Where I Stand - Clarifying My Position

I've been saying for a while now that from a big-picture perspective, this is not a low-risk environment. Today I thought I would do some "esplainin" on my point of view.

First, let's dispel the idea that my position suggests it is time to take a cautious stance. This is certainly not the case. You see, in the investing game there are times to be cautious, times to be aggressive, and times to stick with the bulls and enjoy the ride. In my humble opinion, the latter best describes the approach to be taken at this time.

Back in the early 1990's, when the bulls were really starting to run, Ned Davis wrote, "Three hard down days in here would be a gift." Ned's position was clear. His models were telling him that the bulls were in control, that sentiment had become overly negative for a long period of time (remember, the "Crash of '87" was still fresh in the minds of investors and the first Gulf War was creating havoc in the markets) and that stocks were cheap. This is an example of a time when being aggressive makes a lot of sense.

The Trend is Your Friend

Compare and contrast that position to today's market environment. Yes, the bulls are in control. Our trend models are positive and our momentum models are "okay." It is said that the most bullish thing a market can do is make new highs. So, with the S&P 500, DJIA, NASDAQ Composite, Midcap, and Smallcap indexes all sitting within a stone's throw of new all-time highs, it is clear that the trend is definitely a "friend" to stock market investors at this time. And as the saying goes, "Don't fight the tape."

Beware of the Crowd

However, unlike during the aftermath of the first Gulf War, investor sentiment is extremely positive at this time. One can argue that this is due in large part to Mr. Trump's and the Republican's stunning victories in November. And I'm not the first to suggest that the current joyride to the upside represents a discounting of better days ahead for both the economy and corporate profits.

Yet at the same time, we should always be aware of the crowd - especially when they are at extremes. So, I ask you, is there anyone, anywhere that cannot recite the bull case at the present time? Yes fans, this is what the crowd at extremes looks like.

The Subject of Valuations

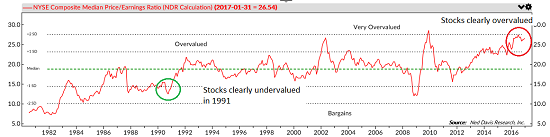

And then there is the subject of valuations. I've written on this subject many times over the past couple of years and cutting to the chase, I haven't changed my stance. The bottom line is that stocks are currently overvalued on every traditional "absolute" metric such as Price-to-Earnings/Dividends/Book Value/Cash Flow/Sales.

The chart below makes this point very clear.

And yes, one can argue that "relative" valuations are significantly better. Recall that "relative" valuations compare the level of stock prices to that of interest rates. The thinking is that if rates are low, stock prices can be higher because there is competition (low rates have also traditionally been viewed as being positive for the economy).

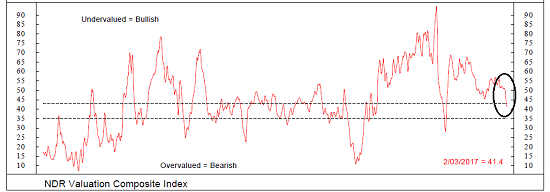

The chart below is a composite index created by Ned Davis Research that (a) goes back to 1965 and (b) compares the valuation of the S&P 500 to a myriad of rate-sensitive metrics including: earnings yield, dividend yield, book value yield, real earnings yield, real dividend yield, bond yields, etc.

The first thing to notice about this particular chart is you have to turn your view upside down because when the line is in the upper reaches of the chart, stocks are undervalued and vice versa.

The good news is that, according to a "relative" approach to valuation, stocks are NOT overvalued. Yet, it is also important to note that they are no longer undervalued either. And if you look at the trend of the indicator, you will see that this index has been moving steadily down (i.e. toward overvalued) for some time now.

The next big-picture item to consider here is that interest rates are rising. And just about everybody on the planet expects rates to continue to rise in the coming years. So, your "relative" valuation metrics are going to need much stronger earnings, dividends, cash flow, book value, etc., in order to stay out of the danger zone.

So, the takeaway is that stocks are most definitely NOT cheap at this point in time. Maybe the market isn't as overvalued as the bears contend when rates are taken into account. But they also aren't as undervalued as the bulls might suggest.

All Good Things Come to an End, Eventually

And finally, there is the age of the current bull. To be clear, I'm talking about the current "cyclical" bull move here, which began on February 11, 2016. Remember, there are cyclical and secular moves in the market. The secular trend usually lasts many years while the cyclical moves are shorter in duration.

There is no denying that the secular bull move, which began on March 9, 2009, remains alive and well. No, in my humble opinion, it's the current cyclical move that needs to be monitored.

With the current cyclical bull set to enjoy a birthday party next week, we should probably keep in mind that these moves don't last forever. In fact, according to the computers at Ned Davis Research, the median cyclical bull since 1900 has lasted 670 calendar days or about 1 year, 10 months.

Therefore, an objective investor must recognize that the bulls "could" encounter some difficulty at some point in the next year. But the good news is that cyclical bears that occur within the context of a secular bull, are traditionally shorter and shallower than normal (the most recent cyclical bear that occurred between August 2015 and February 2016 is a great example of this).

This is where you should start to weigh the risk factors in the market at the present time - to try and figure out whether the current bull will be longer or shorter than the median. And as yesterday's model review and the ramblings above suggest, risk factors are NOT low at this stage.

As such, we can probably agree that unless the economy/earnings pick up SUBSTANTIALLY more than expected (and expectations are high at the present time), the current bull could stumble if there are any real bumps in the road in the next 12 months.

In Sum...

To sum up, I believe the bulls remain in control and will likely continue to be for some time. However, given that expectations are high, rates are rising, valuations are stretched, and the current bull is aging fast, I will conclude that this is not the time to be aggressive. No, this is the time to enjoy the bull train and to be scanning the horizon for storm clouds. Hope this makes sense!

Current Market Drivers

We strive to identify the driving forces behind the market action on a daily basis. The thinking is that if we can both identify and understand why stocks are doing what they are doing on a short-term basis; we are not likely to be surprised/blind-sided by a big move. Listed below are what we believe to be the driving forces of the current market (Listed in order of importance).

1. The State of Trump Administration Policies

2. The State of the U.S. Economy

3. The State of Global Central Bank Policies

Thought For The Day:

"Price is what you pay. Value is what you get." -Warren Buffett

Wishing you green screens and all the best for a great day,

David D. Moenning

Chief Investment Officer

Sowell Management Services

Disclosure: At the time of publication, Mr. Moenning and/or Sowell Management Services held long positions in the following securities mentioned: none. Note that positions may change at any time.

Looking for a "Modern" approach to Asset Allocation and Portfolio Design?

Looking for More on the State of the Markets?

Investment Pros: Looking to modernize your asset allocations, add risk management to client portfolios, or outsource portfolio design? Contact Eric@SowellManagement.com

Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

David D. Moenning is an investment adviser representative of Sowell Management Services, a registered investment advisor. For a complete description of investment risks, fees and services, review the firm brochure (ADV Part 2) which is available by contacting Sowell. Sowell is not registered as a broker-dealer.

Employees and affiliates of Sowell may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Advisory services are offered through Sowell Management Services.

Recent free content from FrontRange Trading Co.

-

Is The Bull Argument Too Easy These Days?

— 8/31/20

Is The Bull Argument Too Easy These Days?

— 8/31/20

-

What Do The Cycles Say About 2020?

— 1/21/20

-

Modeling 2020 Expectations (Just For Fun)

— 1/13/20

-

Tips From Real-World Wendy Rhoades

— 5/06/19

-

The Best Recession Ever!

— 4/29/19

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

{kind=link}

{kind=link}

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464