Morning Comment: Gold & copper poised to diverge...in the other direction.

Well the last two weeks have played out very much like we thought they would. Two weeks ago, we got a “breather” in the market place...which allowed the market to work-off some of the overbought condition that had built up after an 11% rally in less than three weeks. Then we got the Thanksgiving week rally that we thought would take place (like it normally does)...which helped the S&P 500 index rally 2.3% on the week and left it at all-time record highs.......The question right now is whether we’ll also be correct about the next several weeks...and the market will continue to rally into the end of this year (and into very early next year).

We do need to point out that our target for the S&P 500 of 3800 is less than 5% away from where it closed on Friday’s shortened session, so the November rally has already taken the broad market about 2/3 of the way to our December goal. (Just so we can be clear, our December target is 3,800...but we do think it could move a bit above that level in early January.) In other words, more than half of the rally is behind us. Then again, nobody should turn their nose up at another 4%-5% of gains either!

It is our belief that the Fed will continue to keep the liquidity spigots wide open during the next several weeks...due to the fact that the most difficult part of the newest wave of the coronavirus is still in front of us...and should last into early next year. This will likely cause more (and/or further) lock-downs...which, in turn, will cause some further slowdown in the rate of economic growth...at one of the most important times of the year for the economy. Therefore, we believe that the Fed will keep stimulus quite plentiful...so that defaults will not become a serious option for companies over the coming months in the Fed’s beloved credit markets........When you combine this with the enthusiasm that has normally pushed stocks higher at the end of an election year over the past 60 years...and you have a nice formula for further gains.

Last year, the December rally came in a straight line, but we doubt it will be quite that easy this time around. There are still concerns about the virus and the impact it will have on our healthcare system...so we could/should see a few small hiccups along the way. Also, given how expensive the market has become over the last few months, we will certainly be looking VERY closely for signals that we’re wrong...and that the market will roll-over sooner than we’re thinking.

However, we also want to note that several groups could rally a lot more than the above mentioned 4%-5% we’re looking for in the broad market. The bank stocks and energy stocks are still very under-owned (especially the energy names). So if they continue to rally into the end of the year, the reweighting of these groups could/should help them rally more than some of the other “value” sectors that are not quite so under-owned.....That said, the bank and energy stocks are overbought on a very-short-termbasis, so they could see some weakness early this week. However, if long-term interest rates remain near their recent highs of 0.9% (or higher)...and if oil can remain well above $40 (even if both pull-back slightly early this week)...it should help these groups quite a bit into the end of the year.

Switching gears, Bitcoin fell over 15% at one point last week. We called for a 15%-20% pullback, but we didn’t think it would happen in just two days!!! However, it has already bounced-back strongly...and has retraced 75% of that decline (almost all of the decline if you use last week’s closing high as a starting point). This tells us that it will likely get to 20k level we highlighted a week and a half ago before it sees a real and tradable decline. However, given what happened last week, we’re now thinking the real correction will be in the 20%-30% range. (Again, from somewhere near 20k.)

Gold has fallen below $1,800 like we thought it would...and has now broken below its 200 DMA. However, it is finally becoming oversold after its 14% decline from its early August all-time highs. Therefore, we believe that this is a good area to start nibbling on the buy side once again. We’re thinking that it could/should see one more wash-out move...down to (or just below $1,750). So that is a level where we’d want to get more aggressive. (We might hit that level today...the way gold has been falling recently...so getting we might be getting much more aggressive almost immediately.) Either way, “the death of gold due to the rise of bitcoin” is something that is becoming WAY over-done...so we think that gold is starting to look very, very attractive.

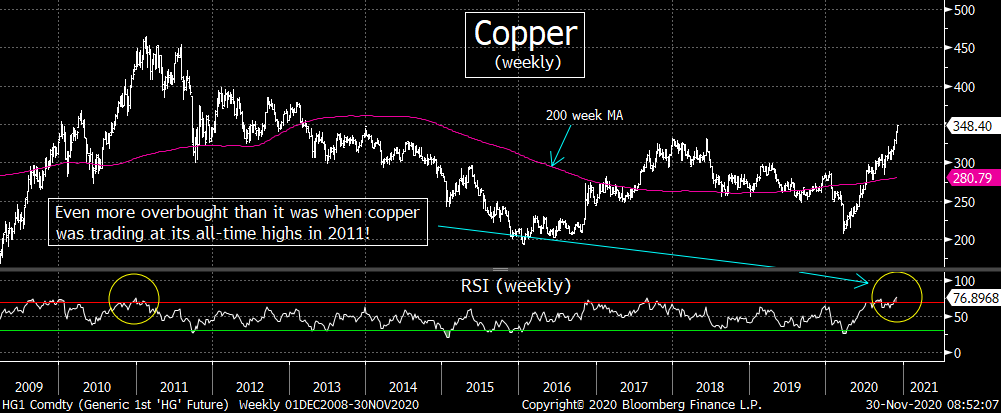

Over the years, the correlation between gold and copper has been a pretty strong one. That said, there have certainly been some times when they have diverged from one another. One of those times has been the last four months...as gold has fallen while copper has been rallying strongly. We think this divergence will continue...but in the opposite direction. In other words, as gold is becoming ripe for a rally...copper is becoming quite ripe for a tradable decline. To be more specific, after the 21% rally over just the past two months in copper, the weekly RSI reading for the commodity is now slightly more overbought than it was at the 2011 all-time highs!

Don’t get us wrong, we are still bullish on commodities for 2021...and we DO think that the more normal correlation between copper and gold will likely return next year. However, no market moves in a straight line. (Sorry for that over-used line, but it IS a very true one.) Therefore, after such a strong move over a relatively short period of time...we think that copper has become quite ripe for a correction. This should be true EVEN THOUGH copper has recently made a nice “higher-high”. (Again, nothing moves in a straight line.)....With this in mind, we believe shorter-term traders should take profits in copper and copper related equities (like SCCO, etc)...and that longer-term investors avoid chasing these assets up at these levels.

Yes, yes....the DXY dollar index did break below its KEY support level, but it is becoming quite oversold and is due for a bounce soon. We think the real dollar weakness will come after it has worked-off its current oversold position (and it’s current over-shorted position in the COT data that we’ve harped-on recently) before that (more significant) decline takes place.

Matthew J. Maley

Managing Director

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464