old highs three times in the past 18 months, BUT only by a slight amount. Each time it rolled back over rather quickly…fell in a sizable manner each time. When you combine this with the re-test of the long-term trend-line…and it tells us that whichever way the stock market moves over the next few weeks should be important for how it acts throughout the entire third quarter (and maybe for the rest of the year).

6) The focus that Tesla (TSLA) gets in the market place has not diminished at all. The fact that TSLA has seen TEN swings of 18%- 50% over just that past 18 months makes it an unbelievable candidate for a lot of focus for investors and traders alike. In fact, after its first significant surge in the price of 370% in 2013, the stock has seen more than 25 swings in the 20%-100% range!!!.......For me, I avoided making many calls on the stock until this year, but the two we have made this year have worked out very well. I said that if it broke below the $250 level, it would be a great sell/short candidate…with a target below $200. (That worked-out beautifully.)…After TSLA did indeed fall below $200, I said that some profits should be taken on the short side (and stop levels should be lowered on the rest). I then said if it got down to the $180 level, full profits should be taken…and it should be bought. Well, TLSA did indeed fall below $180, but since that time, the stock has rallied over 30%! So my switch to the bullish side of the ledger worked out great as well....SO NOW WHAT??? Well, even though it has bounced strongly, it has not become seriously over-bought…and it has only retraced about 25% of its 2019 decline. Thus it should have some more decent upside potential. However, TLSA is testing a significant technical level after its big (further) jump on Wednesday. First of all, it is testing its downward sloping trend-line from its December highs of last year…AND it is also testing the under-belly of the multi-year sideways range it had been in since for about 2.5 years. The bottom end of that range had been “old support,” so now it has become “new resistance,” thus any sizable upside follow-through from here should be quite positive for the stock on a technical basis. ……Again, TSLA is not extremely over-bought (and it’s definitely in the neutral area on an intermediate-term basis), so it has a lot of upside potential. However, after a 32% rally in just four weeks, investors/traders who did get long when TLSA fell to the level we said was attractive ($180) should raise their “sell-stop” levels. In other words, we are going to have to see a “meaningful” break above $250 before we can say that the recent “rally” has another strong leg to come. The potential IS there, but we cannot get ahead of ourselves…and all “sell-stops” should be raised after this recent big pop in the stock.

6a) Even though TSLA gets most of the attention in the auto sector right now, I'm still keeping a very close eye on Ford Motor (F)……I just think that President Trump is going to have to help the auto industry at some point late this year or very early next year. He cannot win re-election without the upper Midwest. He won states like Michigan, Wisconsin, Pennsylvania by less than 1%. Throw Ohio into the mix…and he NEEDS these states, or he has NO CHANCE of getting re-elected…….No, I am not aware of any plans that the President has on the back burner, but I will be watching for announcement on this industry as we move into the fall/winter months……However, I will ALSO be watching the stock of Ford itself. More specifically, I’ll be watching the $10.50 level. If it can break above that level in any meaningful way, it will take it above its five-year trend line going back to 2014. It will also give it its first “higher-low/higher-high sequence in five years, so a break-out above that level should be quite compelling on a technical basis……Ford has been a lousy stock for most of the past five years. However, if it can finally seek a technical break-out…and can get some help from the President…it could become one of the biggest surprise winners of 2019 and 2020!

7) A lot has been made recently about the weakness in growth around the world…and rightfully so. Yes, we all know about the better-than-expecte

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464